Sole Proprietorship in Bangladesh: Registration, Tax & Compliance

Everything a Bangladeshi founder needs to register a sole proprietorship: trade license fees, e-TIN, BIN thresholds, tax slabs, and yearly…

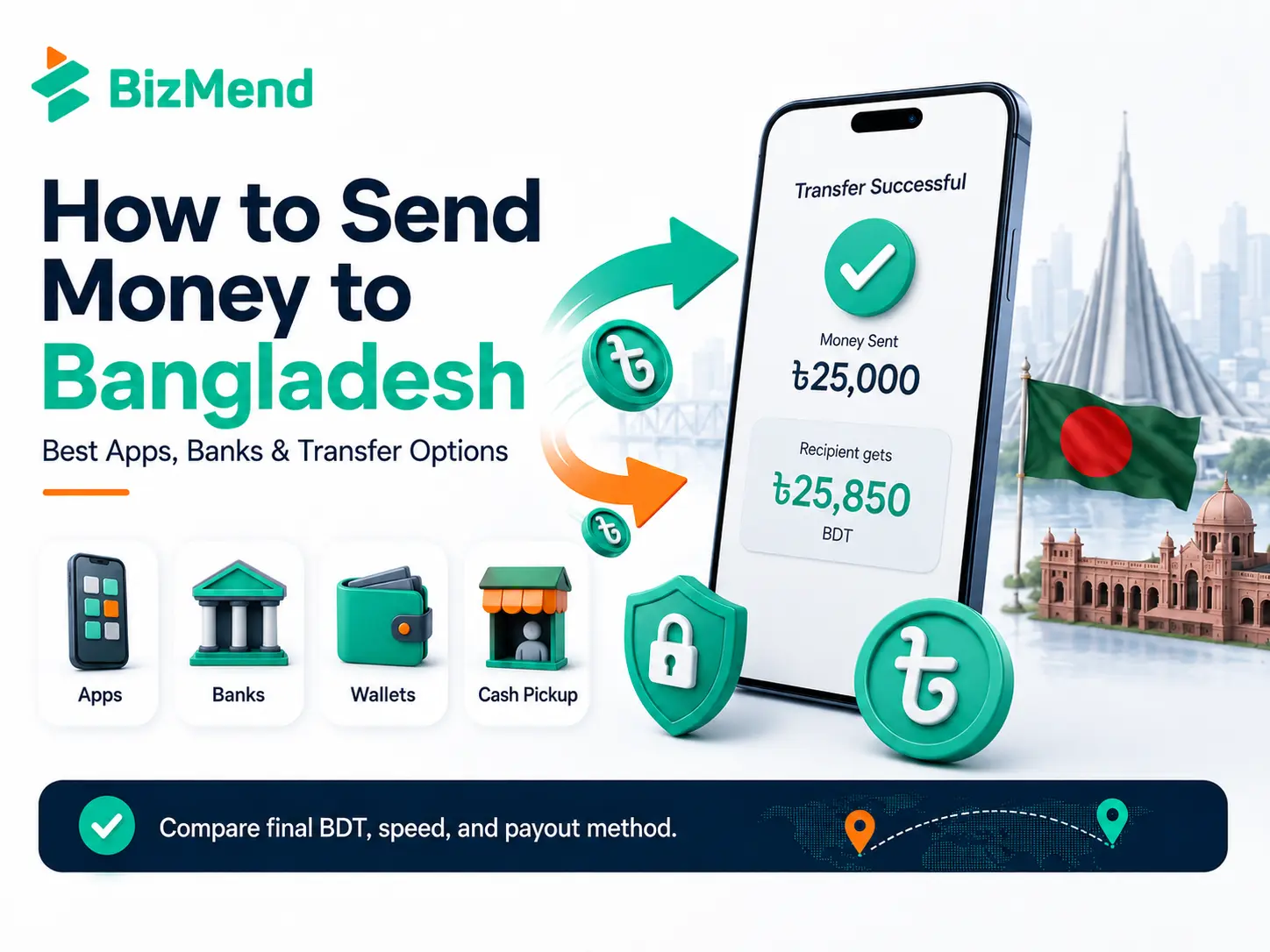

Send money to Bangladesh with clear comparisons of apps, banks, cash pickup, mobile wallets and wires, plus fee and speed checks.

Sending taka home should not feel like guesswork. If you need to send money to Bangladesh, the hard part is rarely finding an app. The hard part is knowing which route gives your recipient the most usable BDT.

Apps, banks, exchange houses, and cash pickup networks can all work, but they price transfers differently. Some show a low fee and earn through the exchange rate. Others cost more but solve a real problem, like rural cash pickup, urgent delivery, or a traceable bank account deposit. This guide walks through the practical choices so you can compare speed, cost, limits, and recipient convenience before you send.

Most Bangladesh remittance routes have three moving parts: how you pay, how the provider converts the money, and how your recipient receives BDT. You might pay with a bank account, debit card, credit card, cash, or an app balance. The recipient might receive a bank deposit, wallet credit, or cash pickup.

For everyday family support, digital remittance apps are often the most convenient starting point. They show the exchange rate, fee, transfer time, payout method, and recipient amount before you confirm. Still, every route has limits. A debit card transfer may be faster. A bank-funded transfer may be cheaper. A cash pickup may solve access problems.

Bangladesh also has a strong formal remittance system through banks, money transfer operators, exchange houses, and mobile financial services. bKash says remittances sent through legal channels qualify for a 2.5 percent government incentive, subject to the route and rules in place. That incentive is one more reason to avoid informal channels.

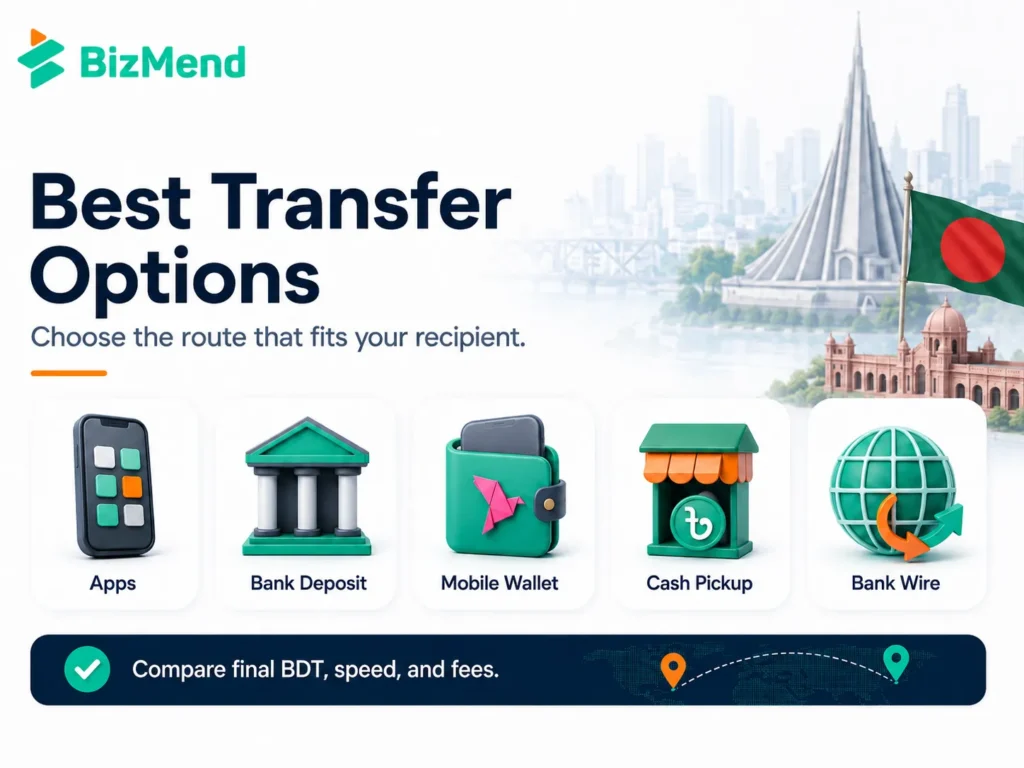

Think of the transfer option as a fit question, not a brand question. The same provider can be great for one recipient and awkward for another. A Dhaka bank account, a Sylhet cash pickup, and a village bKash wallet are three different jobs.

| Option | Best fit | Watch before sending |

|---|---|---|

| Money transfer apps | Regular family support, fast comparison, mobile-first senders. | Fees, exchange rate, wallet limits, and sender-country access. |

| Bank deposit | Savings, rent, tuition, medical bills, larger support. | Correct bank name, branch details, account number, and posting time. |

| Mobile wallet | Recipients who already use bKash, Nagad, or Rocket. | Wallet number, registered name, daily and monthly limits. |

| Cash pickup | Recipients without easy bank access or urgent cash needs. | Valid ID, pickup network, reference number, and branch hours. |

| International bank wire | Higher-value transfers, formal payment records, businesslike documentation. | Wire fee, intermediary charges, exchange rate, and several business days. |

That comparison gives you the real question: what does your recipient need the money to do today? If the answer is groceries, bKash may beat a wire. If the answer is university payment, a bank deposit may beat cash.

Wise is strong for transparent pricing and account-style transfers. Its BDT guide says you can send to Bangladesh bank accounts, bKash accounts, and Nagad accounts, with separate limits for bank and wallet transfers. Wise also states that business transfers to BDT are not currently supported, so treat it mainly as a personal remittance option.

Remitly, Taptap Send, Sendwave, and similar app-first providers can be useful when speed and wallet delivery matter. Remitly lists cash pickup, bank deposit, and mobile wallet delivery for Bangladesh, including bKash, Nagad, and Rocket. Taptap Send lists transfers to any Bangladeshi bank, selected cash pickup partners, and bKash, Nagad, or Rocket.

Western Union, MoneyGram, Ria, WorldRemit, and Xoom are better when the recipient needs broad pickup coverage, a bank deposit, or a familiar global brand. Xoom is especially useful for some PayPal users, since it supports cash pickup, bank deposit, and bKash wallet transfers to Bangladesh from selected countries.

A good remittance app is not the one with the loudest promise. It’s the one that fits your recipient.

An international wire to Bangladesh sends money from your bank to the recipient’s bank account, usually through SWIFT and sometimes through correspondent banks. It can work well for larger transfers, school fees, home payments, family support that needs a paper trail, or situations where the recipient’s bank asks for formal account credit.

The sender usually needs the recipient’s full legal name, bank name, branch information, account number, address details, and sometimes a SWIFT code or routing details. The bank may ask for the purpose of payment, source of funds, or relationship to the recipient. That is normal for regulated transfers.

The tradeoff is cost and timing. A wire may include a sending bank fee, a receiving bank fee, and intermediary bank deductions. The exchange rate may also be weaker than a remittance app. For smaller family transfers, that can feel like buying a whole suitcase for one shirt.

A wire is best when the paper trail matters more than speed.

Mobile wallet delivery is often the most practical way to send money to Bangladesh for daily household use. The recipient receives BDT into a wallet account, then uses it for payments, transfers, mobile recharge, cash out, or bank-linked services depending on the wallet and account level.

bKash says expatriate Bangladeshis can remit to bKash through authorized and listed banks, exchange houses, and money transfer operators. Its remittance page also says recipients of legal-channel remittances receive the current 2.5 percent government incentive and that ATM cash-out for remittance can be available at 7 taka per thousand through specified ATM networks.

Wallet convenience depends on details. The sender must enter the correct mobile number and registered name. Provider limits may differ from wallet limits. Wise, for example, lists specific BDT limits for bank, bKash, and Nagad transfers. Always check the live limit before splitting or repeating transfers.

Cash pickup sounds old-fashioned until the recipient actually needs cash today. It can be useful for older relatives, rural areas, emergency support, or families who trust a known agent counter more than a new app screen.

Western Union lists Bangladesh receipts through cash pickup, bank account, and bKash account. Ria lists cash pickup, bank deposit, and mobile wallet delivery, with a large Bangladesh partner network. MoneyGram also shows Bangladesh receive options such as bank account, cash pickup, and mobile wallet, where available.

The recipient usually needs a valid photo ID, sender name, expected amount, pickup location, and transfer reference such as an MTCN, PIN, or order number. Do not share that reference with anyone except the actual recipient. If a stranger asks for it, stop there.

Start with the final BDT amount, not the advertised fee. A transfer with a zero fee can still cost more if the exchange rate is weaker. The World Bank’s remittance price work treats cost as more than a single fee because exchange margins and payout terms matter too.

Use the same test amount across providers, then compare what the recipient gets. Try one smaller amount, such as 100 dollars, pounds, euros, or dirhams, and one larger amount you might actually send. Some providers become cheaper as the transfer grows. Others stay expensive because card fees or cash pickup fees stay in the mix.

Use this quick checklist before you pay:

A clean transfer starts with clean recipient details. For a bank deposit, confirm the full account name, bank name, branch, account number, and any routing or SWIFT details the provider asks for. Bangladesh account numbers and branch details can be unforgiving when entered casually.

For bKash, Nagad, or Rocket, confirm the wallet number and the registered name before sending. Do not guess from a contact list. If the app warns that an incorrect wallet number may be hard to reverse, take that warning seriously.

For cash pickup, ask the recipient which pickup partner is realistic for them. A slightly worse exchange rate may be worth it if the nearest pickup point is close, open, and familiar. Recipient convenience is part of the price.

Use a mobile wallet when the recipient needs quick household money and already uses bKash, Nagad, or Rocket. Use a bank deposit when the money is larger, formal, or meant for savings and bills. Use cash pickup when the recipient needs physical taka or has weak account access.

Use a bank wire when you need a formal record, your bank requires it, or the amount is large enough that a fixed wire fee hurts less. For ordinary monthly support, start with regulated remittance apps first, then compare banks only if the math or paperwork justifies it.

Most senders should keep two reliable routes: one cheap everyday option and one backup option for urgent cash or app outages. That way, you’re not learning the whole system while someone at home is waiting for medicine money.

The best way to remit to BD depends on the recipient, amount, timing, and proof you need. Compare the final BDT amount, not just the fee. For most family transfers, apps and mobile wallets are practical. For larger or formal payments, a bank deposit or wire may fit better. Check live rates and limits every time.

Usually, the cheapest route is the one with the strongest final BDT amount after fees and exchange-rate markup. Test the same amount through Wise, Remitly, Taptap Send, Ria, Western Union, MoneyGram, Xoom, and your bank before sending.

Yes, many providers support bKash remittances, but availability depends on your sender country and provider. Wise, Remitly, Western Union, Ria, Xoom and Taptap Send a list of all Bangladesh wallet or bKash routes in some form. Check the live route before paying.

A wire can be better for larger transfers, formal records, or bank-requested payments. For regular family support, apps often win on speed and transparency. The wire may still cost more because of sender fees, exchange-rate markup, receiving charges, or intermediary deductions.

Some wallet and cash pickup transfers can arrive within minutes, while bank deposits can take longer depending on provider review, bank posting, holidays, and payment method. Wise says BDT bank transfers can take up to 3 working days after conversion. Always use the estimate shown at checkout.

Current provider and bKash guidance still refers to a 2.5 percent government cash incentive for eligible inward wage remittances sent through legal channels. The rules can change, and documents may be needed for larger transfers, so verify the latest terms with the provider or receiving bank.

Everything a Bangladeshi founder needs to register a sole proprietorship: trade license fees, e-TIN, BIN thresholds, tax slabs, and yearly…

Learn how Rocket mobile banking works in Bangladesh, including features, cash-out charges, account setup, limits, and safe everyday use for…

Learn how bKash merchant accounts work, what documents you need, and how shops and online sellers in Bangladesh accept payments.