How to Close a Company in Bangladesh: Dissolution & Winding Up

Want to close a company in Bangladesh? Learn the legal steps, costs, timelines, and tax clearance requirements for a clean…

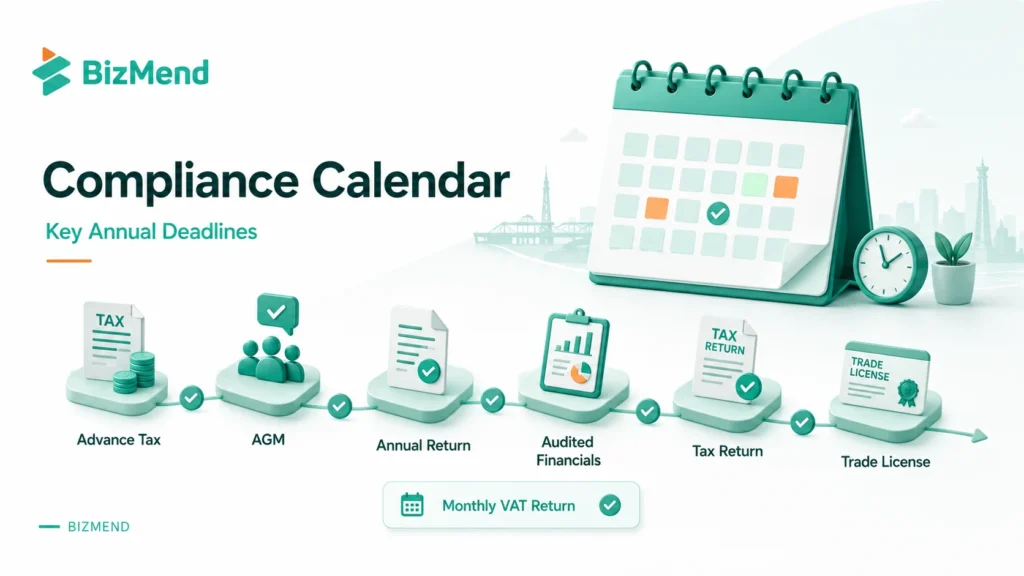

A complete guide to annual compliance in Bangladesh: RJSC filings, income tax deadlines, VAT returns, and penalties explained clearly.

Quick Answer: Annual compliance in Bangladesh requires companies to file an annual return with the RJSC within 21 days of the AGM, submit audited financial statements within 30 days of the AGM, file a corporate income tax return with the NBR (standard deadline: January 15 for July-June fiscal year), pay advance taxes quarterly, file monthly VAT returns, and renew the trade license annually. Non-compliance can result in fines up to BDT 10,000 for RJSC violations and 2% monthly penalties on unpaid tax.

Running a company in Bangladesh without tracking compliance deadlines is one of the fastest ways to get fined, flagged, or frozen. And it happens more than you’d think.

Annual compliance in Bangladesh covers everything your business must file, submit, and renew each year to stay legally active. That means RJSC filings, income tax returns, VAT returns, advance tax payments, and trade license renewals. Each one has its own deadline and its own authority.

This guide breaks down every requirement clearly, so whether you’re a first-time founder or a seasoned finance professional, you know exactly what’s due and when.

Annual compliance in Bangladesh refers to the mandatory filings, payments, and renewals that every registered company must complete each year to remain in good legal standing.

The framework comes from two main sources. On the corporate side, the Companies Act 1994 governs everything administered by the Registrar of Joint Stock Companies and Firms (RJSC). On the tax side, the Income Tax Act 2023 and the VAT and Supplementary Duty Act 2012 set the rules, both enforced by the National Board of Revenue (NBR).

Corporate compliance covers AGMs, annual returns, and audited financial statements filed with the RJSC. This track is about maintaining your company’s formal legal status.

Regulatory and tax compliance covers income tax returns, quarterly advance tax payments, monthly VAT returns, and annual trade license renewal with your local City Corporation.

Both tracks are non-negotiable. Miss one, and you risk fines. Ignore both long enough, and the RJSC can flag your company as non-compliant, which restricts future filings and strains banking relationships.

Every company registered under the Companies Act 1994 is required to complete annual compliance. That includes:

So if you’re thinking about starting a business in Bangladesh as a foreigner, know that annual compliance obligations begin in your very first year of operation. No grace period. No exceptions.

Foreign-owned private limited companies carry the same annual filing obligations as local companies. But they also face additional requirements: BIDA reporting for foreign capital, Bangladesh Bank reporting for share issuances, and work permit renewals. The company types available to foreign investors in Bangladesh also shape certain compliance timelines. Branch offices have different AGM and reporting structures than private limited companies. For companies operating in special economic zones, BEZA and Bangladesh Hi-Tech Parks also carry their own layered compliance requirements on top of the standard filings.

Here’s the compliance timeline most private limited companies need to follow in a typical July-June fiscal year.

| Compliance Task | Deadline | Authority |

| Advance Tax — 1st installment | September 15 | NBR |

| Advance Tax — 2nd installment | December 15 | NBR |

| Monthly VAT Return | 15th of following month | NBR |

| Advance Tax — 3rd installment | March 15 | NBR |

| Advance Tax — 4th installment | June 15 | NBR |

| Annual General Meeting (AGM) | Within 15 months of previous AGM | RJSC |

| Annual Return Filing | Within 21 days of AGM | RJSC |

| Audited Financial Statements | Within 30 days of AGM | RJSC |

| Corporate Income Tax Return | January 15 (often extended by NBR) | NBR |

| Trade License Renewal | Annually (varies by City Corporation) | City Corporation |

The standard corporate tax return deadline is January 15 for companies following the July-June fiscal year. But the NBR regularly extends this. In 2024-25, the deadline was pushed from January 15 to February 15, then again to April 30, 2025. Always check the NBR’s latest orders before assuming the date.

Corporate income tax is the big one. Every company, branch office, liaison office, and joint venture registered in Bangladesh must file an annual income tax return with the National Board of Revenue.

The standard corporate tax rate is 27.5% for unlisted private companies, and 22.5% for listed companies. Startups meeting specific criteria under the Income Tax Act 2023 can qualify for a reduced minimum tax rate of 0.1% on gross receipts.

Filing goes through the NBR’s e-filing portal at etaxnbr.gov.bd. The return must be accompanied by audited financial statements, a withholding tax return, and a pay order for any remaining tax balance after deducting advance payments.

Bangladesh companies must pay advance income tax in four installments throughout the fiscal year: September 15, December 15, March 15, and June 15. Each payment is calculated on estimated annual income. The year-end return then reconciles these advance payments against actual tax liability.

Missing an installment doesn’t just result in a penalty. It triggers interest charges from the NBR that compound on the outstanding amount. A lot of founders only think about tax at year-end. By then, they’re already behind.

This is the one that surprises most new business owners. Even if your company reports a net loss for the year, you still owe a minimum tax of approximately 0.6% of gross turnover. So there’s no such thing as zero tax obligation simply because you’re not yet profitable.

Eligible startups under the Income Tax Act 2023 can apply for a lower rate of 0.1%, provided they meet turnover and ownership criteria. If you’re unsure whether you qualify, that conversation with your CA needs to happen before you file.

The RJSC compliance track is separate from the tax return, but equally important. Filing happens through the RJSC portal at roc.gov.bd.

Every company must hold an AGM every year. The first AGM must happen within 18 months of incorporation. After that, no more than 15 months can pass between two consecutive AGMs.

After the AGM, two things are due:

Annual Return: Filed within 21 days of the AGM, this includes details about shareholders, directors, capital structure, and the company’s auditor.

Audited Financial Statements: Filed within 30 days of the AGM. These must be prepared by a Chartered Accounting firm registered with ICAB and comply with Bangladesh Accounting Standards (BAS) and Bangladesh Financial Reporting Standards (BFRS).

A practical note: CA firms in Dhaka get fully booked around year-end filing season. If you wait until March to engage an auditor, you’ll be scrambling. Book them at least 60 days before your expected AGM date.

VAT registration becomes relevant once your company’s annual turnover crosses the NBR threshold. These thresholds have changed over time, so check them against the latest NBR guidance before you file. NBR’s current VAT compliance guidance states that many businesses with annual turnover above BDT 30 million may need VAT registration and a BIN. Some activities require VAT registration regardless of turnover.

Companies with annual supplies between BDT 8 million and BDT 30 million can enroll for Turnover Tax instead, at a simplified flat rate, rather than going through full VAT registration.

Monthly VAT returns must be filed using the Mushak 9.1 form by the 15th of the following month. Miss a month and penalties start stacking.

There’s also VAT Deduction at Source (VDS). Certain entities must deduct VAT when paying suppliers and remit it to the government. If you’re working with government buyers or large institutional clients, VDS becomes routine.

One thing worth flagging about your business bank account in Bangladesh: your RJSC-registered company name must match your BIN certificate perfectly. A single letter discrepancy can block VAT return submissions. I’ve seen clients spend weeks fixing what looked like a formatting issue but turned into a compliance hold.

The trade license is technically the simplest part of annual compliance in Bangladesh. You renew it every year through your local City Corporation or municipality.

But it’s also the one that catches people off guard. If your trade license lapses, it affects your ability to renew other certifications, particularly your VAT registration and import/export certificates.

Renewal fees range from BDT 100 to BDT 40,000, depending on business type and paid-up capital. The process typically takes 3-4 working days and requires your current TIN certificate and VAT registration.

Set a calendar reminder 30 days before your license expiry. City Corporations don’t send reminders, and nothing in the compliance chain works smoothly when this one expires.

This is the section most people skip until it’s too late.

Late RJSC annual return filing can result in fines of up to BDT 10,000 plus daily fines for continued non-compliance. Persistent non-filing can restrict future RJSC submissions and flag your company to banking and investment authorities.

On the tax side, late filing may trigger additional tax at 2% per month on the difference between assessed tax and tax already paid or deducted, calculated from after the due date until filing or assessment.

For VAT, operating above the BDT 30 million threshold without registration can trigger a legal notice and potential business suspension.

For listed companies, BSEC non-compliance under the investment banking regulations in Bangladesh is a different category entirely. It can mean fines, blacklisting, and in extreme cases, criminal liability for directors under the Securities and Exchange Commission rules.

Bangladesh’s compliance rules are strict when ignored. They don’t warn you twice.

A client of mine, a non-resident founder running a private limited company in Dhaka, nearly lost the ability to open a second bank account because their RJSC annual return hadn’t been filed for two consecutive years. These are the mistakes I see most often:

1. Confusing the RJSC annual return with the income tax return. They’re completely separate filings, with different deadlines, different authorities, and different document requirements.

2. Skipping advance tax installments. The four quarterly payments are easy to forget when revenue is uneven. Each missed installment means interest charges that compound from the due date forward.

3. Waiting too long to hire a CA. Your audited financial statements must comply with BAS. If the audit is rushed or poorly executed, errors follow you into the tax assessment process.

4. Not updating RJSC records after director or shareholder changes. Any change in the board or shareholding structure requires a separate return to the RJSC, independent of the annual return.

5. Letting the trade license lapse. An expired trade license creates a chain reaction that can freeze VAT renewal and delay import/export certificate processing.

The standard deadline for corporate income tax return filing in Bangladesh is January 15 for companies following the July-June fiscal year. Banks, insurance companies, financial institutions, and multinationals using the calendar year follow a different timeline. The NBR frequently extends this deadline. In 2024-25, the final extension moved it to April 30, 2025. Always check the latest NBR notification before assuming a date.

Companies must attach audited financial statements prepared by a registered CA firm, a withholding tax return, and a pay order for any remaining tax balance. The return itself includes business income details, advance tax payments made, minimum tax calculations, and principal financial figures from the audit.

If a company misses the RJSC annual return deadline (21 days after the AGM), penalties of up to BDT 10,000 can be imposed, with daily fines for continued non-compliance. Persistent non-filing allows the RJSC to flag the company, which can restrict future RJSC submissions and affect banking and investment standing.

Yes. Every company registered under the Companies Act 1994 must complete annual compliance. Foreign-owned private limited companies, branch offices, liaison offices, and joint ventures all follow the same RJSC and NBR obligations. Additionally, foreign companies often have extra reporting requirements to BIDA and Bangladesh Bank related to capital inflows, work permits, and profit repatriation.

Companies whose annual taxable supplies exceed BDT 30 million must register for VAT and obtain a Business Identification Number (BIN) from the NBR. Companies with annual supplies between BDT 8 million and BDT 30 million can enroll in a simplified Turnover Tax regime instead of full VAT registration.

Every company registered in Bangladesh must hold an AGM at least once per calendar year. The first AGM must be held within 18 months of incorporation. After that, no more than 15 months can pass between two consecutive AGMs.

Minimum tax in Bangladesh is a tax floor that applies even when a company reports a net loss. It’s calculated at approximately 0.6% of gross receipts or turnover for most companies. This means zero profit doesn’t mean zero tax obligation. Eligible startups under the Income Tax Act 2023 may qualify for a reduced minimum tax rate of 0.1%.

Partly. Corporate income tax returns can be submitted through the NBR’s e-filing portal at etaxnbr.gov.bd. RJSC company filings are handled through roc.gov.bd. However, audited financial statement preparation and some RJSC submissions still require coordination with a local CA firm and, in some cases, physical follow-up with RJSC offices.

Bangladesh companies must pay advance income tax in four quarterly installments: September 15, December 15, March 15, and June 15. Each payment is based on estimated annual taxable income. At year-end, the annual tax return reconciles these advance payments against actual tax liability. Missed installments attract interest charges from the date they were due.

No. Trade license renewal requirements and fees vary by business type, location (city corporation, municipality, or upazila), and paid-up capital. Commercial businesses and manufacturing entities use different application forms. Renewal fees range from BDT 100 to BDT 40,000, and processing typically takes 3-4 working days. A valid TIN and VAT certificate are required to complete the renewal.

Compliance isn’t the exciting part of running a business. Nobody launches a company dreaming about AGM windows and quarterly advance tax installments. The founders who stay out of trouble in Bangladesh are almost always the ones who treated compliance as a system, not a chore.

If I were starting fresh today, I’d hire a local CA within the first two months of incorporation and set up calendar alerts for every deadline listed in this guide. Those two moves alone eliminate most of the pain.

If you also operate a company outside Bangladesh, it’s worth understanding how compliance responsibilities stack. Comparing these requirements against annual compliance for US-based LLCs, for example, gives you a clearer picture of how to manage multi-jurisdiction obligations without things falling through the cracks.

Annual compliance in Bangladesh is manageable. The cost of ignoring it is not.

═══════════════════════════════════════════════════════════════ WRITER REVIEW LOG (Senior Staff Writer – Review & Finalization Pass) Date: 2026-06-06 | Serial: BM-DBL-06 | Post: 8557 STATUS: HELD – pending source verification ═══════════════════════════════════════════════════════════════ SCOPE OF THIS PASS (Option 2 – partial review): Non-factual editorial, cohesion, and value-add review only. No new factual claims added. No fact-checker ESCALATED item was marked verified. No citations or sources invented. Article is NOT frozen as content-final. It remains Draft / HELD pending verification of the statutory figures listed below. EDITORIAL / COHESION CHANGES MADE: 1. Internal-consistency fix (NOT a verification): The VAT registration threshold in the body referenced two different figures – “BDT 50 lakh” in one paragraph versus “BDT 30 million” in two others (the dedicated VAT-suspension paragraph and the FAQ). The outlier “BDT 50 lakh” was aligned to “BDT 30 million” so the article does not contradict itself. The existing hedge (“these thresholds have changed over time; check the latest NBR guidance before you file”) was kept. NOTE: the corrected figure itself is still UNVERIFIED and is listed as a HELD item below. This change resolves an internal contradiction only; it does not confirm the number is correct. VALUE-ADD REVIEW (no changes required): The non-resident / foreign-founder angle is already present and well placed (first-year obligation note; foreign-owned company extra requirements such as BIDA/BIN). The practical value-add items (hire a local CA early; RJSC company name must match the BIN certificate for banking) are present in the body and conclusion. No new content was needed and none was invented. HELD ITEMS – statutory / compliance figures NOT verified (14): These remain unverified because working web sourcing was unavailable during this pass (regulator pages returned 404s / served PDFs; general search was blocked). Each must be confirmed against an authoritative NBR / RJSC / Companies Act source before publishing. 1. RJSC annual return due within 21 days of the AGM 2. Audited financial statements due within 30 days of the AGM 3. First AGM within 18 months of incorporation; max 15 months between consecutive AGMs 4. Corporate income tax return deadline (stated Jan 15 for a July-June fiscal year) 5. Any FY2024-25 deadline extensions referenced 6. Corporate tax rates: 27.5% unlisted private / 22.5% listed 7. Startup minimum-tax rate of 0.1% (Income Tax Act 2023 criteria) 8. General minimum tax of approximately 0.6% 9. Advance tax installment dates: Sep 15, Dec 15, Mar 15, Jun 15 10. VAT registration threshold (now stated as BDT 30 million throughout after the consistency fix above) – figure unverified 11. Turnover Tax band: BDT 8 million to BDT 30 million 12. Monthly VAT return via Mushak 9.1 by the 15th of the next month 13. Penalties: RJSC fine up to BDT 10,000; 2% per month on unpaid tax 14. Trade license renewal fee range BDT 100 to BDT 40,000; processing 3-4 working days WHAT IS NEEDED TO CLOSE: Working web access OR authoritative source URLs for the 14 figures above. Once supplied, a follow-up pass can verify each, lift the HELD status, and only then consider content-final. AE (Writer Review Done): left EMPTY (never stamped while HELD). AF (Writer Review Status): HELD – 14 items need source verification. ═══════════════════════════════════════════════════════════════

Want to close a company in Bangladesh? Learn the legal steps, costs, timelines, and tax clearance requirements for a clean…

Get your Export Registration Certificate (ERC) in Bangladesh. Full document checklist, exact fees, online OLM steps, and renewal rules. Clear…

Bangladesh export incentives include cash assistance from 0.30% to 10% of FOB value across 43 sectors. Learn rates, eligibility, claim…