Bangladesh Stock Market Guide: DSE, CSE & How to Invest

Complete Bangladesh stock market guide 2026: how DSE and CSE work, how to open a BO account, what to invest…

Back-to-back LC in Bangladesh explained: step-by-step process, Bangladesh Bank rules, documents, and how RMG factories use it to import raw materials duty-free

Your EU buyer sends you an LC for USD 200,000 worth of shirts. But you can’t make the shirts without fabric. And you can’t pay for the fabric because you haven’t been paid yet. That’s exactly the problem back-to-back LC in Bangladesh was built to address. It’s the financial mechanism that lets garment factories import raw materials without upfront cash, using the buyer’s LC as collateral.

This guide explains how it works, what Bangladesh Bank requires, and what to watch out for.

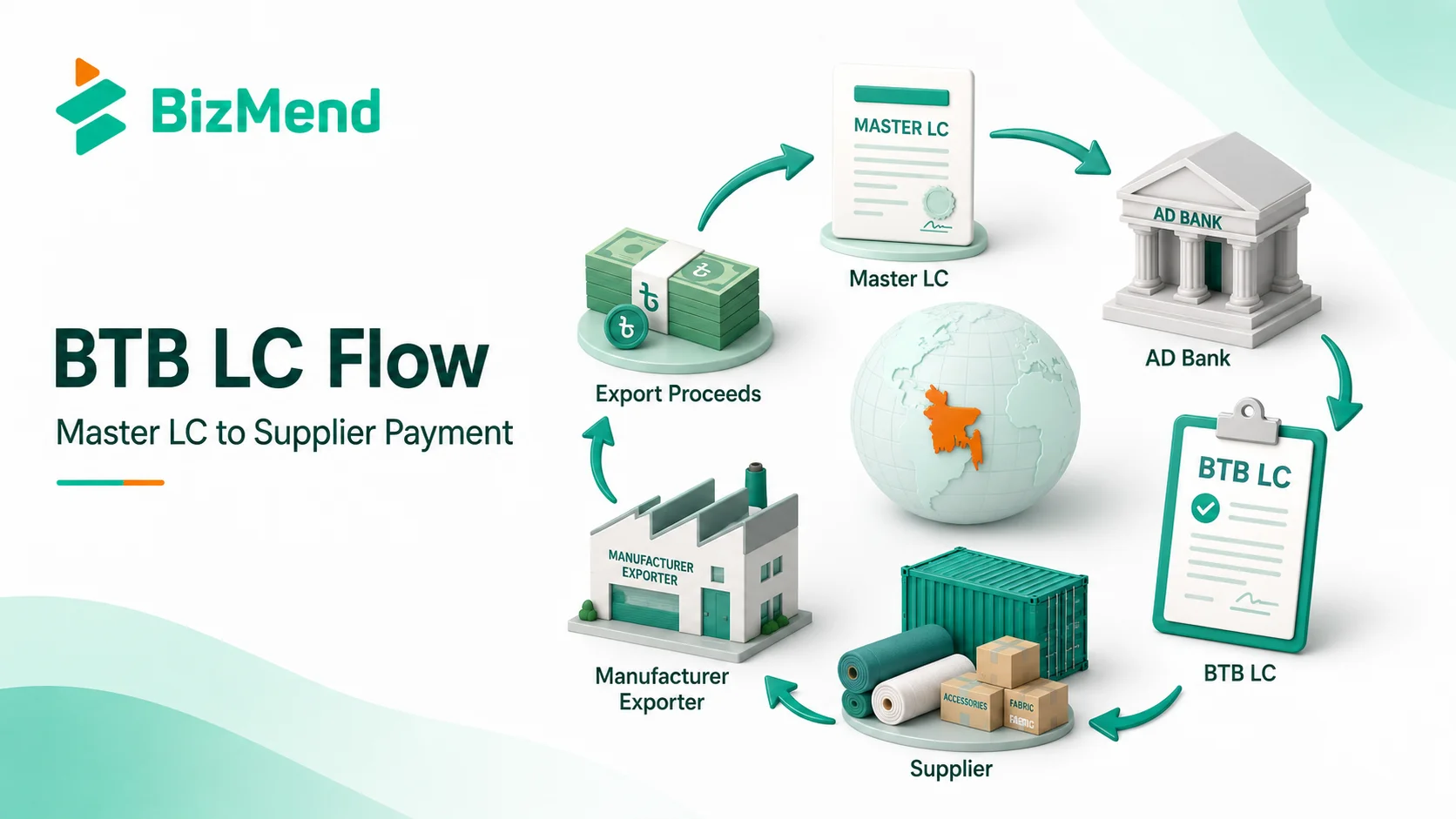

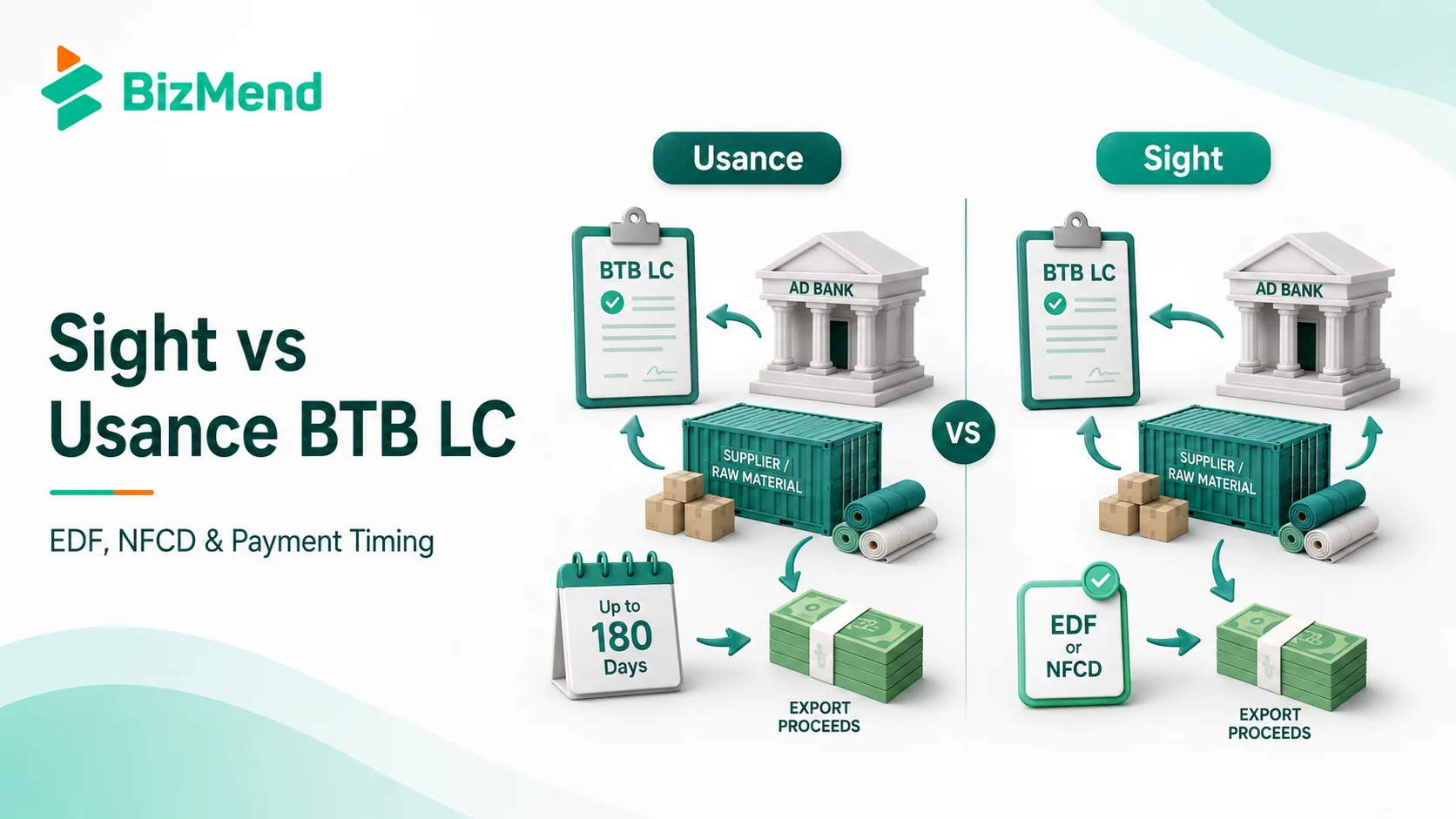

Quick answer: A back-to-back LC in Bangladesh is a secondary import LC opened by an export-oriented manufacturer against a master export LC or export contract. It is mainly used to pay suppliers for raw materials, fabrics, accessories, or packaging needed for export production. Bangladesh Bank allows BTB LC facilities for recognized export-oriented industrial units operating under the bonded warehouse system, subject to valid CCI&E registration, bonded warehouse licence, value-addition limits, and master LC validity. BTB import LCs are generally opened on usance basis for up to 180 days, while EDF/NFCD-backed BTB LCs may be opened on sight basis under relevant Bangladesh Bank instructions.

A back-to-back LC (BTB LC) is a secondary import LC opened by an export-oriented manufacturer against a master export LC or export contract. The manufacturer pledges the master LC as collateral. The bank then opens a new LC in favor of the raw material or accessories supplier.

Bangladesh retained its position as the world’s second-largest apparel exporter after China, with RMG exports reaching USD 38.48 billion in calendar year 2024 (BGMEA and Bangladesh Textile Journal, January 2025). BTB LC is widely used across Bangladesh’s export-oriented RMG sector, supporting procurement of fabric, accessories, and packaging from overseas and local suppliers.

In a regular usance BTB LC, the bank does not usually disburse cash upfront. Instead, it assumes payment liability under the LC when the supplier presents complying documents. BTB LC is usually secured by the master export LC or export contract LC, while margin or collateral requirements depend on Bangladesh Bank instructions, AD bank policy, facility approval, and the client’s risk profile.

If you’re sorting out your banking relationships for trade finance, the guide on top private banks in Bangladesh covers which banks have the strongest export trade finance capabilities.

| Party | Role |

|---|---|

| Foreign Buyer (e.g., EU retailer) | Issues the master export LC through their bank in favor of the garment factory |

| Issuing Bank (buyer’s bank abroad) | Issues the master LC and undertakes to pay the factory on compliant documents |

| Advising Bank (garment factory’s bank in Bangladesh) | Advises the master LC to the factory; opens the BTB LC as the issuing bank |

| Garment Factory (Bangladesh) | Receives master LC or export contract; opens BTB LC against it to pay the raw material supplier |

| Raw Material Supplier (abroad or local) | Beneficiary of the BTB LC; ships fabric, accessories, or packaging to the garment factory |

| Supplier’s Bank | Advises the BTB LC to the supplier; negotiates documents; collects payment |

Bangladesh Bank’s Foreign Exchange Guidelines set out specific rules every AD bank must follow when opening BTB LCs:

If you plan to start a business in Bangladesh in the garment or textile sector, getting your bonded warehouse licence sorted before your first BTB LC application is non-negotiable.

Bangladesh Bank also allows inland back-to-back LCs denominated in foreign exchange in favor of local supplier-manufacturers. Most guides on BTB LC miss this entirely.

This means a garment factory in Dhaka can open a BTB LC in favor of a local yarn mill or accessories maker. The yarn mill ships yarn to the garment factory. The garment factory’s bank pays the yarn mill in foreign exchange at maturity. The yarn mill’s transaction may be treated as a deemed export, and eligible suppliers may access EDF/NFCD-backed facilities subject to Bangladesh Bank rules and AD bank approval.

Reporting note: For inland foreign-currency BTB LCs, EXP/IMP Form is generally not applicable unless EPZ, PEPZ, EZ, or HTP units are involved, as specified in Bangladesh Bank’s current instructions.

Processing speed for BTB LC transactions depends on the AD bank’s trade-finance desk, document quality, compliance review, client limit, and transaction structure. Choosing a bank with a specialized trade-finance team and strong correspondent banking network matters. The guide on commercial banks in Bangladesh gives an overview of banks active in export-oriented trade finance.

Most BTB LCs are usance (deferred payment), with the supplier waiting up to 180 days for payment. But there’s a second type: sight BTB LC backed by EDF or NFCD funds.

| Feature | Usance BTB LC | Sight BTB LC (EDF/NFCD-backed) |

|---|---|---|

| Payment to supplier | At maturity (up to 180 days) | Immediately on document presentation |

| Funded by | Export proceeds (at maturity) | EDF loans or NFCD balances via AD bank |

| Interest (EDF-backed) | Usance interest per BB guidelines | SOFR + 1.50% p.a. (BB FE Circular No. 15, September 1, 2024); effective rate changes as SOFR varies daily |

| Eligibility | All eligible BTB LC factories | Manufacturer-exporters eligible for EDF or NFCD facility |

| Cash flow for supplier | Delayed payment | Immediate payment |

| Cash flow for factory | Deferred liability under LC | EDF/NFCD-backed loan, repaid from export proceeds |

Large AD banks with strong trade-finance desks may offer broader correspondent banking support and faster processing, depending on the client profile. The guide on top foreign banks in Bangladesh gives a starting overview of trade-finance-active banks in Bangladesh.

Required documents usually include valid IRC and ERC issued/renewed through CCI&E, bonded warehouse licence, trade licence, TIN/e-TIN, VAT/BIN where applicable, trade association membership, master export LC or export contract, supplier proforma invoice, BTB LC application, LCAF where required, and bill-of-entry/import reporting documents as applicable.

Having a clean bank account with a solid transaction history matters here. Check the guide on how to open a business bank account in Bangladesh before approaching any bank for trade finance limits.

Normal settlement: On the BTB LC’s maturity date, the AD bank settles payment to the supplier’s bank from the garment factory’s foreign currency export proceeds. The AD bank maintains a foreign currency pool for each bonded warehouse factory, helping match BTB import payments with export receipt timings.

If the export fails and the BTB LC payment falls due:

Export failure creates forced LC liability at the bank, which can block the factory from opening new LCs until the liability is settled. For exporters who also need working capital support outside of BTB LC, non-bank financial institutions in Bangladesh offer leasing and other financing products. And if you’re expanding internationally, US company formation from Bangladesh is an option many export-oriented businesses are now pursuing.

A back-to-back LC (BTB LC) in Bangladesh is a secondary import LC opened by an export-oriented manufacturer against a master export LC or export contract. It is mainly used to pay suppliers for raw materials, fabrics, accessories, or packaging needed for export production. BTB LC is usually secured by the master export LC, with margin requirements depending on bank policy and client profile.

Only recognized export-oriented industrial units operating under the bonded warehouse system can open back-to-back LCs in Bangladesh. The factory must hold valid IRC and ERC issued/renewed through CCI&E, and a valid bonded warehouse licence from the Customs Bond Commissionerate. These requirements come from Bangladesh Bank’s Foreign Exchange Guidelines.

A master LC (or export contract) is received by the Bangladeshi factory from the foreign buyer’s bank. It guarantees payment to the factory when compliant export documents are presented. A back-to-back LC is issued by the factory’s own AD bank against the master LC, in favor of the raw material supplier. The master LC finances the garment factory; the BTB LC finances the supplier.

The BTB LC value cannot exceed the admissible percentage of the net FOB value of the master export LC, as determined by the domestic value addition requirement in the Ministry of Commerce’s current Import Policy Order (IPO). Multiple BTB LCs can be opened against one master LC for different types of inputs, provided the combined value stays within the admissible limit.

BTB import LCs are generally opened on usance basis for up to 180 days, unless a specific or latest Bangladesh Bank instruction allows otherwise. For EDF or NFCD-backed sight BTB LCs, payment is made immediately to the supplier. For EDF-backed sight BTB LCs, the customer-level interest rate is SOFR + 1.50% p.a. under BB FE Circular No. 15 dated September 1, 2024, with the effective rate varying as SOFR changes daily.

An inland BTB LC is a back-to-back LC denominated in foreign exchange opened in favor of a local manufacturer-supplier (such as a yarn mill or accessories maker). Bangladesh Bank allows this to facilitate local input procurement for export-oriented factories. The local supplier’s receipt counts as a deemed export. For inland foreign-currency BTB LCs, EXP/IMP Form is generally not applicable unless EPZ, PEPZ, EZ, or HTP units are involved.

If the factory fails to export and export proceeds don’t arrive, it must purchase foreign exchange from the banking channel using its own taka funds to pay the BTB LC at maturity. The failure must be reported to the Commissioner of Customs and NBR. Bangladesh Bank requires post-facto approval for any remittance in this situation. Forced loan liabilities at the bank typically follow, restricting future trade finance access.

In most cases, BTB LC is secured by the master export LC placed under lien at the bank, without a cash margin requirement. However, margin or risk requirements may depend on the AD bank’s credit policy and the client’s risk profile. Bangladesh Bank’s rules allow BTB LC against the master export LC, but banks may still apply risk-based conditions at their discretion.

Yes. Bangladesh Bank’s guidelines confirm that more than one BTB import LC can be issued against a single master export LC (or against multiple master export LCs). A garment factory might open separate BTB LCs for fabric, accessories, and packing materials, all against the same master LC, provided the combined value stays within the admissible percentage of the master LC’s FOB value.

BTB LC has long been one of the core financing mechanisms behind Bangladesh’s export-oriented garment sector. No factory could afford to pay for fabric, accessories, and packaging upfront and then wait 90 to 120 days for the buyer to pay. The BTB LC structure addresses that gap, and it still does today for millions of export orders every year.

If you’re running a garment operation and aren’t fully comfortable with how your bank handles BTB LC scrutiny, amendments, and payment settlement, that’s the place to start. What’s the one step in your current BTB LC process that causes the most friction?

Complete Bangladesh stock market guide 2026: how DSE and CSE work, how to open a BO account, what to invest…

Export Development Fund (EDF) in Bangladesh explained: current interest rate, eligibility, loan limits, and step-by-step application guide.

Want to close a company in Bangladesh? Learn the legal steps, costs, timelines, and tax clearance requirements for a clean…