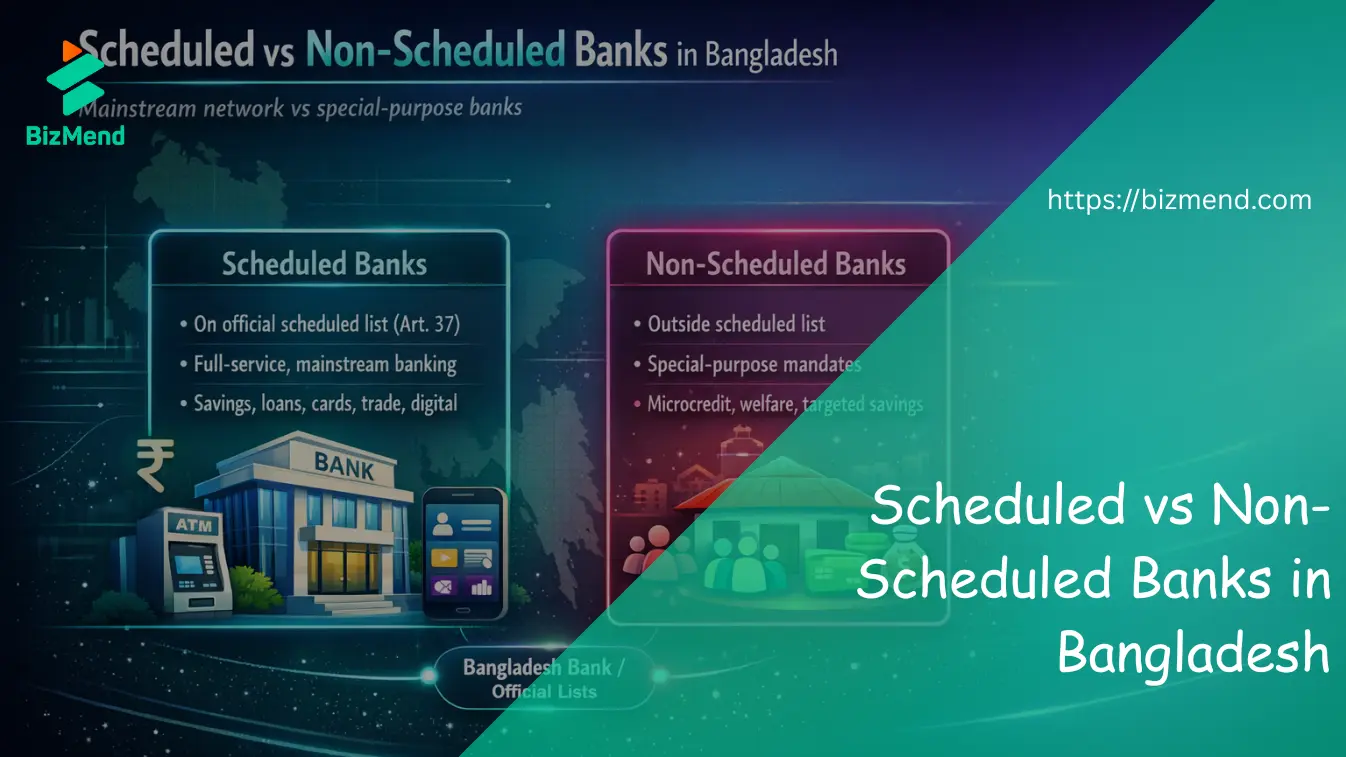

In Bangladesh, a scheduled bank is a bank that is included in the official “scheduled banks” list maintained under Article 37 of the Bangladesh Bank Order, 1972.

A non-scheduled bank is basically a bank outside that scheduled list, usually created for special, specific objectives (so it typically doesn’t offer the full range of services you expect from commercial banks). In this guide on Scheduled vs Non-Scheduled Banks in Bangladesh, we break down what that actually means

If you’re a customer, business owner, or salary account holder, this matters because “scheduled” status is tied to how the bank fits into the regulated banking system and what it can generally do.

What is a “Scheduled Bank” in Bangladesh?

The official meaning (Bangladesh Bank Order, 1972)

The Bangladesh Bank Order, 1972 defines a “Scheduled Bank” as a bank that is included in the list of banks maintained under Article 37. In other words, “scheduled” is not just a marketing word—it’s a formal status tied to a central bank–maintained list. (BB)

Why this status exists (plain English)

Think of scheduled banks as the mainstream banking network , the banks that operate under the core banking framework and are part of the standard regulated banking ecosystem. Bangladesh Bank also publishes regular statistical publications that list scheduled banks currently operating, reinforcing that this list is maintained and updated over time.

What is a “Non-Scheduled Bank” in Bangladesh?

Simple definition (what they are built for)

A non-scheduled bank is generally a bank that is not on the scheduled list, and often exists to serve a special purpose (for example, microcredit, welfare lending, or a targeted savings program). Bangladesh Bank itself publishes statistical tables specifically for non-scheduled banks, which shows the category is recognized in official reporting. (BB)

Why non-scheduled banks exist (the “special-purpose” angle)

Non-scheduled banks are usually created to solve a specific problem (financial inclusion for a target group, employment generation, rural savings, etc.) rather than to behave like full-service commercial banks.

Scheduled vs Non-Scheduled Banks

| Topic | Scheduled Banks | Non-Scheduled Banks |

| Status | Included in the scheduled list under Article 37 | Outside the scheduled list |

| Typical role | Full-service mainstream banking | Special-purpose banking |

| Scope of services | Broad (retail + corporate banking activities) | Often limited to specific functions |

| Regulatory framework | Core banking regulation & supervision ecosystem | Often governed by specific acts/special rules + narrower scope |

| Where to verify | Bangladesh Bank publications/lists | Bangladesh Bank publications + bank’s founding act / official info |

Tip: Don’t rely on “brand reputation” alone. Always verify the status using official sources (I’ll show how below). (BB)

Most Important Differences between Scheduled & Non Scheduled Banks

Licensing and recognition (the “scheduled list” factor)

The cleanest difference is this: scheduled banks are formally recognized by inclusion in the scheduled list maintained under Article 37.

That recognition is a big reason why “scheduled bank” is treated as the standard banking category in Bangladesh.

What services they can offer (full-service vs targeted)

Most people experience scheduled banks as “normal banks” because they typically provide the broad menu: savings/current accounts, cards, loans, trade services, digital banking, corporate services, etc.

Non-scheduled banks are often more focused—designed to deliver specific products or services rather than everything under one roof. (BB)

Supervision and compliance expectations (what changes for customers)

Scheduled banks sit right inside the standard banking ecosystem that Bangladesh Bank oversees through laws and regulations. For example, the Bank Company Act includes provisions that distinguish requirements for banking companies that are “not being a scheduled bank” in certain contexts (showing the law treats the two categories differently). (BB)

Practically, customers usually feel this difference through product range, system integration, and institutional structure—not through day-to-day paperwork.

System privileges (clearing, settlement, interbank participation)

Without getting too technical: scheduled banks are usually the ones that participate fully in the mainstream interbank and payment/clearing infrastructure as part of the formal scheduled network.

Non-scheduled banks may operate with narrower rails depending on their legal setup and scope. (This is one reason many non-scheduled institutions feel “specialized.”)

Customer perception vs reality: is “scheduled Banks” = safe?

A common misconception is: scheduled bank = 100% safe.

Reality: scheduled banks are regulated and integrated into the mainstream system, but no bank is risk-free. That’s exactly why deposit protection rules exist.

For example, in October 2025, news reports said the government approved a draft Deposit Protection Ordinance, 2025, proposing to raise deposit protection from Tk 100,000 to Tk 200,000 if a bank/financial institution is liquidated (always check the latest legal status and implementation). (bdnews24.com)

Why the list can change (mergers + new approvals)

Banking systems evolve: banks merge, restructure, and policy changes happen. Bangladesh Bank’s scheduled-bank publications list “scheduled banks currently operating,” which implies the “current list” can be updated over time. (BB)

Who should care (real-life situations)

You should care about scheduled vs non-scheduled status if you’re:

- opening a salary account,

- using business banking (payments, trade, collections),

- relying on digital services and wide ATM/branch networks,

- comparing bank stability and system participation,

- deciding where to keep larger operational balances.

If you want the full official-style list, use your pillar page (“scheduled banks in Bangladesh”) and keep this post as your decision guide.

Examples of Non-Scheduled Banks in Bangladesh (as examples)

Bangladesh has a small number of non-scheduled banks that are often cited as examples, such as Grameen Bank, Ansar VDP Unnayan Bank, Karmasangsthan Bank, Palli Sanchay Bank, and (historically) Jubilee Bank—but statuses can change, so treat examples as examples and always verify. (Wikipedia)

How to Check if a Bank is Scheduled in Bangladesh (Fast Checklist)

Use this quick process:

- Check Bangladesh Bank publications that list scheduled banks currently operating (a reliable approach because it’s regularly published). (BB)

- Look for the bank under the correct category (state-owned, specialized, private, foreign, etc.). (BB)

- If the bank is not there, check whether it is a special-purpose bank and review its official background (founding act / official page).

- When in doubt, cross-check with Bangladesh Bank reporting that covers non-scheduled banks as a separate category. (BB)

FAQs

What is the main difference between scheduled and non-scheduled banks in Bangladesh?

Scheduled banks are included in the scheduled list under Article 37; non-scheduled banks are outside that list and are often special-purpose institutions.

Who declares a bank as “scheduled” in Bangladesh?

The concept is defined in the Bangladesh Bank Order, 1972, and scheduled status is tied to inclusion in the list maintained under Article 37.

Do non-scheduled banks offer all normal banking services?

Usually no. Many exist for specific objectives, so services can be narrower than mainstream commercial banks.

Are all private commercial banks in Bangladesh scheduled banks?

Most mainstream private commercial banks are treated as scheduled within Bangladesh Bank’s scheduled-bank publications, but you should verify using official lists/publications.

Can a bank be removed from the scheduled list?

Banking status can change due to restructuring, mergers, or regulatory actions. That’s why it’s best to rely on the latest Bangladesh Bank publications and updates.

Does “scheduled bank” mean my money is 100% safe?

No bank is risk-free. Deposit protection rules exist to protect depositors up to a limit if liquidation happens (and limits/rules can change over time).

Why does the scheduled bank list change over time?

Because banking systems change—new banks, mergers, and regulatory updates. Bangladesh Bank publications reflect the “currently operating” scheduled banks.

How can I verify if my bank is scheduled?

Check Bangladesh Bank scheduled-bank publications (like quarterly scheduled bank statistics) and confirm the bank appears in the list. (BB)

What are some examples of non-scheduled banks in Bangladesh?

Commonly cited examples include Grameen Bank, Ansar VDP Unnayan Bank, Karmasangsthan Bank, and Palli Sanchay Bank (verify current status from official sources).