How to Become a Daraz Seller in Bangladesh: Registration, Fees & Growth

Learn how to become a Daraz seller in Bangladesh, register an account, list products, understand fees, manage orders, and grow…

Compare health insurance in Bangladesh by plan type, coverage, exclusions, claim process, hospital network, and company fit before choosing a policy.

A serious illness can turn savings into paperwork overnight. Health insurance in Bangladesh helps reduce that shock, but only when the plan matches the hospital, claim rules, and family risk. The best choice is rarely the loudest ad.

Bangladesh has life insurers, non-life insurers, employer group plans, hospital cash benefits, critical illness cover, and smaller digital health products. This guide explains how they differ, which companies are worth comparing, and what to check before you pay the first premium.

Quick Answer: Health insurance in Bangladesh is a policy or rider that helps pay, reimburse, or provide fixed cash benefits for covered medical events such as hospitalization, surgery, critical illness, accidents, or employee health claims. The right plan depends on your age, budget, hospital preference, family size, exclusions, waiting periods, claim process, and whether you need individual, family, or corporate coverage.

There is no single best health insurance company in Bangladesh for everyone. Compare licensed insurers, written benefits, hospital networks, claim documents, room limits, renewal rules, and exclusions before choosing.

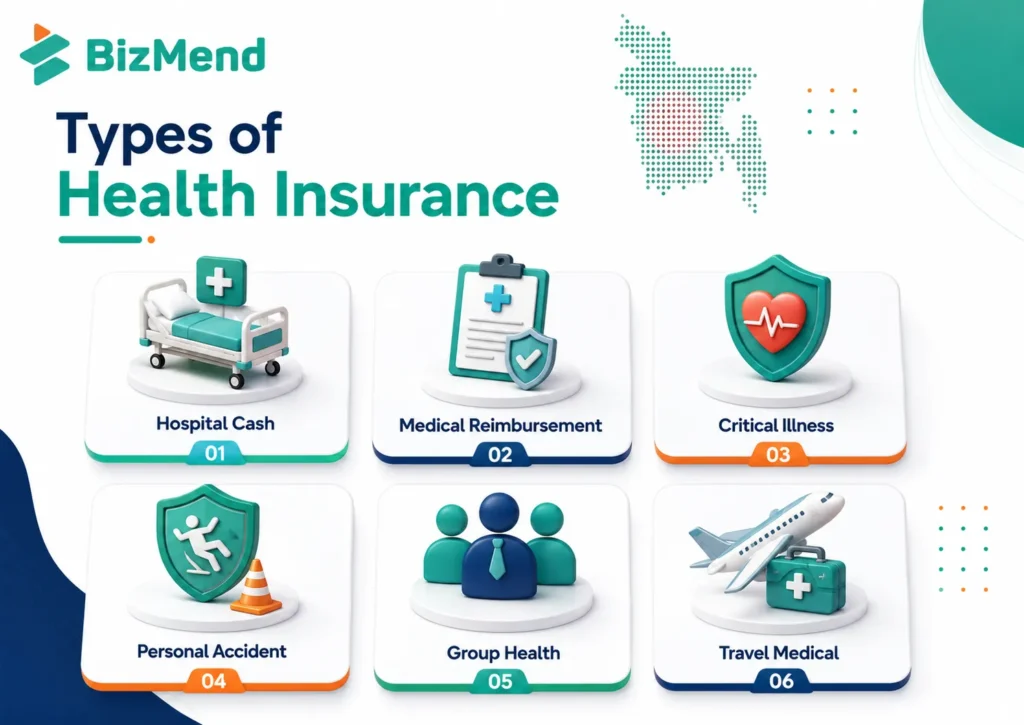

Health insurance is not one identical product. In Bangladesh, the term can refer to medical reimbursement, hospital cash, critical illness payout, accident and sickness cover, employee group medical benefits, or a health rider attached to a life insurance policy.

The market is regulated by the Insurance Development and Regulatory Authority, or IDRA. Before choosing any policy, confirm that the insurer is licensed and that the exact plan name, benefit limit, premium, exclusions, and claim process are written in the policy documents.

The need is real because many households still pay a large share of medical costs directly. World Bank data shows out-of-pocket spending made up about 69.13% of Bangladesh’s current health expenditure in 2023, while the Health Care Financing Strategy 2012-2032 aims to improve financial protection and move toward wider health coverage.

Most buyers should start by identifying the product type. A low premium can look attractive until you realize it pays only a small daily cash amount, not the full hospital bill.

| Plan type | How it usually works | Best fit | Watch carefully |

| Hospital cash or hospital care | Pays a fixed amount per covered hospital stay or day | Families wanting income support during admission | Daily caps, minimum stay, excluded illnesses |

| Medical reimbursement | Pays eligible medical expenses up to limits | Employees, families, and higher-income buyers | Room rent, co-pay, hospital network, documentation |

| Critical illness | Pays a lump sum after diagnosis of listed diseases | Buyers worried about cancer, stroke, heart attack, kidney disease | Disease definitions, survival period, stages covered |

| Personal accident and health | Covers accident-related injury, disability, or related benefits | Workers, commuters, small business owners | Accident definition, disability schedule, exclusions |

| Group health insurance | Employer or organization covers employees and dependents | Companies, NGOs, schools, and larger teams | Dependents, maternity, waiting periods, renewal pricing |

| Travel or overseas mediclaim | Covers medical emergencies abroad | Travelers, students, business visitors | Destination rules, visa needs, emergency assistance |

For many households, the practical choice is a combination: one plan for hospital admission support, one critical illness layer, and a separate life insurance policy for family income protection. If you are comparing life cover separately, Bizmend’s guide to life insurance in Bangladesh is the better place to handle death benefit, maturity benefit, and savings-style policies.

The phrase “top health insurer BD” should be treated carefully. A company can be strong in group medical, another can be better for low-cost accident cover, and another may appear among the best life insurance companies in Bangladesh for life-linked health riders. Do not choose only from a ranked list.

MetLife Bangladesh lists several health and protection options, including MetLife Critical Illness Insurance with Return of Premium, Critical Illness Insurance Protection Plan, MediCare, Critical Care, and Hospital Care. Its site also shows online claims submission, claim forms, and group medical plan options, which makes it easier for buyers to understand service channels before purchase.

Green Delta Insurance lists Shurokkha All Rounder and Shurokkha 365 under health-related products. Public product pages and bancassurance listings show low-ticket coverage examples, claim-document rules, OPD/IPD limits, waiting periods, and claim timelines, but buyers should verify the current premium and benefit table before purchase. These products may suit buyers looking for simple, affordable protection, but the written limits matter.

Pragati Life Insurance lists a health insurance product that covers hospital bills and treatment-related expenses before and after hospitalization, along with life insurance coverage. Pragati Insurance PLC may still be relevant for non-life products, but this health-insurance example should be verified against the exact company and policy document before publication.

Guardian Life is another name to compare for life-linked health and employer benefits. Public pages reference Guardian health insurance, corporate group life and health insurance, and critical disease benefits. Because some Guardian pages require JavaScript, confirm the latest benefit schedule directly from its official documents or office before relying on web summaries.

Individual health insurance is bought by one person or family. You choose the plan, pay the premium, keep the documents, and manage claims yourself. This gives control, but underwriting and exclusions can be stricter.

Corporate health insurance is arranged by an employer, association, school, NGO, or business, and employers should also understand basic labour law in Bangladesh when designing employee benefits. It can cover employees, spouses, children, and sometimes parents depending on the contract. Larger groups may get better pricing or broader terms than a single buyer.

Business owners should compare group medical cover separately from personal family cover. A small company may need employee medical benefits, group life, accident cover, clear renewal terms, and awareness of the legal requirements for starting a business in Bangladesh. If you are still structuring a cross-border company from Bangladesh, Business Globalizer’s guide on how to start a business in the USA from Bangladesh can help with business setup context, but health insurance selection should remain based on Bangladesh insurer documents.

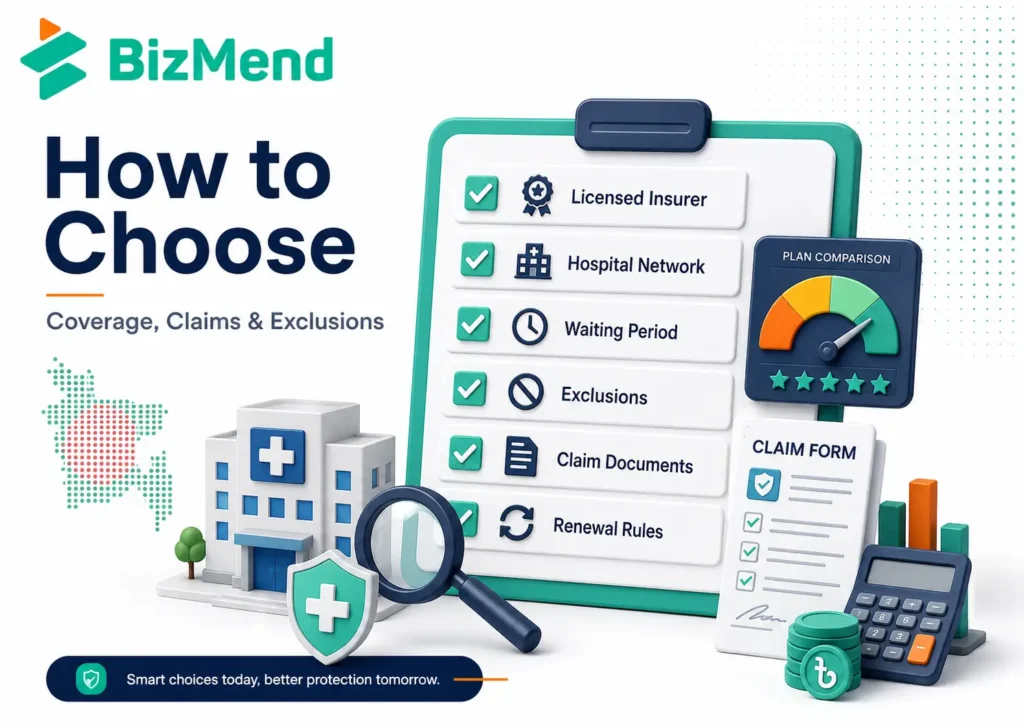

A good hospital insurance plan BD buyers can trust should be clear about exactly what it pays. If the policy wording feels vague before purchase, it may become harder during a claim.

Look for these core items:

Do not assume “comprehensive” means everything is covered. Ask for the policy schedule, benefit table, exclusions, waiting periods, claim form, and required documents before paying.

Exclusions decide what the insurer will not pay for. They are not small print; they are the real boundary of your protection.

Common items to check include pre-existing conditions, maternity, dental treatment, cosmetic treatment, mental health care, congenital conditions, self-inflicted injury, substance-related injury, outpatient treatment, and treatment outside approved hospitals. Some plans also exclude specific diseases for a waiting period.

Limits are just as important. A plan may cover surgery but cap the amount. It may cover hospital stay but pay only a fixed daily cash benefit. It may mention OPD but restrict doctor fees, diagnostics, and medicine under separate small caps.

Ask three direct questions: What is never covered? What is covered only after a waiting period? What is covered but capped? If the answer is not written, do not treat it as part of the policy.

The claim process depends on the product. A fixed hospital cash plan may need proof of admission and discharge. A reimbursement plan may need original bills, prescriptions, diagnostic reports, discharge certificates, NIDs, policy documents, and the completed claim form.

For group health plans, the HR or benefits team may collect documents and submit them to the insurer or third-party administrator. For individual policies, the policyholder usually submits through a branch, online portal, app, email, or claim desk.

Use this simple sequence:

Never change medical facts to fit a policy. Wrong information can delay the claim, reduce the payout, or void the policy.

The best health insurance company in Bangladesh for you is the one that combines solvency, service, coverage, and fit. Brand reputation helps, but policy wording decides the outcome.

Compare at least three insurers using the same questions:

If an agent answers only with promises, slow down. A clear policy document is more valuable than a confident sales pitch.

A young salaried person may start with employer group medical cover, then add personal hospital cash or critical illness protection if the employer plan is small. The goal is to avoid a single hospital event wiping out emergency savings.

A family with children should compare family eligibility, pediatric hospitalization, diagnostic support, OPD limits, and whether both parents can be covered. If maternity matters, confirm it specifically; many plans exclude or limit it.

A small business owner should look beyond personal cover. Employee group medical insurance can support retention, reduce emergency salary advances, and create a clearer benefits structure, especially when the business is also planning to start a business in the USA from Bangladesh. Still, the business should compare renewal pricing, dependent coverage, and claim handling before committing.

A frequent traveler should separate local medical insurance from overseas medical insurance or travel insurance. Local health plans usually do not replace destination-specific travel medical requirements.

The best health insurance in Bangladesh is the plan that fits your medical risk, budget, hospital preference, family size, and claim comfort. Compare MetLife, Green Delta, Pragati Life, Guardian Life, and other licensed insurers by written benefits, exclusions, network hospitals, claim documents, renewal rules, and current IDRA status rather than slogans.

Yes, family coverage is available in different forms, but the structure varies. Some plans cover spouse and children; some allow dependent parents; others are individual-only. Always check age limits, dependent definitions, and renewal rules.

Not always. Many plans exclude pre-existing conditions, cover them only after a waiting period, or require underwriting. Ask for the exact definition and written treatment before buying.

Sometimes yes. Non-life insurers and digital products may offer standalone health, accident, or hospitalization products. Life insurers may offer health riders attached to life policies. Confirm whether the product is standalone or linked.

Common documents include claim form, policy information, NID, hospital admission record, discharge certificate, prescriptions, diagnostic reports, invoices, receipts, and payment proof. The exact list depends on the insurer and product.

It can be better for employees because group pricing and underwriting may be easier. Individual insurance gives more personal control and portability. The better option depends on benefit limits, renewal, dependents, and job stability.

Health insurance in Bangladesh is worth comparing before a medical emergency forces rushed decisions. Start with the risk you need to cover, then compare insurers by licensed status, plan type, hospital access, exclusions, claim documents, and renewal rules. MetLife, Green Delta, Pragati, Guardian Life, and other licensed insurers can all be relevant, but not for the same buyer or the same medical need. The safest approach is simple: shortlist a few credible companies, ask identical questions, read the policy wording, and choose the plan that is clearest on claim day.

Learn how to become a Daraz seller in Bangladesh, register an account, list products, understand fees, manage orders, and grow…

Compare the cost of living in Bangladesh in 2026, including Dhaka and Chittagong rent, food, transport, utilities, inflation, and monthly…

Learn MoA and AoA requirements in Bangladesh, key clauses, drafting basics, RJSC filing steps, amendments, and common company-registration mistakes. Suggested…