Most importers and exporters in Bangladesh know what an LC is. Fewer understand how back-to-back LCs actually work, what the EDF does, or why a Loan Against Trust Receipt matters when your goods arrive at the port. Trade finance in Bangladesh is a full system, and if you only know half of it, you’re leaving money on the table. This guide covers every major instrument, with real numbers and verified facts.

| Quick Answer: Trade finance in Bangladesh includes letters of credit (LC), back-to-back LC, Export Development Fund (EDF) loans, packing credit, Loan Against Trust Receipt (LTR), bill purchase/discounting, and bank guarantees. All are regulated by Bangladesh Bank and facilitated through licensed Authorized Dealer (AD) banks. Exporters are required by Bangladesh Bank to repatriate foreign currency proceeds within 120 days of shipment. |

What Is Trade Finance in Bangladesh?

Trade finance is how businesses fund the gap between placing an order and getting paid. For importers, it means financing goods at the port before you’ve sold them. For exporters, it means getting cash now while you wait for the foreign buyer’s bank to settle.

The whole system runs through Authorized Dealer (AD) banks, commercial banks licensed by Bangladesh Bank to handle foreign exchange transactions. Bangladesh Bank sets the rules. AD banks execute them. Every LC you open, every EDF loan you apply for, every export bill you discount flows through your commercial bank with Bangladesh Bank’s guidelines behind each step.

Understanding how commercial banks in Bangladesh operate in trade finance will save you time and avoidable errors. And if you plan to start a business in Bangladesh with an import or export focus, your bank relationships matter from day one.

Letter of Credit (LC): The Backbone of Bangladesh Trade

An LC (Letter of Credit) is a written commitment by the importer’s bank to pay the exporter a specific amount, provided the exporter presents documents that strictly comply with the LC’s terms. All LCs in Bangladesh operate under UCP 600 (Uniform Customs and Practice for Documentary Credits, International Chamber of Commerce Publication No. 600, 2007 revision).

For imports, the process flows like this:

1. The importer applies to their AD bank with the IRC and underlying import documents such as indent, proforma invoice, purchase contract, or sales contract. LCAF registration was phased out under Bangladesh Bank FE Circular No. 29 dated October 20, 2022.

2. The issuing bank transmits the LC via SWIFT to the exporter’s advising bank abroad.

3. The exporter ships the goods and presents complying documents (commercial invoice, bill of lading, packing list, certificate of origin, and any other documents required by the LC).

4. The issuing bank pays upon receipt of strictly complying documents.

Banks deal in documents, not goods. That principle from UCP 600 is what makes LCs work, and also what makes document discrepancies so costly.

Types of LC Used in Bangladesh

Sight LC: Payment is made immediately when the exporter presents complying documents. No credit period for the importer.

Usance LC (Deferred Payment): The importer gets a credit period, typically 90 or 180 days from bill of lading date, before payment is due.

UPAS LC (Usance Payable At Sight): The exporter receives payment at sight (immediately upon presenting documents), while the importer repays the issuing bank at the end of the usance term. For raw materials, UPAS is typically structured for up to 180 days. For capital machinery, terms can extend to 720 days.

Back-to-Back LC: The garment sector’s primary tool, covered in the next section.

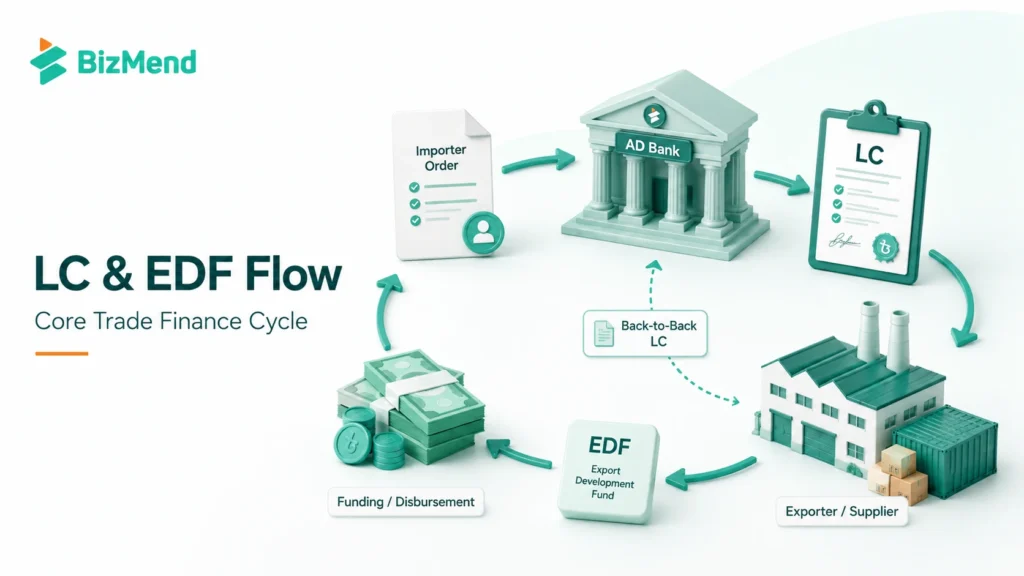

Back-to-Back LC: How the RMG Sector Finances Raw Materials

Back-to-back LC (BTB LC) is how most of Bangladesh’s garment exporters finance raw material imports without draining their own capital.

Here’s the logic: a garment factory receives a master export LC from a foreign buyer. The factory’s AD bank uses that master LC as security to open a second LC (the back-to-back LC) in favor of the fabric or accessories supplier. The supplier ships the inputs. When the garment factory ships finished goods and receives export payment, those proceeds settle the BTB LC.

Around 55% of Bangladesh’s garment exports are handled through back-to-back LCs (Global Trade Review, 2022). It lets factories source billions of dollars of fabric and trims without needing matching cash reserves.

Bangladesh Bank also allows inland back-to-back LCs denominated in foreign exchange for local input deliveries. A garment accessories maker supplying trims to a garment factory can receive payment in foreign currency under an inland BTB LC, which counts as a deemed export.

Export Development Fund (EDF): Bangladesh Bank’s Foreign Currency Window

The EDF (Export Development Fund) is a foreign currency refinancing facility administered directly by Bangladesh Bank. It was established in 1989 through an agreement with the International Development Association (IDA) to support the export sector’s raw material financing needs.

The mechanism: an eligible manufacturer-exporter opens a sight back-to-back LC to import raw materials. Their AD bank pays the foreign supplier. The AD bank then borrows US dollars from Bangladesh Bank’s EDF to cover that payment, on-lending those funds to the exporter in foreign currency.

Key EDF facts (sourced from Bangladesh Bank and the World Bank Bangladesh Development Update, April 2024):

| Metric | Detail |

| EDF size | EDF size has changed significantly; recent reporting places it around USD 2.2 billion, with discussions about gradual expansion. Always verify current EDF availability with the AD bank. |

| Maximum per exporter | USD 10 million (reduced from USD 15 million) |

| Loan tenor | 180 days from disbursement |

| Extended tenor | Up to 270 days with Bangladesh Bank approval |

| Penalty on overdue | 4% per annum, debited from AD bank’s FC clearing account |

| Eligibility | Manufacturer-exporters; also producers of intermediate goods (deemed exports) |

The EDF was significantly restructured between 2022 and 2024 due to foreign exchange reserve pressures and IMF conditionality. The facility’s exact terms are updated periodically by Bangladesh Bank’s Foreign Exchange Policy Department (FEPD). Always confirm current terms with your AD bank before applying.

Pre-Shipment Finance: Packing Credit and Export Cash Credit

Once you have an export LC or a confirmed firm export contract, two instruments help you finance production before goods ship.

Packing Credit (PC): A short-term credit facility given to exporters against export LC or firm contract, to cover costs of manufacturing, processing, and packing goods for export.

Key terms confirmed by Bangladesh Bank circulars and commercial bank disclosures:

- Rate: Pre-shipment export credit rates should be verified with the current Bangladesh Bank circular and the exporter’s AD bank. Bangladesh Bank later moved pre-shipment export credit pricing to a reference-rate-based framework, and eligible exporters may access lower-cost pre-shipment support under specific Bangladesh Bank funds.

- Maximum tenure: 120 days (extendable to 180 days under Bangladesh Bank’s export refinancing scheme)

- Amount limit: Packing credit limits vary by bank, product, export arrangement, and Bangladesh Bank rules. Total pre-shipment finance is usually linked to the FOB value of the export LC or firm contract and should be confirmed with the AD bank.

- Must be adjusted from the relevant export proceeds.

Export Cash Credit (ECC): Similar to PC but structured as a revolving credit facility. Supplements an exporter’s working capital for genuine export costs.

If you’re choosing a bank for packing credit, the best private banks in Bangladesh guide covers which banks are most responsive to export-oriented businesses.

Post-Shipment Finance: LTR, Bill Purchase, and Discounting

Loan Against Trust Receipt (LTR)

LTR is the standard post-import financing tool in Bangladesh. After imported goods arrive and the bank receives shipping documents, instead of paying the full LC amount upfront, the importer takes a Loan Against Trust Receipt. The importer holds the goods “in trust” for the bank, sells them, and repays the loan from sales proceeds.

Key LTR terms per Bangladesh Bank guidelines:

- Tenure: 30 to 180 days depending on the nature and marketability of goods

- Consumer goods: Maximum 90 days per Bangladesh Bank circular

- Security: Hypothecation of imported goods

- Drawing is allowed once per LTR; no further drawing is permitted under the same LTR.

FDBP and Bill Discounting for Exporters

FDBP (Foreign Documentary Bill Purchase): Your AD bank purchases your export bills drawn under an LC, paying you the negotiated amount immediately. The bank takes on the payment risk from the foreign issuing bank. FDBP converts shipped goods into immediate working capital, provided the submitted documents comply with LC terms.

Bill Discounting (for usance bills): If your LC is on usance terms, the foreign bank issues an acceptance. You can discount that acceptance through your AD bank or offshore banking unit (OBU), receiving funds now minus a discount charge. Bangladesh Bank limits the all-in-cost of foreign currency bill discounting to a ceiling set by FEPD.

For exporters working with global buyers, top foreign banks in Bangladesh like Standard Chartered and HSBC often offer more competitive bill discounting rates due to their international correspondent networks.

Bank Guarantees in Trade Finance

Bank guarantees are non-funded instruments. Your bank promises to pay if you fail to perform. In Bangladesh trade finance, guarantees are used at every stage of contracting and project execution.

| Guarantee Type | Purpose |

| Bid Bond (BB) | Assures a tender-issuing authority you’ll honor your bid if selected |

| Performance Guarantee (PG) | Confirms you’ll complete a contract as agreed |

| Advance Payment Guarantee (APG) | Protects a buyer who pays in advance; bank refunds if you fail to deliver |

| Payment Guarantee | Guarantees payment to a foreign supplier in lieu of LC |

AD banks in Bangladesh can issue foreign bank guarantees to beneficiaries abroad through their correspondent bank networks, and receive counter-guarantees from overseas banks for foreign parties doing business in Bangladesh.

Common Mistakes to Avoid in Trade Finance

5. Document discrepancies in LC. The number one reason for delayed payment under LC is documents that don’t strictly match LC terms. A date format difference, an incorrect product description, or any mismatch can trigger a discrepancy. Banks check documents against the LC terms under UCP 600, not against the actual goods.

6. Applying for EDF without confirming eligibility. EDF is for manufacturer-exporters with valid export LCs or firm contracts. Trading companies, indentors, and service exporters generally don’t qualify.

7. Misunderstanding LTR tenor limits. For consumer goods, Bangladesh Bank caps LTR at 90 days. Rolling LTR repeatedly without repayment creates forced loans that damage your credit history.

8. Missing the 120-day export repatriation rule. Bangladesh Bank requires exporters to repatriate foreign currency proceeds within 120 days of shipment. Missing this can restrict your ability to open new LCs.

9. Not using BTB LC when it’s available. SME exporters who self-finance raw material imports lock up working capital unnecessarily when the back-to-back LC mechanism can free that capital at no extra cost beyond usual bank charges.

If you need to open a business bank account in Bangladesh to start trade finance operations, do it before your first shipment. AD banks need an operating relationship with you before they’ll sanction trade finance limits. And if you’re thinking beyond Bangladesh, US company formation from Bangladesh is an increasingly popular way for local exporters to reach global buyers and collect payments through US entities. For businesses that need financing outside the traditional bank channel, non-bank financial institutions in Bangladesh also offer leasing and working capital products that can complement trade finance.

Key Insights

- LC governs the majority of Bangladesh’s import payments and all LCs follow UCP 600 (ICC, 2007 revision). Getting documents to strictly comply with LC terms is the single most important skill in trade finance.

- Back-to-back LC powers the RMG sector. About 55% of garment exports use BTB LC to finance raw material imports without tying up working capital. It’s available to any exporter with a valid master export LC.

- EDF has been significantly restructured. EDF was reduced from its earlier peak of around USD 7 billion and has reportedly fallen to around USD 2.2 billion, with possible future expansion under discussion. The per-exporter ceiling dropped from $15 million to $10 million. Verify current availability with your AD bank.

- Packing credit and pre-shipment finance rates depend on current Bangladesh Bank rules, refinance availability, and bank pricing. Eligible exporters may access lower-cost pre-shipment support under specific Bangladesh Bank funds.

- LTR keeps your cash moving post-import. Bangladesh Bank limits LTR tenure to 90 days for consumer goods and up to 180 days for other goods. Drawing is one-time only.

- FDBP gives exporters instant cash after shipment under an LC, without waiting for the foreign bank to settle. Bill discounting works similarly for usance LCs.

- Export proceeds must be repatriated within 120 days of shipment per Bangladesh Bank rules. Missing this deadline restricts your ability to open new LCs and invites Bangladesh Bank scrutiny.

Frequently Asked Questions

What is trade finance in Bangladesh?

Trade finance in Bangladesh is the set of banking and financial instruments that fund import and export transactions. It includes letters of credit (LC), back-to-back LC, Export Development Fund (EDF) loans, packing credit, Loan Against Trust Receipt (LTR), bill purchase, bill discounting, and bank guarantees. All instruments are regulated by Bangladesh Bank and accessed through licensed Authorized Dealer (AD) banks.

What is a back-to-back LC in Bangladesh?

A back-to-back LC is a secondary LC opened by an exporter using their master export LC as collateral, to finance the import of raw materials or inputs. The exporter’s AD bank issues the BTB LC in favor of the foreign supplier. When the exporter ships finished goods and receives export payment, those proceeds settle the BTB LC. It’s used extensively in Bangladesh’s garment sector.

How does EDF work in Bangladesh?

The Export Development Fund (EDF), managed by Bangladesh Bank, provides US dollar refinancing to AD banks, which then lend those funds to eligible manufacturer-exporters for importing raw materials against back-to-back LCs.EDF ceilings and availability are updated periodically by Bangladesh Bank, so exporters should confirm the current per-exporter limit and fund availability with their AD bank before applying. EDF loans have a 180-day tenor, extendable to 270 days, and must be repaid from export proceeds.

What is packing credit in Bangladesh?

Packing credit rates should be verified with the current Bangladesh Bank circular and the exporter’s AD bank, as pricing may depend on refinance availability and bank-level terms.

What is LTR in Bangladesh banking?

LTR (Loan Against Trust Receipt) is a post-import financing facility. After imported goods arrive, instead of paying the full LC amount upfront, the importer takes a loan from their AD bank and holds the goods “in trust.” Repayment comes from goods sales. Bangladesh Bank limits LTR tenure to 90 days maximum for consumer goods and up to 180 days for other goods. Drawing is one-time only under each LTR.

What does UPAS LC mean in Bangladesh?

UPAS (Usance Payable At Sight) is a type of LC where the exporter receives payment at sight upon presenting complying documents, while the importer repays the issuing bank at the end of a usance period. For raw materials, UPAS is typically structured for up to 180 days. For capital machinery, terms can extend to 720 days. It benefits exporters needing immediate cash and importers wanting deferred payment.

Who is eligible for EDF loans in Bangladesh?

EDF loans are available to manufacturer-exporters who import raw materials or inputs for direct export production, and to producers of intermediate goods for local delivery (deemed exports) to export-oriented manufacturers. Trading companies, indentors, and service exporters are generally not eligible. Borrowers must also be within the single borrower exposure limit set by Bangladesh Bank.

What is FDBP in Bangladesh?

FDBP (Foreign Documentary Bill Purchase) is a post-shipment export finance instrument where an AD bank purchases (negotiates) an exporter’s export bills drawn under an LC. The bank pays the exporter immediately, taking on the payment risk from the foreign issuing bank. FDBP converts shipped goods into immediate working capital, provided the submitted documents comply with LC terms.

What are the main bank guarantees used in trade finance in Bangladesh?

The main bank guarantees in Bangladesh trade finance are: Bid Bond (assures a tender authority the bidder will honor their bid), Performance Guarantee (ensures contract completion), Advance Payment Guarantee (protects buyers who pay in advance), and Payment Guarantee (covers payment to foreign suppliers). AD banks issue these locally and can arrange foreign bank guarantees through their correspondent networks.

Final Thoughts

Trade finance in Bangladesh is deeper than most traders realize. LC and EDF are just the headline tools. The real skill is knowing how packing credit, LTR, FDBP, and back-to-back LC all connect into one financing cycle that keeps cash moving from supplier to factory to buyer and back again.

If I were starting fresh, I’d pick one instrument, say the one relevant to my next shipment, and learn exactly how it works with my specific bank before applying. What instrument do you need most right now: pre-shipment, post-shipment, or something in between?