If you’re a manufacturer-exporter in Bangladesh and your raw material supplier abroad wants payment now, but your export payment won’t arrive for months, the Export Development Fund (EDF) exists for exactly that gap. It’s Bangladesh Bank’s foreign currency window for the export sector, and most eligible exporters don’t use it correctly.

This guide covers what EDF actually is, who qualifies, what the current interest rate is, and how to apply through your bank.

Quick answer: The Export Development Fund (EDF) in Bangladesh is a foreign currency refinancing facility managed by Bangladesh Bank. It lets eligible manufacturer-exporters borrow US dollars through their Authorized Dealer (AD) bank to pay for raw material imports against back-to-back LCs. As of September 2024, the interest rate is SOFR + 1.5% per annum at the customer level. Loan ceilings vary by exporter category, from as low as USD 2 million for some association categories to up to USD 20 million for eligible BGMEA/BTMA members.

What Is the Export Development Fund (EDF)?

The EDF is a revolving foreign currency fund created in 1989 by Bangladesh Bank, originally set up through an agreement with the International Development Association (IDA). The IDA treaty was signed on April 26, 1989, and the fund started disbursements in October 1989. Its core purpose hasn’t changed since then: give manufacturer-exporters access to foreign currency to pay for the imported raw materials they need to produce export goods.

The fund is managed by Bangladesh Bank’s Forex Reserve and Treasury Management Department (FRTMD) at the central bank’s head office. It’s not a grant or subsidy. It’s a revolving loan pool funded from Bangladesh’s foreign exchange reserves.

The EDF has gone through significant changes in size. During the COVID-19 pandemic, it was expanded to $7 billion. Since 2022, Bangladesh Bank reduced it due to foreign exchange reserve pressures and IMF conditionality. As of April 2026, FBCCI (Federation of Bangladesh Chambers of Commerce and Industry) reported the EDF had fallen to approximately $2.2 billion, prompting business leaders to ask Bangladesh Bank’s governor to gradually expand it back to $5 billion (The Business Standard and The Daily Star, April 2026).

If you plan to start a business in Bangladesh focused on manufacturing for export, the EDF is one of the first financing tools worth understanding.

How the EDF Works in Practice

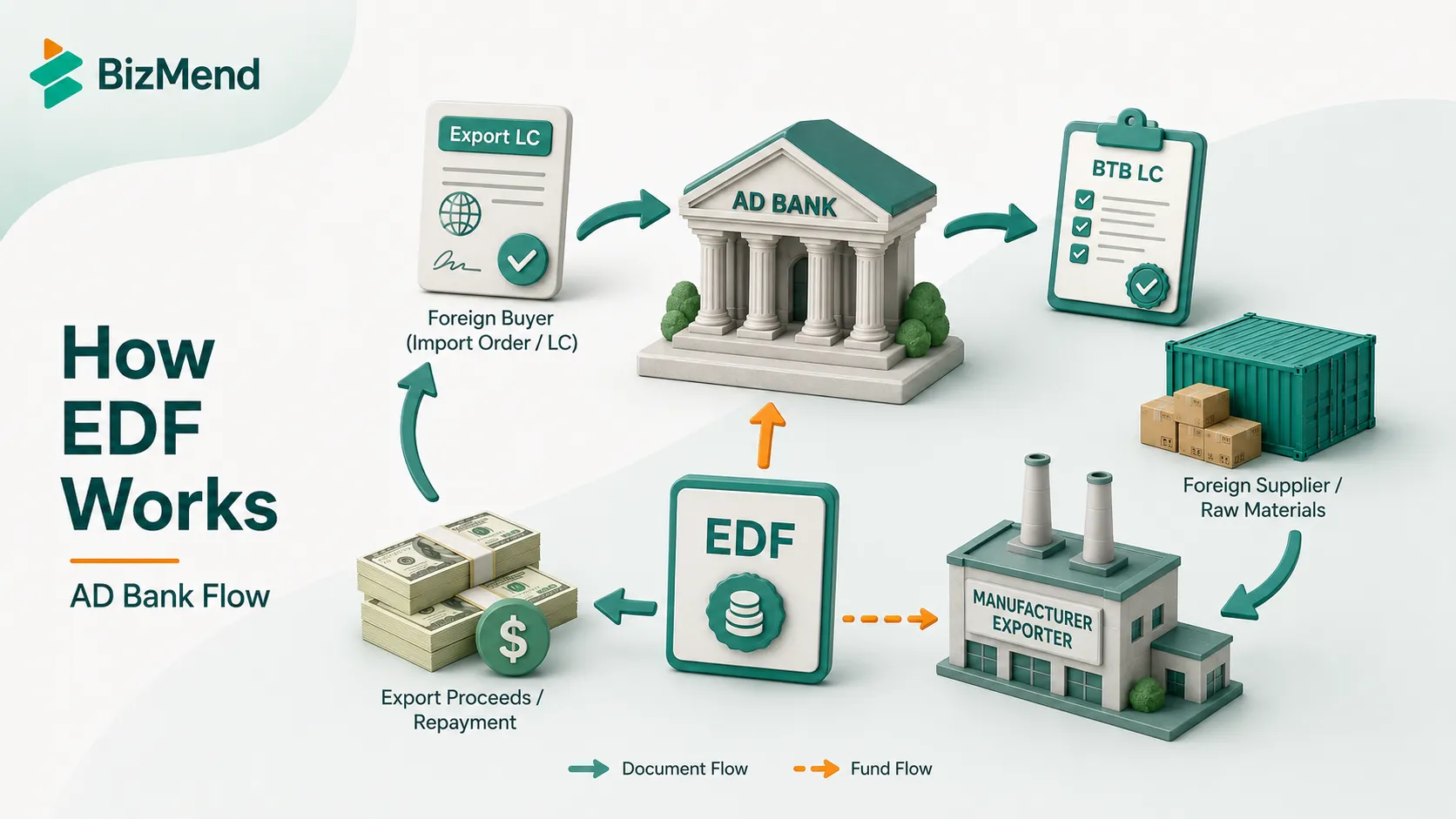

The EDF doesn’t go directly from Bangladesh Bank to your company. It flows through your Authorized Dealer (AD) bank, which is any scheduled commercial bank licensed by Bangladesh Bank to handle foreign exchange transactions.

The basic flow:

- You receive a confirmed export LC (or firm export contract) from your foreign buyer.

- You open a sight back-to-back LC in favor of your raw material supplier abroad.

- Your AD bank pays the foreign supplier when documents arrive.

- Your AD bank then borrows US dollars from Bangladesh Bank’s EDF to cover that payment.

- You owe your AD bank the foreign currency loan, which you repay from your export proceeds when they arrive.

The AD Bank’s Role in EDF Disbursement

Your AD bank does the heavy lifting. It applies to Bangladesh Bank’s FRTMD for EDF funds after paying your back-to-back LC. The branch submits an intimation to Bangladesh Bank at the time of opening the EDF back-to-back LC, and then claims the EDF disbursement immediately after receiving negotiated import bills that comply with LC terms.

The AD bank reports EDF transactions to Bangladesh Bank through a daily LC opening statement and a monthly statement (submitted within 7 days of the following month). EDF operates on a deal-by-deal basis. Shariah-compliant banks participate via a Restricted Mudaraba Agreement with FRTMD.

If you’re looking for which banks have the strongest trade finance capabilities, the guide on top private banks in Bangladesh gives a solid starting comparison.

Who Is Eligible for EDF in Bangladesh?

Who Qualifies

Eligibility is tightly defined by Bangladesh Bank’s FE Circulars. The current framework stems from the Master Circular on EDF (FE Circular No. 45, December 31, 2017) and subsequent circulars. You’re eligible if you are:

- Manufacturer-exporter producing goods for direct export, with a valid export LC or firm export contract from an overseas buyer.

- Producer of intermediate goods (deemed exporter) delivering inputs to manufacturer-exporters against inland back-to-back LCs denominated in foreign exchange. Example: a fabric mill supplying yarn to a garment factory.

- Type B or Type C EPZ company producing readymade garments for export (per FE Circular 90, March 2021).

- BGMEA, BKMEA, BTMA, BDYEA, BGAPMEA, or LFMEAB member firm making bulk raw material imports, subject to association-specific limits.

EDF is also available under Shariah financing modes (Murabaha Foreign Currency Investment) for Islamic banking customers, through MFCI arrangements with FRTMD.

Who Does NOT Qualify

- Trading companies and indentors. EDF is for manufacturers, not resellers.

- Service exporters. Software, freelancing, or consulting firms don’t qualify.

- Exporters with a repatriation default. If you’ve failed to repatriate export proceeds within 120 days of shipment without a permitted extension, you’re disqualified from EDF until the default is cleared.

- Loans exceeding the single borrower exposure limit. Your AD bank cannot extend EDF beyond Bangladesh Bank’s prescribed cap.

- Imports that don’t comply with the value addition criteria of the current Import Policy Order (IPO).

EDF Loan Limits by Exporter Category

Loan ceilings were reduced in April 2023 as Bangladesh Bank tightened EDF access. These are the current applicable limits:

| Exporter Category | Maximum EDF Loan Per Exporter |

|---|---|

| General manufacturer-exporters (BTB LC) | USD 10 million |

| BGMEA member mills | USD 20 million |

| BKMEA member mills | USD 15 million |

| LFMEAB (leather goods and footwear) | USD 15 million |

| BTMA (textile, bulk imports) | USD 20 million |

| BDYEA (dyed yarn, bulk imports) | USD 10 million |

| BGAPMEA (garment accessories, inland BTB LC) | USD 2 million |

For general BTB LC importers, the ceiling is capped at the lower of USD 10 million, or the value of input imports permissible under the export LC per the IPO’s value addition requirements.

EDF Interest Rate: What You’ll Pay Now

This is where most existing guides are wrong. Bangladesh Bank switched to a new interest rate framework effective September 1, 2024, through BB FE Circular No. 15 issued by the Foreign Exchange Policy Department.

The current structure:

- AD banks borrow from Bangladesh Bank’s EDF at SOFR + 0.5% per annum

- Exporters (customers) are charged by their AD bank at SOFR + 1.5% per annum

SOFR stands for Secured Overnight Financing Rate, the benchmark rate published daily by the Federal Reserve Bank of New York at 8am New York time. Bangladesh has been using SOFR since July 2023, replacing LIBOR after its global discontinuation.

The rate is variable and changes daily. When the circular was issued in September 2024, SOFR was approximately 5.33%, making the effective customer rate about 6.83% per annum. As the US Federal Reserve cut rates through late 2024 and into 2025, SOFR has declined. Check newyorkfed.org for the current SOFR before estimating your EDF borrowing cost.

Important: Before September 2024, Bangladesh Bank charged AD banks a fixed 3% and AD banks charged customers a fixed 4.5%. That fixed rate structure no longer applies.

For the best terms on EDF-linked products, the guide on top foreign banks in Bangladesh covers which banks have the strongest international correspondent networks for trade finance.

EDF Loan Tenor and Repayment Terms

EDF loans are short-term by design. Key terms per Bangladesh Bank circulars:

- Standard tenor: 180 days from the date of EDF disbursement by Bangladesh Bank to the AD bank.

- Extension: Up to 270 days maximum, granted by Bangladesh Bank upon written application from the AD bank.

- Repayment source: Must come from the export proceeds of the relative shipment.

- Overdue penalty: AD banks face a 4% per annum penalty on any EDF amount not repaid to Bangladesh Bank on time. Bangladesh Bank can debit this directly from the AD bank’s foreign currency clearing account.

For bulk import association members (BGMEA, BKMEA, BTMA, and BDYEA), EDF loans are also available against past export performance, allowing slightly more flexible drawdown timing.

How to Apply for EDF: Step-by-Step

You don’t apply directly to Bangladesh Bank. The EDF application runs entirely through your AD bank. Here’s how the process works:

- Receive your master export LC or firm export contract from your foreign buyer.

- Open a sight back-to-back LC (EDF BTB LC) through your AD bank’s branch. The branch sends an intimation to Bangladesh Bank’s FRTMD with prescribed details at this stage.

- The foreign supplier ships the goods and presents documents to the negotiating bank abroad.

- Your AD bank receives and pays the negotiated import bills.

- The AD bank branch applies to Bangladesh Bank for EDF disbursement within 3 days of receiving complying import documents.

- Bangladesh Bank’s FRTMD credits US dollars to the AD bank’s foreign currency clearing account.

- The AD bank advises you of the credit and adjusts the EDF loan receivable.

- You ship the export goods and collect export proceeds.

- You repay the EDF loan to your AD bank from export proceeds within 180 days (or up to 270 days if extended).

To manage EDF financing smoothly, you’ll need a current account set up with your AD bank. Read the full guide on how to open a business bank account in Bangladesh if you haven’t already, and make sure your trade finance limits are sanctioned before your first shipment.

How commercial banks in Bangladesh structure their trade finance departments varies. Banks that specialize in export-oriented sectors, particularly garments and textiles, tend to process EDF transactions faster.

Documents Typically Required

The standard set for EDF BTB LC transactions includes:

- Valid export LC or firm export contract (master LC from foreign buyer)

- Membership certificate from the relevant export association (BGMEA, BKMEA, etc.) if applicable

- Export Registration Certificate (ERC)

- Import Registration Certificate (IRC)

- Business/Trade License

- TIN certificate

- BTB LC application and underlying import documents such as proforma invoice, purchase agreement, or sales agreement.

- Commercial invoice from the foreign supplier

- Proforma invoice

- Bank’s credit appraisal and sanction letter for EDF sub-limit

- Insurance cover note or policy

For bulk importers applying based on past export performance, you’ll also need documented evidence of foreign currency realizied from inland back-to-back LCs over the preceding 12 months.

And if you’re expanding beyond Bangladesh and want a US entity to handle global buyers or payment gateways, US company formation from Bangladesh is a practical option many export-oriented businesses are now pursuing.

Common Mistakes to Avoid

- Applying as a trader, not a manufacturer. EDF is strictly for manufacturers who produce the export goods themselves. If you’re buying finished goods and re-exporting, you don’t qualify.

- Having an outstanding repatriation default. If any export bill wasn’t repatriated within 120 days without a BB extension, you’re blocked from EDF until the default is cleared.

- Exceeding the value addition requirement. Your input import value under BTB LC must comply with the IPO’s value addition rules. Over-importing disqualifies the transaction.

- Applying for EDF on deferred or usance BTB LCs. EDF covers sight payment BTB LCs only. Deferred payment structures don’t qualify.

- Delaying the application to Bangladesh Bank. The branch must claim EDF disbursement immediately after receiving complying import documents. Delays cause settlement problems.

- Confusing EDF with packing credit. EDF is foreign currency financing for raw material imports. Packing credit (PC) is taka-denominated pre-shipment working capital for production costs. They’re different instruments serving different needs.

For businesses that also need local currency financing alongside EDF, non-bank financial institutions in Bangladesh offer leasing and working capital products that can complement your trade finance structure.

Key Insights

- EDF is a foreign currency loan, not a grant. It lets manufacturer-exporters borrow US dollars through their AD bank for raw material imports against back-to-back LCs. It must be repaid from export proceeds.

- The interest rate is now SOFR-based and variable. Per BB FE Circular No. 15 (September 1, 2024), AD banks charge exporters at SOFR + 1.5% per annum. The old fixed rate of 4.5% no longer applies. Check current SOFR at newyorkfed.org.

- EDF has shrunk dramatically. The fund stood at $7 billion at its peak but fell to approximately $2.2 billion by April 2026. Bangladesh Bank is in discussion about gradually expanding it back to $5 billion (FBCCI, April 2026).

- Loan ceilings vary by category. General BTB LC importers are capped at USD 10 million. BGMEA members get up to USD 20 million. Association membership matters significantly.

- Trading companies and service exporters do not qualify. EDF is for manufacturer-exporters only. Any repatriation default within the past 120-day window disqualifies you automatically.

- The tenor is 180 days, extendable to 270 days. EDF loans must be repaid from export proceeds within 180 days of disbursement. Extensions require a written application to Bangladesh Bank.

- The application goes through your AD bank, not directly to Bangladesh Bank. FRTMD disburses to the AD bank, which manages the borrower relationship. Your bank relationship quality matters.

Frequently Asked Questions

What is the Export Development Fund (EDF) in Bangladesh?

The Export Development Fund (EDF) in Bangladesh is a foreign currency revolving loan facility managed by Bangladesh Bank’s Forex Reserve and Treasury Management Department (FRTMD). Established in 1989 via an IDA agreement, it provides US dollar financing to eligible manufacturer-exporters through Authorized Dealer (AD) banks against back-to-back LCs for raw material imports.

What is the current EDF interest rate in Bangladesh?

As of September 1, 2024 (per Bangladesh Bank FE Circular No. 15), EDF interest rates are SOFR-based. AD banks borrow from Bangladesh Bank at SOFR + 0.5% per annum. They charge manufacturer-exporters at SOFR + 1.5% per annum. SOFR is a variable rate published daily by the Federal Reserve Bank of New York. The previous fixed rate was 4.5% for customers; that no longer applies.

Who is eligible for EDF in Bangladesh?

EDF is available to manufacturer-exporters producing goods for direct export against valid export LCs or firm export contracts. Producers of intermediate goods (deemed exporters) supplying inputs to manufacturer-exporters under inland BTB LCs in foreign exchange also qualify. EPZ Type B and C companies making garments for export are eligible. Trading companies, indentors, and service exporters are not eligible.

What is the maximum EDF loan per exporter?

Loan ceilings depend on the exporter category. General BTB LC importers: USD 10 million. BGMEA members: USD 20 million. BKMEA members: USD 15 million. LFMEAB (leather and footwear): USD 15 million. BTMA (textile, bulk): USD 20 million. BDYEA (dyeing/yarn, bulk): USD 10 million. These ceilings were reduced in April 2023; exporters should confirm current category-wise limits with their AD bank before applying.

How long is the EDF loan tenor?

EDF loans are repayable within 180 days from the date of disbursement by Bangladesh Bank. This can be extended to a maximum of 270 days upon written application to Bangladesh Bank with explanation of why export proceeds will take longer to arrive. The interest rate during the extension period is the SOFR-based rate prevailing at the time of extension.

Can I apply for EDF directly at Bangladesh Bank?

No. EDF applications are made entirely through your Authorized Dealer (AD) bank. The AD bank opens the EDF BTB LC, pays the foreign supplier, and then applies to Bangladesh Bank’s FRTMD for disbursement. Your AD bank branch must submit an intimation to Bangladesh Bank at LC opening and claim EDF funds within 3 days of receiving complying import documents.

What happens if I don’t repay EDF on time?

If EDF loans are not repaid to Bangladesh Bank on schedule, the AD bank faces a 4% per annum overdue penalty on the outstanding amount, which Bangladesh Bank can debit directly from the AD bank’s foreign currency clearing account. The importer’s creditworthiness is severely affected, and future EDF eligibility will be restricted.

What is a deemed export in the EDF context?

A deemed export under EDF means a local sale of inputs to a final manufacturer-exporter under an inland back-to-back LC denominated in foreign exchange. For example, a textile mill selling yarn to a garment factory against an inland BTB LC in USD counts as a deemed export. The yarn mill can access EDF financing for its own raw material imports on the basis of these inland BTB LC proceeds.

Does EDF cover usance or deferred payment LCs?

No. Under standard EDF rules, the fund covers sight payment back-to-back LCs. EDF is designed for immediate payment to foreign suppliers, not for deferred payment structures. Its purpose is to bridge the timing gap between the sight payment to the foreign supplier and the later arrival of export proceeds from the buyer.

Final Thoughts

Honestly, EDF is one of the most valuable tools available to Bangladeshi exporters, but it’s also one of the most misunderstood. The rate has changed, the fund has shrunk, and eligibility rules have tightened. What worked three years ago doesn’t automatically work today.

If you’re a manufacturer-exporter and you haven’t already set up EDF sub-limits with your AD bank, talk to your trade finance officer this week. The fund is available. It’s just smaller now and the process requires cleaner documentation than it used to. What’s the one thing you’d want to double-check before your next back-to-back LC application?