Best Savings Accounts in Bangladesh 2026: Highest Interest Rates

Compare the best savings accounts in Bangladesh for 2026 by interest rate, safety, access, fees, and fit for everyday savers.

Wise to Bangladesh sounds simple until the account rules show up. A Wise money transfer can pay BDT into Bangladesh. The confusion starts when you try to receive, hold, or...

Wise to Bangladesh sounds simple until the account rules show up. A Wise money transfer can pay BDT into Bangladesh. The confusion starts when you try to receive, hold, or route money through a Bangladesh-based Wise account.

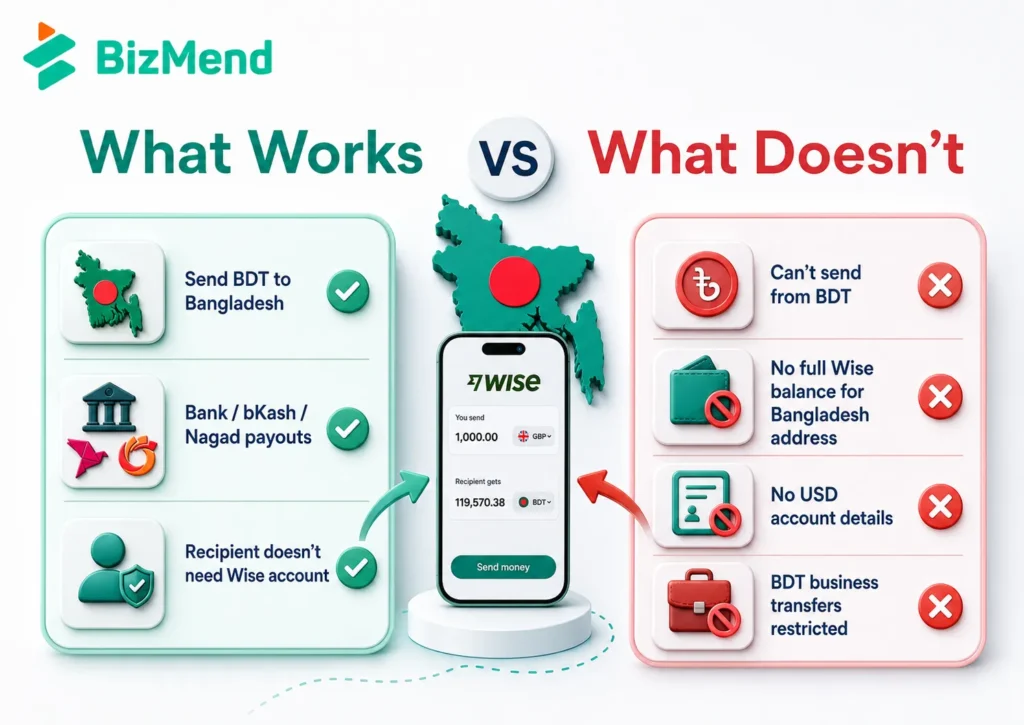

If you’re a freelancer, NRB, or remote worker, the difference matters. Wise can send money into Bangladesh for personal recipients, including bank, bKash, and Nagad payouts. It doesn’t currently give a Bangladeshi address the full balance and account details setup many people expect. This guide gives the clean version: what works, what doesn’t, and where to check before you depend on it without mixing payout access with full account access.

Yes, if the job is sending money into Bangladesh. No, if the job is using Bangladesh as a full Wise account country. That split is the reason so many Wise Bangladesh searches lead to different answers.

Wise is useful for Bangladesh payouts. It isn’t a full banking substitute for a Bangladesh address.

So a person in the US, UK, Canada, Europe, or another supported sending market may be able to send BDT to a relative in Dhaka. A Bangladesh-based freelancer, though, should not treat Wise like a guaranteed way to get US bank details or hold client funds.

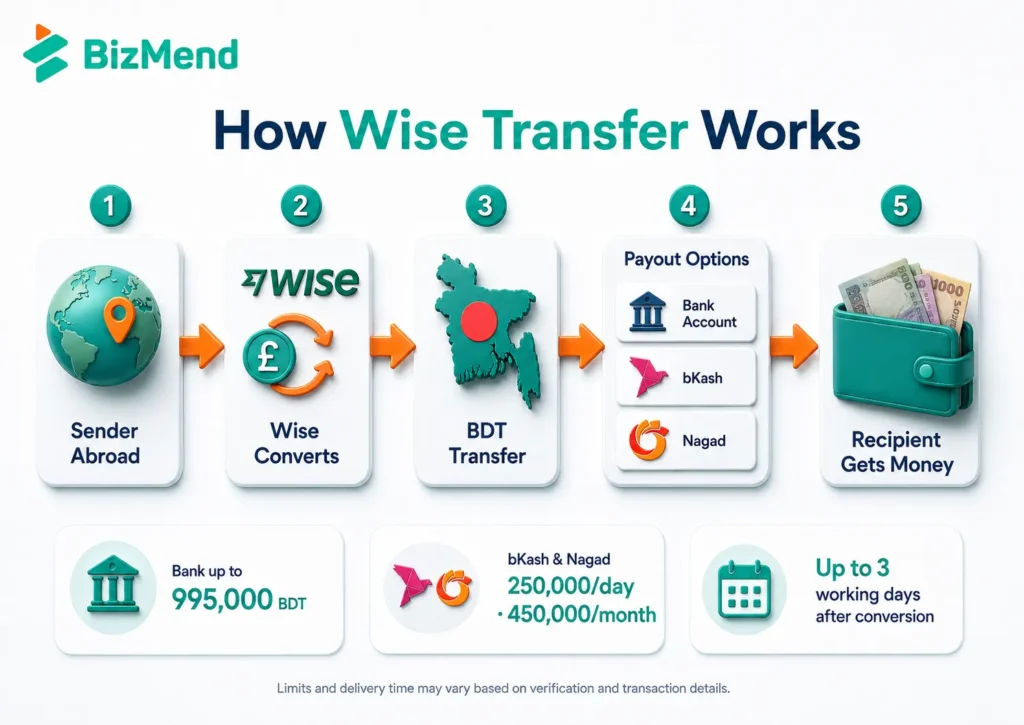

For a normal personal remittance, Wise works as a sender-side transfer tool. The sender funds Wise in an available currency. Wise converts the money, then pays the recipient in Bangladeshi taka.

The recipient usually doesn’t need to open Wise. For a bank payout, the recipient needs a Bangladesh bank account that can receive the local transfer. For mobile wallet payouts, the mobile number has to match the wallet account.

Small detail errors cause real delays. Wise’s BDT guide asks for different information depending on the payout method, so confirm the recipient record before the sender pays.

| Payout method | Details to collect | Watchpoint |

|---|---|---|

| Bangladesh bank account | Full recipient name, bank and branch details, and bank account number. | The account number should be a maximum of 17 digits and should match bank records. |

| bKash or Nagad | Recipient mobile number connected to the wallet account. | Wise says the number should start with 880, so remove the local leading zero. |

If you’re receiving money from abroad, don’t guess branch names or account formats. Ask your bank or wallet provider for the exact details, then pass those details to the sender.

Treat Wise’s calculator as the live source for price and timing. Fees, exchange rates, funding methods, and delivery estimates can change by country, amount, payment method, and verification status.

| Item | Wise guidance | What it means |

|---|---|---|

| Bank account limit | Up to 995,000 BDT per transfer to bank accounts. | Larger personal transfers may need more than one transfer or another bank route. |

| bKash and Nagad limit | 250,000 BDT per day and 450,000 BDT per month. | Mobile wallet payouts are useful, but they aren’t built for every large transfer. |

| Arrival time | Up to 3 working days after Wise receives and converts the money. | Do not promise same-day delivery until Wise shows the final estimate. |

| Conversion time | Conversion can take up to 2 working days. | Funding delays or extra checks can add time before payout. |

| Fee and rate | Shown before the sender pays. | Check the exact route instead of relying on an old screenshot. |

This matters most around rent, tuition, family medical bills, and payroll-like payments. If a deadline is tight, give the transfer more room than the fastest estimate suggests.

Freelancers usually want one of three things: invoice payment, foreign currency holding, or a route from client money to a Bangladesh bank account. Wise doesn’t treat all three as the same product.

The wrong question is whether Wise exists in Bangladesh. The right question is which Wise feature you mean.

A personal gift from an NRB family member is not the same as a client paying a software invoice. Keep personal remittance, salary, freelance income, and business income separate in your records. Yeah, it’s less tidy than people want, but it prevents expensive confusion.

Wise’s help page describes Bangladesh’s Cash Incentive for Inward Wage Remittances. It says a Bangladesh national working abroad can receive a 2.5% incentive on money sent back to Bangladesh, and the incentive goes to the recipient.

Do not assume every foreign payment gets that treatment. Mutual Trust Bank’s terms for the wage earner incentive list freelancing, IT services, remote jobs, trade payments, exports, gifts, and goods or services transactions as ineligible for that 2.5% wage earner incentive. Salary repatriated from abroad may qualify after verification.

That’s compliance-aware, not alarmist. Clean money can still be delayed when the purpose code, sender type, or recipient documentation doesn’t match the bank’s review process.

Most Wise confusion comes from using one label for different money flows. A family remittance, a salary payment, a client invoice, and a business settlement can all look like foreign money coming into Bangladesh. Banks may treat them very differently.

| Scenario | Wise fit | Practical move |

|---|---|---|

| NRB sends monthly support to family. | Often a good fit if Wise shows Bangladesh as available from the sender country. | Save the recipient profile, then check the live rate and fee each month. |

| Overseas friend sends a personal gift. | Can fit if both sides are individuals and the payout is BDT. | Keep the purpose personal and avoid invoice or supplier language. |

| Remote employer pays salary. | Not always a normal Wise remittance. | Ask payroll and the recipient bank what documents and purpose wording they need. |

| Freelance client pays an invoice. | BDT business restrictions may block or complicate the Wise route. | Use a bank or approved payment route that matches service income records. |

| Bangladesh resident wants USD details. | Wise is not a reliable answer for a Bangladesh address. | Check regulated bank or payment options that actually support your residence. |

That sounds picky, but it is the practical difference between a transfer and a record you can defend later. If the payment is income, treat the bank trail as part of the job.

Before using Wise for a bank account in BD, run a quick check. It takes five minutes and can save a full week of follow-up.

For recurring family support, this checklist may feel repetitive. For freelancer income, it is essential. A payment route that works once can still fail later if the sender, amount, purpose, or bank review changes.

Wise fits best when the sender is outside Bangladesh, the recipient is an individual, and the payout is meant to arrive in BDT. It is less suitable when you’re trying to create a foreign account layer for Bangladesh-based earnings.

| Wise may fit | Use another route |

|---|---|

| NRB family remittance to a personal recipient. | Client payment to a Bangladesh business or supplier. |

| BDT payout to a bank account, bKash, or Nagad. | Need for USD account details with a Bangladesh address. |

| Sender wants an upfront fee and rate before payment. | Need to hold foreign currency in a Bangladesh-based Wise balance. |

| Personal transfer within Wise’s BDT rules. | Outbound payment from BDT or a corporate BDT transfer. |

The best route is the one that matches the real payment purpose. If the money is salary, invoice income, or business proceeds, start with that truth before choosing the transfer tool.

Wise can be a strong Bangladesh payment tool, especially for personal remittances into BDT. The mistake is treating it as a full banking answer for every Bangladesh-linked earner. Check the exact feature, sender type, recipient type, limit, and bank documentation before you rely on it. That one check keeps the transfer practical.

Yes, you can receive money sent through Wise in Bangladesh when the payout route is supported. Wise’s Bangladesh guidance lists bank accounts, bKash, and Nagad as BDT payout options. For a local bank payout, the recipient usually doesn’t need a Wise account.

Wise may let people register from many countries, but a Bangladesh address should not expect the full Wise Account feature set. Bangladesh is not on Wise’s current list for holding money, and Wise lists Bangladesh as unavailable for USD account details.

Wise’s BDT guide says BDT can be sent to bKash and Nagad accounts in Bangladesh. The recipient mobile number should start with 880. Wise also lists caps of 250,000 BDT per day and 450,000 BDT per month for bKash and Nagad.

Sometimes the word Wise is used too broadly here. A client may not be able to send a business transfer to BDT through Wise, and a Bangladesh-based freelancer should not assume access to USD account details. Use a route that fits the invoice, tax, and bank purpose.

Wise says that after it receives and converts the money, a BDT transfer can take up to 3 working days to arrive in the recipient’s bank account. Conversion can take up to 2 working days, and Wise shows the estimated timing when the transfer is created.

Compare the best savings accounts in Bangladesh for 2026 by interest rate, safety, access, fees, and fit for everyday savers.

A Nagad merchant account turns a phone number into a payment counter. For small shops, that can mean faster checkout…

How to register a partnership firm in Bangladesh under the 1932 Act. RJSC steps, deed clauses, fees, taxes, and the…