Corporate tax in Bangladesh gets confusing fast. One source says 27.5%. Another mentions 20%, 22.5%, tax holidays, minimum tax, and filing dates that seem to move. If you run a company, that confusion can wreck pricing, cash planning, and board-level forecasts.

The practical version is simpler. Most local companies should begin with the standard rate that applies to their entity type, then test whether a listed-company break, an approved exemption, or minimum tax rules change the final bill. This guide walks you through the 2026 rates, the reliefs worth checking, and what filing a company return in Bangladesh actually involves.

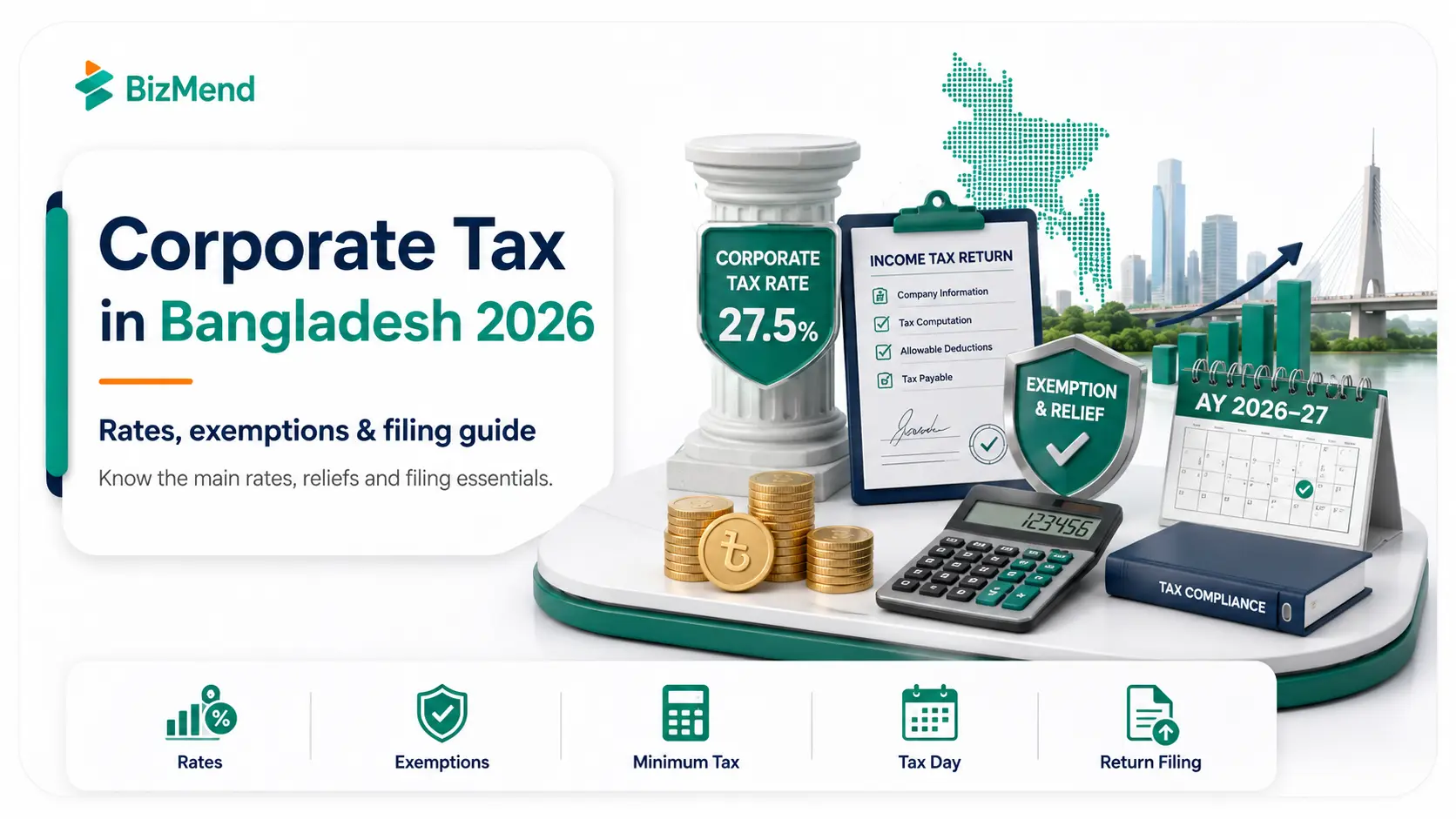

Quick answer: For most local private companies in Bangladesh, the working corporate tax rate for Assessment Year 2026-27 is 27.5%. Listed companies, banks, mobile operators, tobacco manufacturers, and approved exempt projects can fall under different rules. Company returns follow the tax day set by the Income Tax Act, 2023, unless NBR later issues a specific extension.

Key Takeaways

- For many local private limited companies, 27.5% is the right starting assumption for Assessment Year 2026-27.

- A locally incorporated company with foreign shareholders usually follows the same company rate table as a locally owned company. The extra foreign-owner issues sit in remittance, treaty, and withholding rules.

- Listed companies may still get lower rates, but the details depend on how much paid-up capital moved through the IPO and whether income moved through banking channels.

- Minimum tax can apply even when your company reports little profit or a loss, so a weak P&L does not always mean a low final tax bill.

- Tax holidays and reduced-rate incentives are approval-based. You do not get them just because your sector sounds similar to an eligible one.

- The legal filing date comes from the company’s tax day under the Income Tax Act, 2023, but NBR has recently granted deadline extensions in practice.

- Late filing can trigger both cash penalties and extra scrutiny, especially if your return position depends on reduced rates or exemptions.

- If your project sits in an EPZ, economic zone, or hi-tech park, check the live SRO and the zone authority before you lock in any forecasted tax savings.

What Corporate Tax in Bangladesh Actually Means

Corporate tax is the income tax a company pays on taxable profit. In Bangladesh, a resident company is taxed on worldwide income, while a non-resident company is taxed on Bangladesh-source income. That distinction matters, but for a locally incorporated company, the first practical question is still simple: what company rate category do you fall into?

This article is the local-company version of the topic. A local company owned by Bangladeshi founders and a local company owned by foreign shareholders usually start from the same company rate table. The foreign-owner complications come later through profit remittance, treaty relief, branch taxation, and withholding. If you are still at the company-setup stage, your tax position can also be shaped by where and how the project is registered.

Corporate Tax Rates in Bangladesh for 2026

Here is the part most readers actually came for. In Assessment Year 2026-27, the default answer for many local companies is 27.5%. For official reference, check NBR’s latest Income Tax Paripatra 2025–2026 before finalizing any tax position.

| Company category | Indicative 2026 rate | What to know |

|---|---|---|

| Other local companies, including most private limited companies | 27.5% | This is the main working rate for ordinary local companies in the 2026-27 summary. |

| Publicly traded company with more than 10% of paid-up capital through IPO | 22.5% | The budget summary keeps a lower listed-company rate here, with a 20% outcome where the banking condition is met. |

| One-Person Company | 27.5% | Older writeups often mention a lower rate. Recheck your assumption against the current year summary before budgeting. |

| Publicly traded bank, insurance, or finance company | 37.5% | No general rebate applies in the current summary. |

| Non-publicly traded bank, insurance, or finance company | 40% | This remains one of the higher corporate rate bands. |

| Mobile phone operator company | 45% | Special IPO-linked relief can matter, but the base rate is still high. |

| Tobacco manufacturer | 45% plus 2.5% surcharge | This is the highest routine headline rate in the current table. |

| Private university, private medical college, private dental college, private engineering college, or private ICT college | 10% | Sector-specific rate. Check the exact institutional category before using it. |

Two details trip people up here. First, old blog posts and old budget notes still float around with 25% or 22.5% numbers for non-listed companies and OPCs. Those older rates are not a safe 2026 planning shortcut. Second, listed-company relief is not just about being listed. The amount raised through IPO and the way income moves through banking channels can still change the result.

When a Company May Pay Less Than the Standard Rate

Lower taxes are possible in Bangladesh, but they are rarely automatic. In most cases, a company needs to qualify through its category, approval status, location, or a specific incentive rule.

Here are the main situations to check:

Listed-company benefit

A publicly traded company may qualify for a lower rate if it moves more than 10% of its paid-up capital through an IPO. The current budget summary also allows a 20% outcome where the banking condition is met.

Approved tax-exempt manufacturing activities

The Sixth Schedule to the Income Tax Act allows phased exemptions for certain approved manufacturing businesses. The list includes sectors such as API, agricultural machinery, automobile parts, electronic components, leather goods, mobile phone manufacturing, plastic recycling, toy manufacturing, and some AI or automation-related manufacturing.

Timing rules

This is where many forecasts go wrong. The current published schedule ties eligibility to approved entities that started commercial production between July 2020 and June 2025. So, if a project starts in mid-2026, do not assume a tax holiday unless a newer extension or sector-specific notice confirms it.

Zone-based incentives

Companies in economic zones, EPZs, and hi-tech parks may get separate incentive packages. Some can be strong, especially for hi-tech and export-oriented businesses. But the company, project location, approval file, and active SRO all need to match.

The safe approach is to separate three things: a lower rate based on company category, an exemption based on formal approval, and marketing claims about incentives that still need legal confirmation.

Do Not Ignore Minimum Tax

A company can have weak profit and still owe tax. Bangladesh uses a minimum-tax framework that compares regular tax on profit with tax on gross receipts and, in some cases, withholding outcomes. For many ordinary company cases, the gross-receipts minimum is 1%. For mobile operators it is 1.5%. For tobacco and sweetened beverages, it is 3%.

There is also a narrow point of relief worth knowing. A manufacturing industrial undertaking can fall to 0.1% of gross receipts for its first three income years from commercial production, subject to the conditions behind that treatment. So yes, the minimum-tax regime can cut both ways. It can create a bill when you expected none, and in a few approved cases it can soften the landing for a new factory.

In practice, this means a company tax computation should not stop at taxable profit. You need to test the minimum-tax floor before you sign off the return or quote the year-end liability to management.

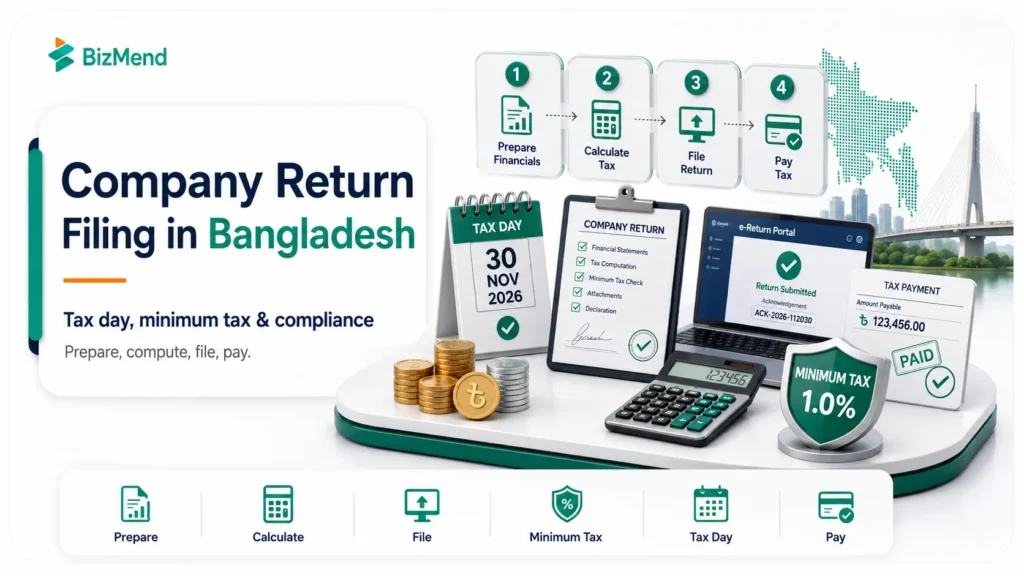

The Filing Timeline and What the Return Usually Includes

Under the Income Tax Act, 2023, a company’s tax day is the 15th day of the seventh month after the end of the income year, or 15 September if that earlier date would land on or before 15 September. That is the statutory rule. In real life, NBR may still extend a filing cycle. For example, for the 2025-26 return season, the deadline for non-individual taxpayers was extended through 17 May 2026 after 15 May fell on a weekend holiday.

A company return usually pulls together the audited accounts, a tax computation, schedules for advance tax and tax deducted at source, support for any exemption or reduced-rate claim, and the payment trail for any balance due. The return must be signed and verified by the company’s principal officer under the Act.

NBR’s e-services pages show that e-Return remains part of the live filing setup. Even so, the safest approach is not to reduce filing to portal data entry. Close the books first. Reconcile tax positions second. Submit only after the rate category, minimum tax, withholding credits, and exemption papers all line up.

- Confirm the correct company category for the year. Most errors start here.

- Close the financial statements and get the audit file ready before the tax computation is finalized.

- Compute both regular tax and minimum tax. Use the higher result where the rules require it.

- Match withholding tax, advance tax, and any tax paid with the return to your ledger and bank evidence.

- File by the statutory date unless NBR issues a written extension for that filing cycle.

- Archive the acknowledgment, payment proof, and supporting schedules in one place for assessment or bank queries later.

If your company relies heavily on trade flows, foreign currency, or profit transfers, the banking side also matters. Foreign Banks in Bangladesh for Export Import Business is a useful next read for that operational angle.

Mistakes That Create Trouble Fast

- Budgeting from an outdated tax rate

Teams often see an old 25% rate in an article, copy it into a forecast sheet, and forget to update it. By the time the return is due, the pricing, dividend plan, and cash forecast may already be wrong. - Treating incentives as guaranteed savings

A tax holiday is not automatic. A reduced rate is not given just because a company works in a promising sector. If the approval, start date, location condition, or banking requirement is missing, the lower rate may not hold. - Filing late and underestimating the damage

Late filing creates penalties and extra attention. NBR’s FAQ pages cite a penalty of 10% of the tax on the last assessed income, with a Tk 1,000 minimum, plus Tk 50 for each day the delay continues. Even when the amount is manageable, the follow-up work can waste serious time. - Ignoring proper documentation

Current rate relief and exemption conditions often depend on bank-routed receipts, bank-routed payments, and traceable transactions. If the paper trail is weak, the lower-rate claim becomes weak too.

Late filing hurts twice: first in penalties, then in the questions it invites.

Final Thoughts

Corporate tax in Bangladesh is not impossible to handle. It just punishes lazy assumptions. Start with the right rate, test every claimed exemption before you promise a saving, and treat the filing calendar like part of operations. That is how a tax issue stays admin work instead of turning into a cash problem.

Frequently Asked Questions

What is the standard corporate tax rate for a private limited company in Bangladesh in 2026?

For many ordinary local private limited companies, the working rate for assessment year 2026-27 is 27.5%. You should still confirm whether the entity sits in a special category, because listed companies, banks, telecom operators, tobacco manufacturers, and some education entities follow different rates.

Does a company still pay tax in Bangladesh if it made little profit or a loss?

Possibly, yes. Bangladesh uses minimum-tax rules based on gross receipts, so a low-profit year does not always mean a zero tax bill. That is why companies should test regular tax and minimum tax side by side before filing.

When is a company income tax return due in Bangladesh?

The legal due date comes from the company’s tax day under the Income Tax Act, 2023. That is generally the 15th day of the seventh month after the income year ends, or 15 September if that earlier date would fall before 15 September. NBR can still issue cycle-specific extensions, so always check live notices before filing.

Are tax holidays or corporate tax exemptions automatic for eligible sectors?

No. They depend on approval, sector fit, location, commencement timing, and the live SRO or schedule behind the benefit. If your file cannot prove those conditions, you should not budget as if the exemption is guaranteed.

Does foreign ownership change the corporate tax rate of a Bangladesh-incorporated company?

Not by itself. A locally incorporated company with foreign shareholders usually follows the same company-rate table as any other local company in that category. The extra foreign-owner issues usually show up in remittance, withholding, treaty, and branch-office rules, not in a separate local company rate table.