How to Send Money to Bangladesh: Best Apps, Banks & Transfer Options

Send money to Bangladesh with clear comparisons of apps, banks, cash pickup, mobile wallets and wires, plus fee and speed…

Compare life insurance in Bangladesh by policy type, provider strength, claims record, legal terms, and family protection needs.

One bad insurance policy can haunt a family for years. Life insurance sounds like a relief until the claim day comes. Then the small details matter. The nominee, the exclusions, the unpaid premium, and the policy you barely read. Everything starts to become meaningless.

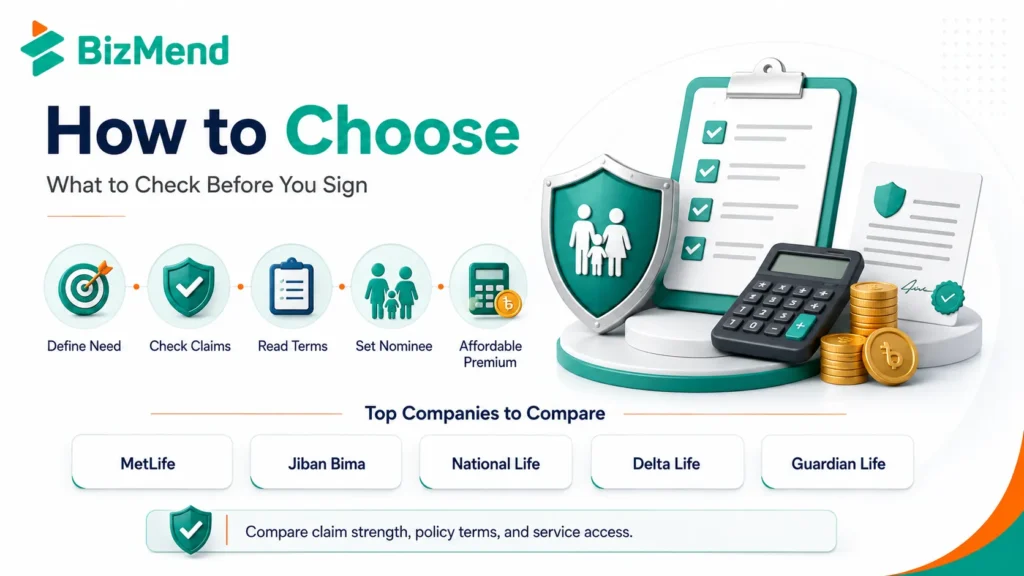

In Bangladesh, life insurance can protect income, education, loans, retirement plans, or business stability. But not every policy deserves your money. Some mix savings and protection so tightly that buyers miss the real cost. This guide breaks down the main policy types, top companies to compare, and the checks to make before you sign.

Life insurance is a contract. You pay premiums, and the insurer promises a defined benefit if the insured person dies, survives to maturity, or meets another covered condition. In Bangladesh, that contract sits under the Insurance Act 2010 and IDRA supervision.

The market is bigger than many first-time buyers expect. IDRA’s licensed insurer list includes state-owned Jiban Bima Corporation, foreign company MetLife, listed insurers such as National Life and Delta Life, and newer private players such as Guardian Life, LIC Bangladesh, Astha, Akij Takaful, and NRB Islamic.

For buyers, the core question isn’t whether insurance sounds good. It’s about what job the policy must do. Family income protection, retirement savings, education planning, employee benefits, loan protection, and business continuity all need different structures.

A life policy should solve a real risk, not just make a premium receipt look responsible.

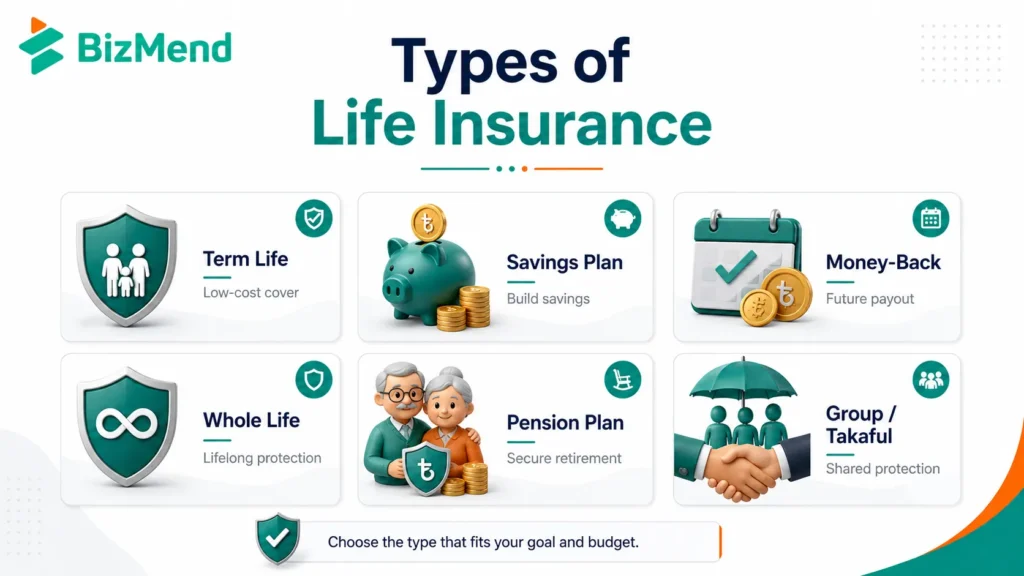

If you’re comparing a life insurance policy Bangladesh providers offer, the product name can feel confusing. Many plans use words like savings, protection, DPS, pension, Hajj, child education, money back, or Takaful. Strip the name down to the benefit pattern.

| Policy type | What it usually does | Best fit |

|---|---|---|

| Term life | Pays a death benefit for a set period, often with little or no savings value. | Parents, borrowers, founders, and income earners who want low-cost protection. |

| Endowment or savings plan | Combines life cover with a maturity payout if you keep paying until the end. | People who want disciplined savings plus protection. |

| Money-back plan | Pays scheduled survival benefits during the policy term and may pay maturity value later. | Buyers who need planned cash points for education or family costs. |

| Whole life | Runs for life or a very long period, subject to policy terms and premium payment. | Estate planning or lifelong family protection. |

| Pension or retirement plan | Builds future income or lump-sum value for retirement. | Workers and business owners without enough retirement savings. |

| Group life | Covers employees, association members, or borrowers under one group policy. | Employers, lenders, and organizations. |

| Takaful | Uses a Shariah-based structure for protection and savings. | Buyers who want an Islamic insurance model. |

The official product list shows how broad the market is. IDRA-approved products include term insurance, child education plans, pension insurance, group insurance, health riders, credit shield, Hajj Bima, Denmohor Bima, and savings plans across several insurers.

Term life is the cleanest protection product. If the insured person dies during the policy term, the nominee receives the sum assured, subject to exclusions and documents. If the person survives the term, many pure term plans don’t pay a maturity amount.

That tradeoff is why term cover can be useful. You’re paying for risk protection, not forcing every taka to behave like savings. For a young parent or business owner, that can mean more cover for the same budget.

Endowment and savings plans are common in Bangladesh because people like seeing money come back. They can help disciplined savers, but the protection amount may be lower than a similar premium spent on term life.

Goal-based policies can be useful when the goal is real and dated. A child education plan should match school or university timing. A pension plan should match retirement age. A Hajj plan should make sense besides other savings options.

Don’t buy these plans because the label sounds responsible. Ask for the maturity schedule, surrender value table, and the total premium you’ll pay over the full term. The total cost is where weak decisions often show up.

Group life covers many people under one policy, often through an employer. Credit life can repay a loan if the borrower dies. Bancassurance is newer in Bangladesh. Banks act as corporate agents, and it introduced both life and non-life insurance products on 4 March 2024.

Bank-based insurance can be convenient, but don’t treat convenience as suitability. If a bank offers cover with a loan or deposit, ask whether it’s optional, who the insurer is, what the bank earns, and how claims are filed.

No single company is best for every buyer. A young parent, a retired couple, a salaried worker, and a garment factory owner may need different products from different insurers.

So treat this as a practical shortlist, not a ranking. These names are worth comparing because they appear in regulatory data, public filings, bancassurance channels, or visible market reporting.

| Company | Why readers compare it | Buyer check |

| MetLife Bangladesh | Large international life insurer. Its Bangladesh page lists around 1 million customers and 9 sales offices. Reporting for 2024 placed it first in life premium income. | Compare product terms, price, medical rules, and local service access. Large size does not replace policy reading. |

| National Life Insurance | Major local insurer. TBS reported Tk2,102 crore in 2024 premium collection, and its annual report shows a strong premium volume. | Check claim history, branch service, product charges, and maturity assumptions. |

| Delta Life Insurance | Long-standing listed life insurer. Its 2024 financial highlights show Tk948.31 crore gross premium and Tk907.83 crore claims. | Review current governance notices, unsettled claim lists, and official claim documents. |

| Jiban Bima Corporation | The lone state-owned life insurer started on 14 May 1973, with public sector reach. | Check service speed, product fit, online facilities, and the branch you will actually use. |

| Guardian Life | Visible in modern retail, group, and bancassurance channels. IDRA-linked reporting placed it among the top five claim settlers in the first half of 2025. | Review benefit limits, hospital or group conditions, claim submission steps, and renewal terms. |

| LIC Bangladesh | A recognizable foreign-linked brand in Bangladesh, also present in bancassurance listings. | Confirm the exact local entity, product terms, premium collection method, and service points. |

| Popular Life, Pragati Life, Sandhani Life, Meghna Life | Established private names that often appear in market lists and policy discussions. | Use the latest annual report, claim data, and IDRA notices before treating any as a final choice. |

This is where the guide needs to be honest. Bangladesh has credible life insurers, but the sector has also struggled with delayed claims, weak governance, and public mistrust. That’s not a footnote. It’s part of the buying decision.

In July 2025, 15 life insurers were in a high-risk category, and around 45 percent of life insurance claims remained unsettled at the end of 2024. The same report cited 13 lakh pending life claims worth Tk 4,414 crore.

A cheap premium loses its charm if the claim money doesn’t arrive when the family needs it.

IDRA also ordered special audits of 15 life insurers in 2025 to review financial distress, delayed claims, shrinking assets, life fund weakness, and management expenses. The lesson is simple: don’t buy from a name just because an agent seems confident.

Your first filter should be the reason for buying. A policy for family income protection should be judged by death benefit and affordability. A policy for retirement should be judged by long-term value, surrender rules, and realistic payment discipline.

If you’re using insurance for business continuity, add two more checks. First, make sure the business can pay premiums even during low sales. Second, decide whether the company, family, lender, or partner should receive the benefit.

A simple rule is better than guessing. Add household debt, future education costs, funeral costs, and 5 to 10 years of income support. Then subtract liquid savings your family could actually use without selling a home or closing a business.

| Need | Question to ask | Example |

|---|---|---|

| Family income | How many years would dependents need support? | Tk 80,000 monthly support for 7 years equals Tk 67.2 lakh before inflation. |

| Debt | Which loans should disappear if you die? | Home loan, business loan, vehicle loan, or personal loan balance. |

| Education | What future cost is already predictable? | School, university, coaching, hostel, or overseas study support. |

| Business continuity | What cash would keep operations alive? | Payroll, rent, supplier dues, and partner buyout cost. |

| Final costs | What immediate expenses would the family face? | Medical bills, funeral costs, and short-term household cash. |

Don’t chase a round number because it sounds big. A Tk 10 lakh policy may be helpful for some families and far too small for others. The number should come from obligations, not pride.

The Insurance Act 2010 matters because it sets rules around policyholder rights and insurer conduct. For example, section 57 lets a life policyholder nominate the person or persons who should receive policy money after death, subject to the policy and legal rules.

Surrender is another key issue. Under the Act, a relevant life policy in force for at least 2 years may be surrendered at the policyholder’s written request, and the insurer generally has 1 month to pay the surrender value after the request, subject to the Act’s conditions.

No buyer can audit an insurer like a regulator. But you can still check signals. Look at licensing, financial statements, life fund size, claim settlement behavior, credit rating, branch or service reach, digital claim options, and complaint history.

MetLife Bangladesh has around 1 million customers, 14 customer touch points, 232 agencies, and around 16,000 financial associates. Those figures don’t prove every policy is right, but they show why scale and service reach belong in the comparison.

For smaller or newer companies, ask harder questions. How long has the company operated? Has it filed current statements? Are claims being paid on time? Does the agent explain exclusions without rushing you? A weak answer now can become a painful claim later.

The most common mistake is treating life insurance like a guaranteed investment. Some policies do build value, but protection and savings aren’t the same job. If you mix them, make sure you understand the cost of mixing them.

Life insurance is a long promise. If the premium feels tight in month one, it may become unbearable in year five. Buy the policy you can keep, because a lapsed policy protects nobody.

Before you sign, slow the process down. A serious insurer or agent should tolerate questions. If someone pressures you to decide immediately, that’s useful information too.

Life insurance in Bangladesh can be a smart family and business protection tool, but only when the policy matches the risk. Start with need, then compare licensed providers, claim behavior, cost, surrender rules, and service. A good policy should make a hard day easier for your family, not leave them chasing paperwork.

Life insurance in Bangladesh is a contract with a licensed life insurer. You pay premiums, and the insurer pays a benefit after death, at maturity, or after another covered event, depending on the policy type and terms.

There isn’t one best company for every buyer. Recent verified signals point to companies such as MetLife, National Life, Delta Life, Jiban Bima Corporation, Pragati Life, Popular Life, Guardian Life, Alpha Life, and LIC Bangladesh, but you should compare claim settlement, financial strength, product terms, and service access.

Term life is usually better for pure protection because it can offer more cover for a lower premium. Endowment insurance may fit buyers who want savings plus protection, but they should compare total premiums, guaranteed returns, surrender value, and the actual death benefit.

Yes, a life policyholder can usually change or cancel a nomination before the policy matures, following the insurer’s process and the Insurance Act 2010. Always get written confirmation that the insurer has registered the updated nominee.

Ask for the sum assured, premium term, maturity benefit, surrender value, exclusions, claim documents, agent license status, payment methods, revival rules, and claim settlement record. If the answers aren’t clear in writing, don’t sign yet.

Send money to Bangladesh with clear comparisons of apps, banks, cash pickup, mobile wallets and wires, plus fee and speed…

Learn how remittance in Bangladesh works, formal channels to use, how incentives apply, and compare fees, rates, delivery options, and…

Understand how a liaison office in Bangladesh works, what BIDA approval involves, where the limits sit, and which compliance steps…