Most people in Bangladesh use a bank every day – salary comes in, bills go out, maybe an FDR here and there. That’s commercial banking.

Then you hear terms like investment banking, merchant banking, IPO, bonds, and it suddenly feels like a different world.

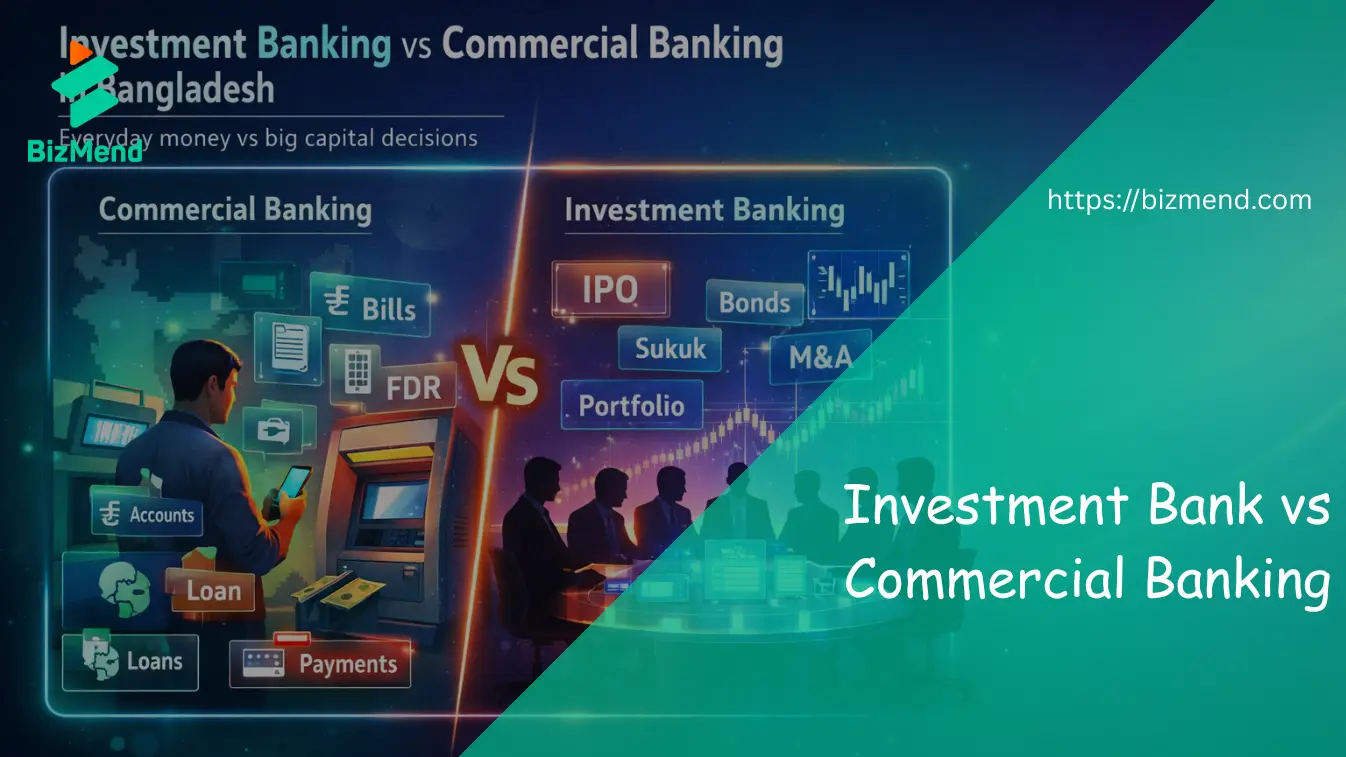

In Bangladesh, commercial banking looks after your everyday money – deposits, savings, loans, cards and payments. Investment banking (mostly called merchant banking here) helps companies and investors with big, long-term capital decisions – IPOs, bonds, sukuk, M&A and professional portfolio management.

So same “bank” word, but two very different jobs.

In this guide, we’ll break down investment banking vs commercial banking in Bangladesh in simple language, show their key differences, and help you understand which one you actually need.

Overview: Two Different Banking Roles in Bangladesh

Bangladesh has several types of financial institutions:

- Commercial banks (public, private, Islamic)

- Merchant banks (investment banking)

- NBFIs, microfinance, etc.

When we talk about investment banking vs commercial banking in Bangladesh, we’re really comparing:

- Commercial banks → everyday banking for people and businesses

- Investment / merchant banks → capital-market and advisory services for larger funding and investment needs

You will likely use commercial banking from day one of your career or business.

You typically meet investment banking later, when your capital needs get bigger or your investments become more serious.

What Is Commercial Banking in Bangladesh?

Core Commercial Banking Services

A commercial bank is what you think of as a “normal bank”. It focuses on:

- Accounts

- Savings accounts

- Current accounts

- FDRs and term deposits

- Lending

- Personal loans, home loans, car loans

- SME and corporate loans

- Overdrafts and working-capital finance

- Payments & Channels

- Cheques, BEFTN, RTGS

- Cards (debit, credit, prepaid)

- ATM network, internet banking, mobile apps

- Other services

- Remittances (inward and outward)

- Basic trade finance (LCs, bank guarantees, export/import bills)

Commercial banks are built to keep money safe, liquid and moving.

Who Uses Commercial Banking?

- Individuals: salary, savings, daily transactions, small loans

- Small shops & SMEs: business accounts, payments, overdrafts, POS terminals

- Corporates: large accounts, cash management, payroll, trade finance

If you think of monthly income, monthly bills, and standard loans, you’re firmly in commercial banking territory.

What Is Investment Banking (Merchant Banking) in Bangladesh?

Investment Banking / Merchant Banking Defined

Globally, the term is investment banking.

In Bangladesh, you’ll mostly see merchant banks and investment divisions of commercial banks doing this work.

They do not focus on salary accounts or personal loans.

Instead, they focus on:

- Helping companies and institutions raise large capital

- Helping investors invest in the capital market professionally

You can think of an investment / merchant bank as a deal architect and capital-market guide.

Key Investment Banking Services in Bangladesh

Common investment banking services include:

- Equity capital services

- IPOs (Initial Public Offerings)

- RPOs and rights issues

- Private placements (raising money from selected investors)

- Debt & sukuk services

- Corporate bonds and debentures

- Sukuk (Islamic investment certificates)

- Structured/project finance deals

- Advisory & corporate finance

- Mergers & acquisitions (M&A)

- Restructuring and turnaround plans

- Valuation and capital-structure advice

- Portfolio management services (PMS)

- Discretionary portfolios (they manage for you)

- Advisory portfolios (they advise, you decide)

- Special mandates for NRBs and institutions

Investment banking in Bangladesh sits more around DSE/CSE and capital markets, not around branch counters and ATM booths.

Who Uses Investment Banking?

- Mid to large companies planning big expansion

- Listed companies raising fresh capital or doing M&A

- Government / infrastructure projects using bonds or sukuk

- Banks & NBFIs issuing subordinate bonds or special capital instruments

- High-net-worth individuals and NRBs who want professional portfolio management

So when your money decisions move from “How do I pay this month’s bills?” to “How do I raise 200 crore?” or “How do I invest a few crore wisely?”, you move closer to investment banking.

Investment Banking vs Commercial Banking in Bangladesh – Key Differences

Let’s put them side by side in simple terms.

1. Purpose and Role

- Commercial banking:

Designed to handle everyday banking – deposits, savings, lending, payments. - Investment banking:

Designed to handle big capital decisions – raising money through shares/bonds, advising on deals, managing investments.

2. Clients and Use Cases

- Commercial banking clients:

- General public

- Micro, small and medium businesses

- Large corporates for routine banking

- Investment banking clients:

- Growing mid/large companies

- Government/large projects

- Institutions (funds, insurers, pensions)

- HNWIs, family businesses, NRBs

In short, commercial banking is about your daily cash flow.

Investment banking is about large, strategic moves.

3. Products and Services

- Commercial banking products:

- Savings/current accounts

- FDRs, loans, cards

- Remittances, simple mutual funds, basic investment products

- Investment banking products/services:

- IPOs, rights issues, private placements

- Bonds, debentures, sukuk

- M&A advisory, valuation, restructuring

- Portfolio management services (PMS)

4. Regulation and Risk Profile

- Commercial banks:

- Regulated mainly by Bangladesh Bank

- Deposit-focused, with strong rules on capital and liquidity

- From a customer view: more stable, predictable products

- Investment / merchant banks:

- Regulated mainly by BSEC and stock exchanges

- Deal and market-focused (shares, bonds, sukuk)

- Products are market-linked, so returns can rise or fall

That doesn’t mean one is “safe” and the other is “dangerous”.

It means they operate under different rules and risk profiles.

When to Use Investment Banking vs Commercial Banking in Bangladesh

For Business Owners and Founders

Use commercial banking when you need:

- Business accounts and payment handling

- Salary disbursement and vendor payments

- Working-capital loans, OD, LC facilities

- Basic trade and cash management

Use investment banking when you need:

- Large long-term capital beyond normal bank loans

- To go public via IPO or raise more equity

- To issue bonds or sukuk for projects

- To sell a stake or bring a strategic investor

- To buy another company or merge (M&A)

- To restructure heavy debt or complicated balance sheets

A healthy, growing company in Bangladesh will often start with commercial banks and later add investment banking when its ambitions and funding needs increase.

For Individual Investors and NRBs

Use commercial banking for:

- Salary income, emergency fund

- Savings, FDRs, basic recurring deposits

- Day-to-day payments, cards and remittances

Use investment banking for:

- Building a serious long-term investment portfolio

- Getting access to IPOs, bonds, sukuk

- Having a professional manage your capital through PMS

So you’ll likely keep your main accounts with a commercial bank, and route investment money through an investment/merchant bank.

How Investment Banks and Commercial Banks Work Together in Bangladesh

It’s not always “investment banking vs commercial banking in Bangladesh” like rivals.

In many cases, they work as a team.

- A commercial bank may have its own investment arm (merchant bank / capital company).

- You might have your operating accounts and loans with the bank, and your IPO, bond or PMS with its investment subsidiary.

This is good for you because:

- The group already knows your business cash flows

- Coordination between daily banking and big deals can be smoother

- You can build a long-term relationship with one financial group that grows with you

Think of it like this: commercial banking is the foundation, investment banking is the upper floors you add when you grow.

Common Misconceptions About Investment Banking vs Commercial Banking

Let’s quickly clear a few myths:

- “Investment banking is only for giant multinationals.”

False. Many mid-sized and fast-growing Bangladeshi companies use merchant banks for private placements, bonds and IPOs. - “Merchant banks are just broker houses.”

No. A broker mainly executes buy/sell orders. A merchant bank can design whole deals – IPOs, M&A, bonds, PMS, etc. - “I don’t need investment banking because I already have a bank loan.”

Loans are great for many needs, but they have limits. For big expansion, acquisition or IPO, investment banking tools can be more suitable. - “Investment banking always means IPO.”

IPO is just one service. Bonds, sukuk, M&A and portfolio management are equally important parts of investment banking in Bangladesh.

FAQs on Investment Banking vs Commercial Banking in Bangladesh

Is an investment bank safer than a commercial bank in Bangladesh?

They are safe in different ways. Commercial banks focus on deposits and loans under Bangladesh Bank rules, while investment/merchant banks handle capital-market products under BSEC. Investment products involve market risk, but both are regulated.

Can I open a savings account in an investment or merchant bank?

No. Merchant banks in Bangladesh usually don’t offer regular savings or salary accounts. You keep those with a commercial bank, and use merchant banks mainly for capital-market and advisory services.

Do all commercial banks in Bangladesh have investment banking arms?

No. Some large banks run their own merchant-banking or capital-market subsidiaries. Others only provide traditional banking. Each bank decides whether to enter investment banking or not.

When should a company start talking to an investment bank?

When your funding needs go beyond normal loans, or you’re thinking about an IPO, bond/sukuk issue, or selling/buying a company. It’s smart to talk early, not only when there’s a crisis.

Can NRBs use Bangladeshi investment banks for portfolio management?

In many cases, yes. NRBs can open special investment accounts (subject to KYC and FX rules) and use portfolio management services to invest in local shares, bonds and sukuk.

Are investment-banking fees higher than normal bank charges?

Usually yes, because deals are complex and customized. But these fees are tied to large transactions and long-term value, not to everyday services like ATM or account fees.

Do I need both a commercial bank and an investment bank as a business owner?

Most growing businesses in Bangladesh eventually use both. Commercial banks for daily operations; investment/merchant banks for big capital raising, restructuring or strategic deals.