Most founders assume closing a company is straightforward. File some paperwork, stop trading, done. In Bangladesh, that thinking will leave you with unresolved liabilities, flagged RJSC records, and directors personally on the hook for obligations the company never formally settled.

Closing a company in Bangladesh is a structured legal process called winding up. This guide covers every step, every cost, and every authority you have to deal with, including the parts that catch foreign investors off guard.

Quick Answer: To close a company in Bangladesh, you must follow the voluntary winding-up process under the Companies Act 1994. This involves preparing a Declaration of Solvency, passing a special resolution at an Extraordinary General Meeting, appointing a liquidator, obtaining tax clearance from the National Board of Revenue, and filing a final return with the RJSC. The company’s name is then struck off the register. The full process takes 6 to 11 months.

Is Closing Your Company the Right Move?

Before you start the winding-up process, it’s worth asking whether full dissolution is actually what you need. A few alternatives are worth considering first.

Transfer the shares. If the company has value, selling your shareholding to another party is often faster and cleaner than dissolving. The company continues, you exit.

Make the company dormant. A company with no active business can be kept registered without trading. Annual compliance filings still apply, but there’s no business activity to manage. This works well if you might want to restart later.

Convert the structure. Sometimes founders want to exit Bangladesh operations but keep a presence. Restructuring from a private limited company to a liaison office may be the better call depending on future plans.

If none of those fit, then dissolution is the right path. But it’s worth ruling them out first.

What “Closing a Company” Means Under Bangladesh Law

Under the Companies Act 1994, closing a company formally is called winding up. The process converts the company’s assets to cash, pays off all creditors, settles employee dues, and distributes whatever remains to shareholders. Once done, the RJSC removes the company’s name from its official register. The company ceases to exist as a legal entity.

This process applies only to companies registered under the Companies Act 1994. Closing a sole proprietorship or partnership follows different rules entirely.

The Three Legal Routes

Members’ Voluntary Winding Up: The company is solvent. Directors confirm this in a Declaration of Solvency, and shareholders vote to close. This is the standard route for companies exiting in good financial health.

Creditors’ Voluntary Winding Up: The company is insolvent and can’t pay its debts. Creditors have significant influence over who acts as liquidator and how assets are divided.

Compulsory Winding Up by Court: The High Court Division of the Supreme Court orders the closure. Triggered by creditor petitions, failure to hold statutory meetings, default on statutory filings, or inability to pay debts.

For most founders, members’ voluntary winding up is the route that applies.

Your Pre-Closure Checklist

Before you start any formal filing, get these in order. Skipping any of them causes bottlenecks later.

- Prepare audited financial statements up to the latest practicable date

- Confirm the company has no outstanding bank loans or credit facilities

- Compile a full list of all creditors and outstanding payables

- Calculate all employee settlement obligations: gratuity, provident fund contributions, outstanding salaries, earned leave

- Check for any pending tax assessments or outstanding VAT returns at the National Board of Revenue

- Confirm your annual compliance in Bangladesh filings (annual returns, income tax returns) are up to date with the RJSC and NBR

- Identify all active licenses: trade license, BIN (VAT registration), import/export certificates, any sector-specific permits

- Confirm outstanding contractual obligations with suppliers, landlords, or clients

- For foreign-owned companies: locate all encashment certificates proving original inward investment

Getting these resolved before you start saves weeks. The auditor and the tax office don’t accelerate their timelines for you.

How to Voluntarily Close a Company in Bangladesh: Step by Step

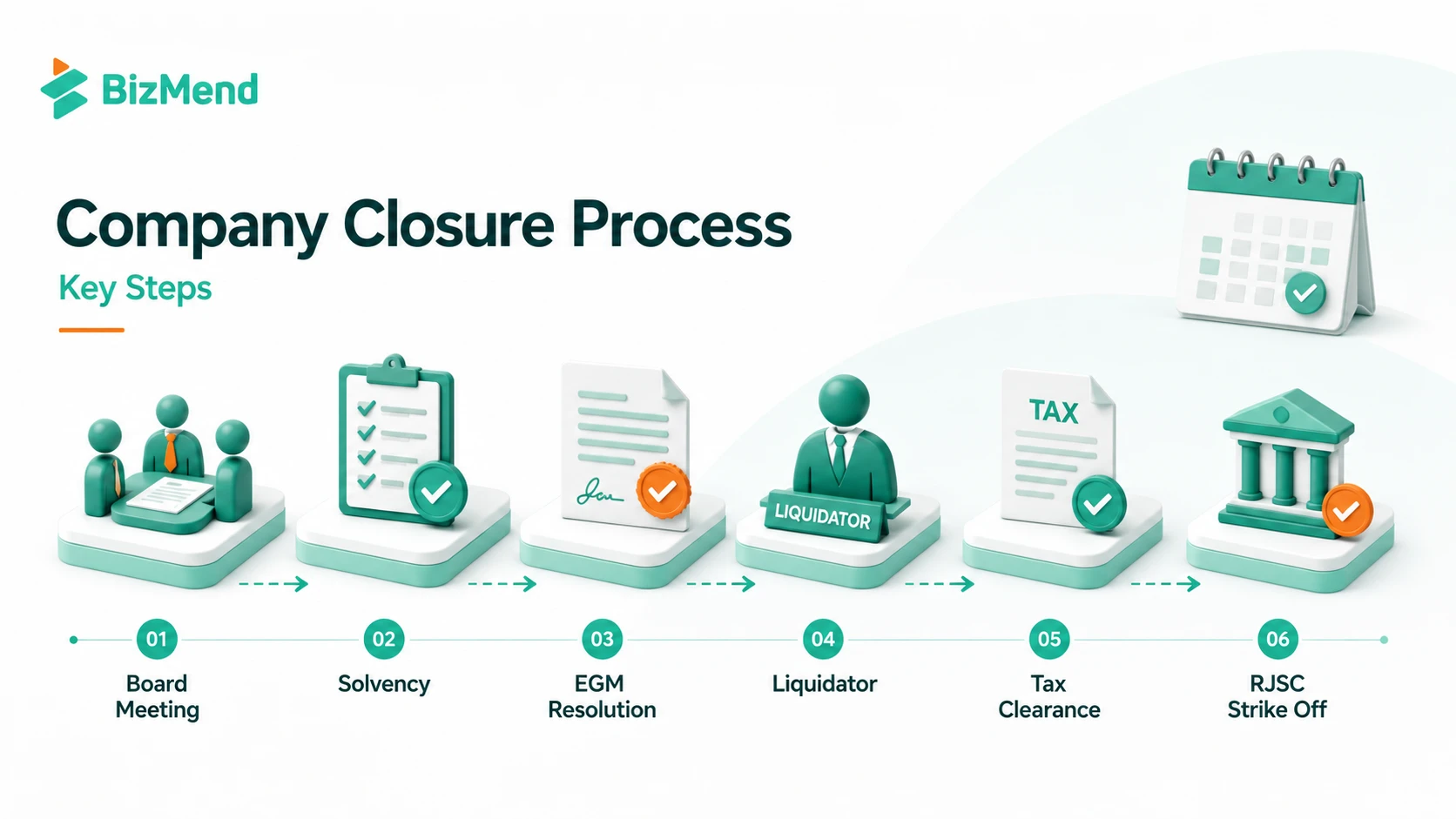

- Board Meeting and Preparation of Documents. The board convenes and approves two documents: the Declaration of Solvency and the audited Profit and Loss Account and Balance Sheet up to the latest practicable date. The Declaration is signed by all directors, or a majority if there are more than two. It confirms directors have made a full inquiry and the company has no debts or can pay all debts within three years. Both documents must be notarised.

- File the Declaration of Solvency with the RJSC. The notarised Declaration must be filed with the RJSC before EGM notices go out. This sequencing is critical and commonly mishandled. RJSC filing first. EGM notice second. Deadline: within 5 weeks of board approval.

- Hold the Extraordinary General Meeting. Shareholders vote to approve the winding up and appoint a liquidator, including their agreed remuneration. The full content of the meeting and the resolution text must also be filed with the RJSC.

- Advertise the Resolution Publicly. Within 10 days of passing the special resolution, publish it in the Official Gazette and in a newspaper circulating in the district where the registered office is located. This is legally required, not optional.

- Notify the RJSC and the Tax Authority. File the liquidator’s appointment with the RJSC using Form VIII. Notify the Deputy Commissioner of Taxes within 15 days. Under Section 199 of the Income Tax Act 2023, business closure is a taxable event. Submit a written application to the DCT within 15 days of cessation and file a final income tax return.

- The Liquidator Runs the Wind-Down. The liquidator realises all assets, pays creditors in the legally required order, fully settles all employee dues (gratuity, provident fund, outstanding salaries), and prepares the Final Account documenting how assets were distributed. If the process runs beyond one year, the liquidator must hold an annual meeting and submit a progress report.

- Final EGM and Submission to RJSC. Once the Final Account is ready, the liquidator calls a final EGM with at least one month’s public notice by advertisement. A special resolution on disposal of company books is passed. The final return and Final Account must reach the RJSC within one week. The RJSC strikes the name from the register. The company is closed.

Handling Tax, VAT, and Licenses Before You’re Done

RJSC filing is only one piece. These regulatory closures must all happen in parallel.

Income Tax (Section 199, Income Tax Act 2023): File a final income tax return covering the period from the start of the last financial year to the closure date. Pay any remaining tax balance. Obtain a tax clearance certificate from the tax office. Without this, the RJSC process cannot conclude cleanly.

VAT Registration (BIN Cancellation): File VAT returns for all outstanding periods up to closure, then formally cancel the BIN with the National Board of Revenue. Leaving a BIN active creates ongoing reporting obligations even after trading stops.

Trade License: Surrender your trade license to the issuing City Corporation or municipality. An uncancelled trade license can complicate future dealings with the same authority.

Sector-Specific Permits: Import/export registration certificates, environmental clearance certificates, or industry-specific permits should be formally closed or surrendered where required.

What Does It Cost to Close a Company in Bangladesh?

Nobody talks about this clearly, so here’s a practical breakdown.

| Cost Item | Estimated Range | Notes |

|---|---|---|

| Liquidator fee | BDT 30,000–150,000+ | Varies by company complexity and assets |

| Legal/corporate lawyer | BDT 50,000–250,000+ | Depends on firm and case complexity |

| CA/audit fees (Final Account) | BDT 20,000–80,000 | Required for audited financial statements |

| Gazette advertisement | BDT 5,000–15,000 | Two required (resolution + final meeting) |

| Newspaper advertisement | BDT 3,000–10,000 | Per advertisement, per newspaper |

| RJSC filing fees | BDT 400–2,000 | Per document filed (approx. BDT 200/document) |

| Notarisation fees | BDT 2,000–5,000 | For Declaration of Solvency |

| Tax clearance processing | Variable | Any outstanding tax must be fully paid |

Total realistic range: BDT 110,000 to BDT 500,000+ for a small to mid-size private limited company, not counting outstanding taxes and employee settlements. Foreign-owned companies should budget additionally for FEID approval costs, AD bank due diligence fees, and Bangladesh Bank compliance documentation.

The Extra Steps for Foreign-Owned Companies

If you started this company as a foreign investor, your entity structure shapes your exit obligations. The company types available to foreign investors in Bangladesh each follow a different path out. A foreign-owned private limited company, a branch office, and a liaison office all have different dissolution paths.

For private limited companies with foreign shareholders: after all debts are settled and the company is wound up, surplus funds belonging to foreign shareholders cannot be sent abroad freely. You need prior approval from Bangladesh Bank.

Post-Liquidation Remittance via FEID

The liquidator, acting through the company’s Authorised Dealer (AD) bank, submits an application to the Foreign Exchange Investment Department (FEID) of Bangladesh Bank. How commercial banks in Bangladesh function as Authorised Dealers matters here: your choice of AD bank affects the timeline of this step.

Documents required for FEID approval:

- Winding-up documents under the Companies Act

- Certificate from liquidator confirming all liabilities are fully paid

- Audited financial statements

- Tax clearance certificates from the NBR

- Encashment certificates proving the original inward investment

This step is mandatory regardless of how much is being remitted. The business bank account in Bangladesh you opened when you incorporated will be the account your AD bank works with through this process.

How Long Does the Process Take?

Local (Bangladeshi-owned) companies: 6 to 9 months under normal conditions.

Foreign-owned companies (with FEID remittance): 9 to 11 months.

What extends the timeline: outstanding tax assessments, employee settlement disputes (gratuity disagreements are common), RJSC processing backlogs, delays in CA completing audited accounts, and FEID approval processing time.

Budget 12 months if this is your first time through the process. Steps that look routine on paper, like booking the auditor or getting tax clearance, usually take longer once you are in the queue.

Key Insights

- Winding up is the only legal way to close a company in Bangladesh registered under the Companies Act 1994. Simply stopping operations doesn’t dissolve the company. The RJSC registration, compliance obligations, and director liability all remain until formal dissolution is complete.

- Consider alternatives before starting. A share transfer, dormant company status, or structural conversion may serve your goals without the time and cost of full dissolution. Worth reviewing before you commit.

- The Declaration of Solvency must be filed with the RJSC before EGM notices go out, and within 5 weeks of board approval. Getting this sequence wrong is one of the most common mistakes that derails the process early.

- Closing a company costs real money. Budget BDT 110,000 to 500,000+ for professional fees, advertisements, filings, and auditing for a standard private limited company, before any outstanding taxes or employee obligations.

- Tax closure is mandatory under Section 199 of the Income Tax Act 2023. Filing a final income tax return and obtaining a clearance certificate from the NBR are non-negotiable steps. Dissolution is treated as a taxable event.

- Foreign investors need Bangladesh Bank’s permission to remit surplus funds after dissolution. The FEID approval process adds 2 to 4 months to the overall timeline and requires specific documentation from the liquidator and AD bank.

- Employee dues, VAT cancellation, and trade license surrender must all be completed before the Final Account is prepared. Outstanding employee settlements can delay the Final EGM significantly.

Frequently Asked Questions

How do you close a private limited company in Bangladesh?

To close a private limited company in Bangladesh, you follow the voluntary winding-up process under the Companies Act 1994. Directors prepare a Declaration of Solvency, which is filed with the RJSC. Shareholders then pass a special resolution at an Extraordinary General Meeting appointing a liquidator. The liquidator settles all liabilities, prepares a Final Account, and after a final EGM, submits the final return to the RJSC. The RJSC strikes the company’s name off its register.

Can I just stop trading and leave the company registered?

You can, but it creates ongoing problems. A registered but inactive company still has annual RJSC return filings and income tax return obligations. Directors remain personally liable for unresolved obligations. If filings lapse long enough, the RJSC may administratively strike off the company, which can affect the directors personally and complicate future company registrations.

What is the Declaration of Solvency and who signs it?

The Declaration of Solvency is a formal statement confirming that directors have made a full inquiry into the company’s affairs and that the company has no debts, or can pay all debts within three years from the commencement of winding up. It must be signed by all directors, or a majority if there are more than two, and then notarised. It must be filed with the RJSC before EGM notices are issued, within 5 weeks of board approval.

How much does it cost to close a company in Bangladesh?

The realistic total for a small to mid-size private limited company ranges from BDT 110,000 to BDT 500,000 or more. This includes liquidator fees (BDT 30,000 to 150,000+), legal fees (BDT 50,000 to 250,000+), CA/audit fees (BDT 20,000 to 80,000), Gazette and newspaper advertisements (BDT 8,000 to 25,000), and RJSC filing fees. Outstanding taxes and employee settlements are additional costs.

Do employees have any rights during company dissolution?

Yes. Employee dues must be fully settled before the liquidator can prepare the Final Account. This includes all outstanding salaries, gratuity, provident fund contributions, and earned leave payments. Employee dues take priority in the creditor payment order. Disputes over employee settlements can significantly delay the Final EGM and the entire closure process.

What is the role of the Special Resolution in closing a company?

The special resolution, passed at the Extraordinary General Meeting, formally approves the winding up and appoints the liquidator. It must be filed with the RJSC and advertised in the Official Gazette and a local newspaper within 10 days of being passed. A second special resolution is passed at the Final EGM regarding the disposal of the company’s books and papers.

What happens to company assets during dissolution?

The liquidator takes control of all assets and converts them to cash. Proceeds pay off creditors in a legally defined order: secured creditors first, then preferential creditors (including employee dues), then unsecured creditors. Whatever remains after all obligations are settled is distributed to shareholders in proportion to their shareholding.

Is closing a company different for a branch office or liaison office?

Yes. Branch offices and liaison offices of foreign companies were set up with BIDA approval, and their closure requires notifying BIDA as well as the RJSC. Liaison offices cannot earn revenue, so their closures are simpler on the financial side, but regulatory notifications are still required from multiple authorities including BIDA and Bangladesh Bank.

What tax return must be filed when closing a company?

Under Section 199 of the Income Tax Act 2023, a company’s cessation of business is a taxable event. The company must file a written application to the Deputy Commissioner of Taxes within 15 days of ceasing operations and file a final income tax return covering the period from the start of the last income year up to the closure date. Any outstanding tax must be paid and a tax clearance certificate obtained.

Can a foreign investor get surplus funds out of Bangladesh after closing a company?

Yes, but prior approval from Bangladesh Bank’s Foreign Exchange Investment Department (FEID) is required before any surplus funds can be remitted abroad. The application goes through the company’s Authorised Dealer bank and must include winding-up documents, a liquidator’s certificate confirming all liabilities are paid, audited financial statements, and tax clearance certificates. No amount threshold exempts you from this approval.

Final Thoughts

Company closure in Bangladesh rewards those who plan ahead and punishes those who don’t. The common pattern: a founder decides to close in month one, does nothing concrete until month three, then discovers outstanding tax filings, an employee dispute, and a liquidator who’s fully booked for six weeks. Suddenly it’s month ten and they’re still not done.

If you’re reading this now, that’s already an advantage. The founders who close cleanly are the ones who treated the checklist seriously from day one.

And here’s a question worth sitting with: do you have other entities open elsewhere while you’re closing this one? If you’re managing a US company alongside your Bangladesh operations, understanding the annual compliance requirements for US-based LLCs keeps that side from becoming a problem while you’re focused on the exit here.

Plan the timeline. Get the auditor booked. Start earlier than feels necessary.