Liaison Office in Bangladesh: Registration, Rules and Compliance

Understand how a liaison office in Bangladesh works, what BIDA approval involves, where the limits sit, and which compliance steps…

Learn how remittance in Bangladesh works, formal channels to use, how incentives apply, and compare fees, rates, delivery options, and risks.

Hundi can look convenient until the receipt disappears. Sending remittance in Bangladesh can feel simple too, until they get caught in fees, weak rates, or the wrong channel. You send it. Your family waits.

That is why the channel matters before the money even leaves your hand. The route you pick, whether a bank, a licensed exchange house, or an account deposit, decides what your family actually receives. With Bangladesh taking in more than $32.7 billion in remittances in the first 11 months of FY 2025 to 2026, the stakes aren’t small. This guide breaks down the safest ways to send money, where fees hide, and what to check before you choose a channel.

A remittance is money sent by someone abroad to a person or account back home. In Bangladesh, the word usually points to migrant workers, Bangladeshis living abroad, and overseas professionals. It can land in a bank account, cash pickup point, or mobile wallet, depending on the route.

For Bangladesh, this is not side money. The country is widely cited as a top 10 global recipient, with IOM-based coverage in 2026 describing Bangladesh as the eighth largest recipient for 2024. Recent Bangladesh Bank data reported by local outlets showed about $3.42 billion to $3.43 billion in May 2026 alone.

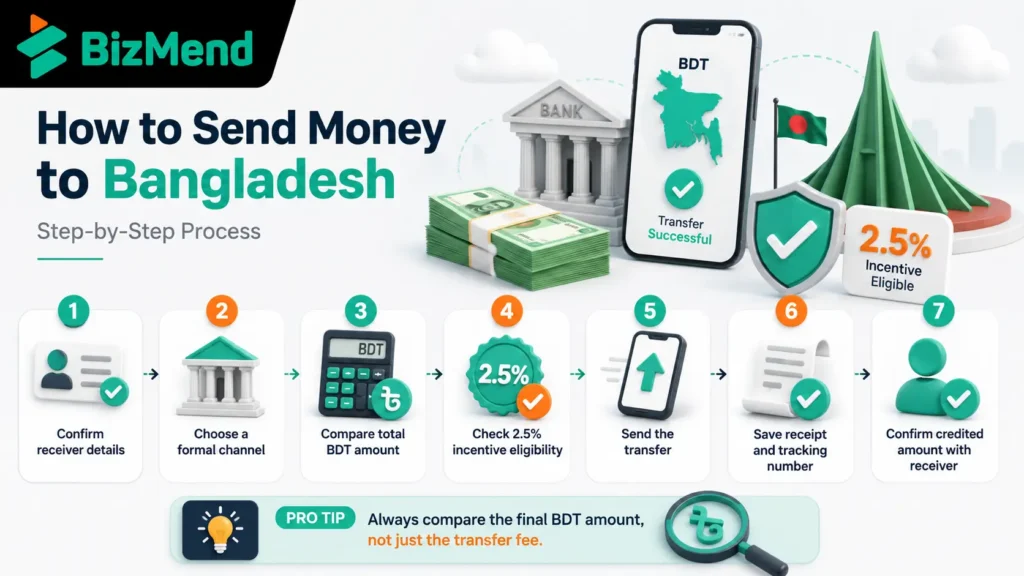

A remittance route isn’t just about speed. It’s also about proof, rate, and legal protection.

That is why the channel matters. For foreign remittance in Bangladesh, clean records help the receiver prove where the money came from, claim any eligible incentive, and avoid messy questions later. A higher promised rate means little if the receiver has no receipt, no complaint path, and no bank record.

A formal channel is any legal route that moves money through regulated banks, licensed exchange houses, recognized MTOs, approved payment providers, or licensed mobile financial service providers. The sender may see a branch counter, an agent desk, an app, or a web portal. The receiver sees the final payout.

The best channel is not one brand for everyone. It depends on the sender’s country, transfer size, receiver access, exchange rate, pickup rules, incentive handling, and how much proof you need later. Okay, that’s a lot. But this is exactly where people save money.

Most failed or frustrating transfers start with a small detail: a mismatched name, old phone number, wrong account type, or unclear pickup instruction. Slow down before the transfer leaves your hand.

If the transfer is for business, salary, export income, or investment, do not label it casually as family remittance. The purpose can affect bank questions, tax records, and incentive treatment. The cleaner the label, the fewer headaches later.

Bangladesh’s government incentive is one of the biggest reasons formal remittance channels matter. As of June 2026, major bank and wallet pages still describe a 2.5% government incentive for eligible wage earners’ remittances sent through legal channels. Policies can change, so check the current rule before sending.

Some transfers may not qualify under the wage earner incentive. Bank guidance lists items such as FDI, donations, trade payments, freelancing or IT service income, remote job payments, exports, gifts, goods or service transactions, bond purchases, and foreign cash brought by nonresidents as outside this incentive bucket.

That does not mean every other transfer is bad. It means it may follow another rule. If you’re receiving business or service income, ask the receiving bank how to code it and what documents they need.

The sender fee is only the loudest cost. The quiet cost is often the exchange rate margin, meaning the gap between the market reference rate and the rate your provider uses. A transfer with a low fee can still deliver less BDT if the rate is weak.

The cheapest fee can still be the costly route if the exchange rate is weak.

World Bank Remittance Prices Worldwide data is a useful reminder here. Its Q3 2025 report put the global average cost of sending $200 at 6.36%, while digital remittances averaged 4.59%. For the USA to Bangladesh corridor, World Bank data showed a total average cost of 7.61% in Q3 2025. Your provider may be better or worse.

Use the channel that fits the receiver’s real life, not the one that sounds the newest. A parent in a village, a spouse with a bank account, and a small shop owner receiving customer money do not need the same route.

The practical test is simple: can the receiver collect the money easily, can you prove the source, and does the final BDT amount still look good after every charge? If the answer is no, keep comparing.

Mobile wallets have made remittance easier for many families. bKash, for example, says expatriate Bangladeshis can send money to bKash accounts through authorized and listed foreign banks, MTOs, and exchange houses. Its page also says receivers using legal channels get the 2.5% government incentive.

There are limits and charges to check. bKash states that remittance to a bKash account can be sent up to BDT 250,000, and it lists an ATM cashout charge of BDT 7 per thousand for remittance cashout from specified ATM networks from March 19, 2024. Read the current page before sending.

Bangladesh Bank has allowed licensed MFS providers to bring wage remittances in association with recognized foreign payment partners. That helps explain why wallet routes are now part of the formal remittance channel BD conversation. Still, wallet delivery is inward remittance. It does not mean every outward transfer from Bangladesh is allowed.

Hundi can look tempting because the quoted rate may beat the bank rate. Let’s not sugarcoat it: the risk is real. The transfer may leave no legal receipt, no regulated complaint path, and no clean source record for the receiver.

Bangladesh authorities have linked hundi to illegal money transfer and money laundering concerns. Even if the sender only wants to help family, the informal route can put the receiver in a weak position when a bank, tax office, or law enforcement agency asks questions.

Family remittance is usually about support: food, education, rent, medical costs, savings, or building a home. The receiver should keep the bank SMS, wallet statement, receipt, and any incentive credit record. These small records can matter during disputes.

Small businesses need a stricter habit. If money is coming from a foreign customer, investor, buyer, marketplace, or employer, it may not be ordinary wage remittance. The bank may need an invoice, agreement, purpose code, contract, or tax record.

Do not mix family support and business receipts in one casual trail. If a business owner receives customer payments as personal remittance, the problem may not show up today. It can appear later during tax filing, loan review, audit, or account checks.

Before sending money to Bangladesh, run through this short check. It takes a few minutes, and it can save days of calls afterward.

If a provider cannot answer these questions clearly, pause. A real channel should make the cost, delivery path, and proof easy to understand before you pay.

Remittance in Bangladesh works best when you stop chasing only the loudest rate and compare the whole transfer. The right route is legal, traceable, fairly priced, and easy for your receiver to use. For most families, that means an authorized bank or MTO, with mobile wallet delivery when speed matters. For business money, keep the purpose clear from day one. A little checking before sending saves a lot of stress after.

The safest way is to use a formal channel: an authorized bank, licensed exchange house, recognized MTO, or approved mobile wallet partner. You should receive a tracking number, clear fee, exchange rate, receiver details, and a complaint route. If there is no receipt, walk away.

As of June 2026, major Bangladeshi bank and wallet pages still describe a 2.5% government incentive for eligible wage earners’ remittances sent through legal channels. Check the latest Bangladesh Bank or receiving bank rule before sending because incentive rules can change.

Yes, if your sending provider is an authorized partner that supports bKash delivery. bKash lists foreign banks, MTOs, and exchange houses as routes for sending remittances to bKash accounts. Check the current transaction limit, receiver name, wallet number, incentive treatment, and cashout charge.

No. Hundi may promise a better rate, but it removes regulated proof and can create legal, tax, fraud, and money laundering risks. The receiver may also lose the benefit of a clean banking record and any eligible government incentive.

They should confirm the purpose of the payment before it arrives. Customer invoices, export proceeds, remote work income, investment money, and family support can be treated differently by banks and tax authorities. Keep contracts, invoices, bank advice, and conversion records together.

Understand how a liaison office in Bangladesh works, what BIDA approval involves, where the limits sit, and which compliance steps…

Branch office in Bangladesh explained for foreign companies, from BIDA approval and USD 50,000 remittance to RJSC, TIN, VAT, and…

Learn the current income tax slabs in Bangladesh for 2026. Understand who must file, what documents you need, and how…