ICT Sector in Bangladesh: Growth, Exports, and Opportunities

An accurate overview of the ICT sector in Bangladesh: FY26 export data, top IT companies, freelancing figures, government policy, and…

A data-backed guide to the leather industry in Bangladesh: FY26 export figures, key challenges, government incentives, and what investors need to know in 2026.

Bangladesh has the raw material, the workforce, and the government support. But the leather industry in Bangladesh has been stuck near the $1 billion export mark for over a decade. That tension, between real potential and real structural problems, is exactly what this guide covers.

If you’re an investor, exporter, or researcher trying to understand where the sector actually stands, you’ll find the verified numbers and the honest picture here.

Quick answer: The leather industry in Bangladesh is the country’s second-largest export sector after ready-made garments. Total leather, leather goods, and footwear exports reached about $1.145 billion in FY2024-25, according to EPB data reported in May 2026. The sector includes over 200 tanneries and more than 3,600 footwear-making units, according to current BIDA sector data, and employs roughly 850,000 workers. The biggest growth bottleneck is the absence of Leather Working Group (LWG) certification, caused by an underperforming effluent treatment plant at the Savar Tannery Industrial Estate.

Bangladesh’s leather sector is bigger than most people picture. It’s not just tanneries. The industry runs across four main product segments: tannery output (raw and processed hides), finished leather, leather goods (bags, wallets, belts, jackets), and leather footwear.

The country has around 220 tanneries, approximately 140 of which are active, according to BIDA. The footwear segment includes over 3,500 small and medium enterprises, 90 large-scale firms, and produces roughly 378 million pairs annually. About 53% to 66% of that production goes to the domestic market, meaning the local demand base is substantial even without counting exports.

The sector employs around 850,000 workers, per BIDA’s investment profile. Bangladesh contributes approximately 1.13% of worldwide leather production and processes more than 180 million square feet of raw hides and skins each year. The country holds about 2.4% of the global livestock population, giving it a steady domestic supply of raw hides from cattle, goat, and buffalo. The input side of the value chain is genuinely strong. The processing and finished goods side is where things get complicated.

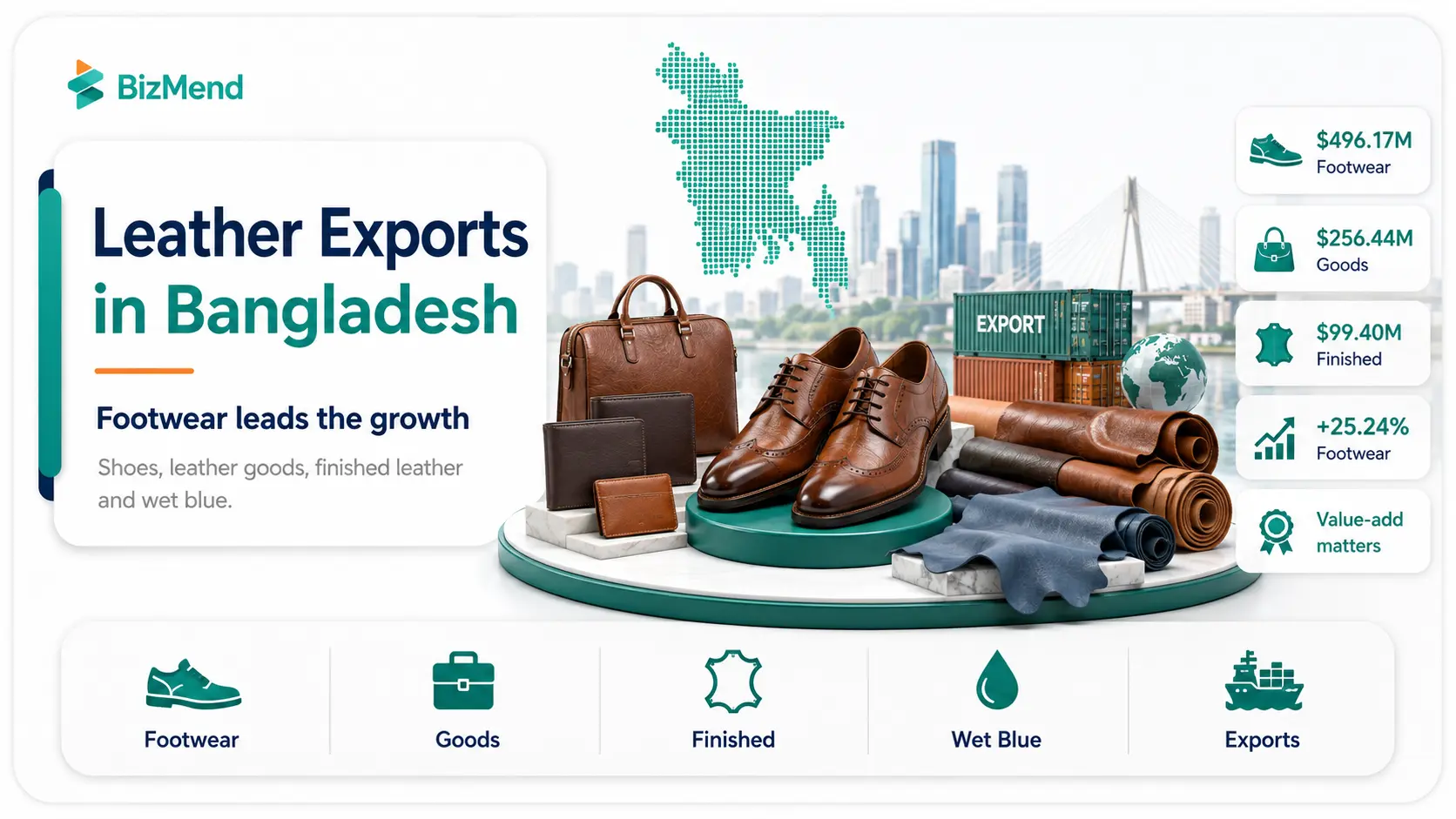

Footwear dominates. Leather shoes and boots made up roughly 58% of all leather-related exports between July 2024 and March 2025. Leather goods, including bags, wallets, belts, and travel accessories, come second. Finished leather and wet blue (semi-processed) hides round out the third major category.

Wet blue is the problem. Over 60% of Bangladesh’s export revenue from raw leather still comes from wet blue, which is semi-processed and commands much lower prices than finished leather goods. A significant amount of value is being left on the table.

Total leather exports between July 2024 and May 2025 reached $1,057.82 million, a 12.55% increase over the same period the previous year, according to EPB data reported by The Financial Express. For the full FY2024-25, total leather-sector exports reached about $1.145 billion.

| Segment | Exports (USD) | YoY Change |

|---|---|---|

| Leather footwear | $496.17 million | +25.24% |

| Leather goods | $256.44 million | -6.11% |

| Finished leather | $99.40 million | -6.29% |

| Total (Jul–Mar FY25) | $852.01 million | +9.89% |

Source: EPB data, The Financial Express (2025)

The headline growth looks decent. But the detail matters. Footwear is growing fast. Leather goods and finished leather are both shrinking.

Footwear exports to the US grew 74.1% to $209.61 million in the first seven months of 2025, per Otexa data. Bangladesh is now recognized as one of the world’s top 10 footwear producers, according to the World Footwear 2024 Yearbook.

Major brands currently sourcing from Bangladesh include H&M, Decathlon, Kappa, Neemans, Reebok, Walmart, Target, and Steve Madden. Global brands like Nike, Adidas, and Puma are reportedly shifting sourcing to South Asia as part of the broader China+1 trend, and Bangladesh is positioned to capture a meaningful share of that.

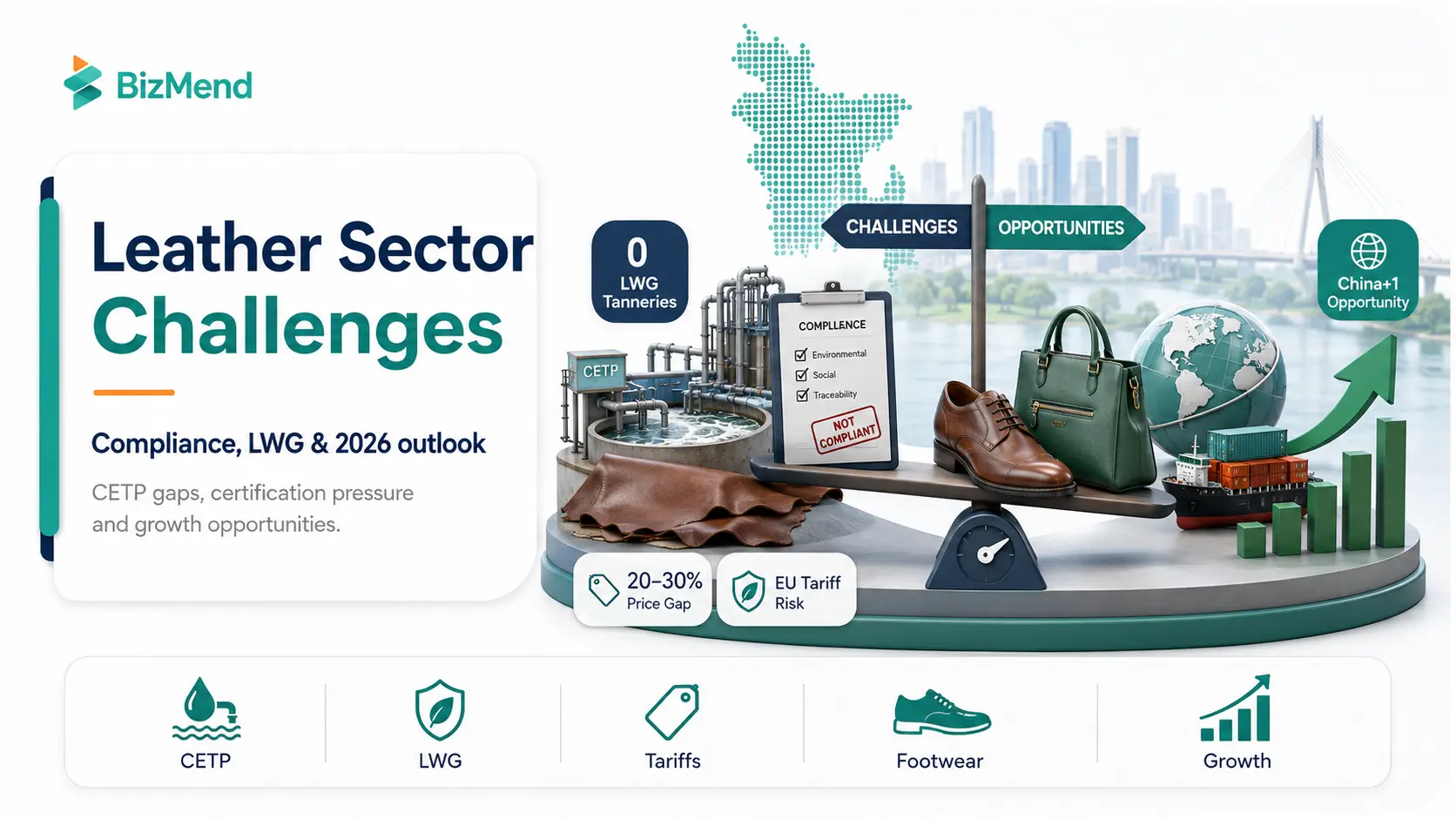

The short answer: compliance. Global buyers are increasingly avoiding Bangladeshi leather goods because the country’s tanneries can’t obtain Leather Working Group (LWG) certification, which is the accepted global standard for environmental performance in leather manufacturing.

Without LWG certification, Bangladesh sells into lower-end markets at discounted prices. According to Dr. M Masrur Reaz, Chairman of Policy Exchange Bangladesh, the absence of LWG certification forces Bangladesh to sell raw hides at 20% to 30% below what certified competitors can charge. India and Pakistan have far more LWG-certified leather facilities than Bangladesh, while Bangladesh still has very limited certified capacity and most Savar tanneries remain outside premium buyer requirements.

This is the issue underneath everything else. When tanneries were relocated from Hazaribagh in Dhaka, where they were causing severe pollution of the Buriganga River, to the Savar Tannery Industrial Estate (STIE), the plan included a Central Effluent Treatment Plant (CETP) that would handle waste and allow tanneries to meet international environmental standards.

The CETP still doesn’t work properly. Industry sources and Bangladeshi media consistently report that it continues to operate below international standards, releasing untreated water into the Dhaleshwari River. That means tanneries at Savar can’t get LWG certification. Without LWG, they can’t access premium European and US buyers. Without those buyers, exports stay flat.

According to Md Shaheen Ahamed, Chairman of the Bangladesh Tanners Association (BTA), non-implementation of social compliance and an ineffective CETP are pushing the formal tannery sector toward informality. Banks typically require clean environmental records before approving loans, making it harder for tanneries to invest in upgrades.

Industry experts have proposed placing the CETP under direct supervision of BEPZA or a new Leather Development Authority, and offering tax rebates and soft loans to tanneries pursuing LWG certification.

Despite the compliance challenges, the leather sector carries explicit priority status. The Leather and Leather Products Development Policy (2019) and the Export Policy 2024-27 both designate it as a high-priority industry. Current incentives include:

Three dedicated industrial estates are being developed for leather and tannery operations in Savar, Rajshahi, and Chattogram. Foreign investors can own 100% of a manufacturing business in most sectors. If you’re thinking about starting a business in Bangladesh as a foreigner, the leather sector is explicitly listed as a high-priority area with preferential policy treatment.

Understanding your company structure before committing matters. There are real differences between a private limited company, joint venture, and branch office setup. This guide on company types and restrictions for foreigners in Bangladesh explains the practical options. If you’re considering one of the dedicated leather industrial estates, the setup process for operating in Bangladesh’s economic zones and special parks is different from standard BIDA registration.

The shift of manufacturing investment away from China is ongoing. Bangladesh has already benefited from EU anti-dumping duties imposed on Chinese shoes. Chinese and South Korean companies have signed agreements to produce footwear and accessories inside Bangladesh EPZs, according to BEPZA data.

For investors specifically, the strongest opportunity is in finished leather goods and value-added footwear manufacturing for export to Europe and North America. The raw material base exists. The workforce exists. The gap is in compliance, product quality, design capability, and branding, which is also where the value-add is sharpest.

The top industries in Bangladesh for foreign investment overview confirms leather is one of the more actionable manufacturing opportunities for foreign capital right now, though it requires understanding the compliance environment.

Bangladesh graduates from Least Developed Country (LDC) status in 2026. When that happens, the duty-free and quota-free market access Bangladeshi exporters currently enjoy in many markets will begin phasing out.

After LDC graduation, Bangladesh’s EU EBA duty-free access is expected to continue during a transition period until 2029. After that, without GSP+ or another preferential arrangement, leather and footwear exports could face MFN tariff exposure. That’s a direct hit to price competitiveness for a sector already selling at a discount due to compliance gaps.

The UNDP has identified leather as a “critical post-LDC graduation growth engine” in its policy paper on the sector, but also notes the sector needs to move fast. Securing GSP+ status from the EU could partially offset the tariff impact, but GSP+ requires strict compliance with labor and environmental standards, which brings the conversation back to the CETP.

Getting the banking side right early matters too. This guide on how to open a business bank account in Bangladesh covers the practical steps for foreign investors. And for Bangladeshi entrepreneurs looking to set up a US holding company for access to US buyers and payment processors, starting a business in the USA from Bangladesh is a well-traveled route.

Bangladesh’s leather sector is the country’s second-largest export earner after ready-made garments. Total exports were approximately $1.03 billion in FY2025, per EPB data. The sector has around 220 tanneries, over 3,500 footwear manufacturers, and employs roughly 850,000 workers.

The sector has been unable to grow past $1 billion for over a decade due to the absence of LWG certification, an underperforming Central Effluent Treatment Plant at Savar, reliance on wet blue semi-processed leather instead of finished goods, and resulting limited access to premium buyers in Europe and North America.

The Savar Tannery Industrial Estate (STIE) is Bangladesh’s primary tannery hub, built when tanneries were relocated from Hazaribagh in Dhaka to reduce river pollution. It includes a Central Effluent Treatment Plant (CETP), though the plant continues to operate below international standards, preventing tanneries from obtaining LWG certification.

Leather Working Group (LWG) certification is the global environmental performance standard for leather manufacturers. Bangladesh’s tanneries can’t obtain it because the CETP at Savar doesn’t treat effluent to the required standard. India has over 150 LWG-certified tanneries, Pakistan over 80. Bangladesh has none, which forces the country to sell at 20-30% below certified competitors.

As of 2025: 50% tax exemption on export income (until June 30, 2028, per SRO No. 44/2024), no VAT on exported goods (SRO No. 180 Ain/2025/308 from June 2025), duty-free import of capital machinery, reduced Corporate Income Tax for 5-10 years by location (until June 30, 2030), and a For FY2025-26, Bangladesh Bank continued export cash incentives for 43 sectors; leather goods were among the categories eligible for up to 10% incentive for shipments between January 1 and June 30, 2026.

Yes, in most cases. Bangladesh allows full foreign ownership in leather manufacturing. Investors typically register through BIDA and may operate within dedicated leather industrial estates in Savar, Rajshahi, or Chattogram, which offer additional infrastructure and tax incentives.

After graduating from LDC status, Bangladesh will lose duty-free access in several markets. In the EU, leather footwear will face an MFN tariff of around 10% instead of the current zero. This directly cuts price competitiveness. Securing GSP+ status could partially offset the impact, but it requires meeting strict environmental and labor standards.

Current buyers include H&M, Decathlon, Kappa, Neemans, Reebok, Walmart, Target, and Steve Madden. Nike, Adidas, and Puma are reportedly shifting sourcing toward South Asia as part of the China+1 trend, representing a potential opportunity for Bangladesh’s footwear manufacturers.

Industry executives and analysts estimate exports could reach $5 billion annually by 2030 if long-standing infrastructure and compliance bottlenecks are resolved. Some projections suggest $10 billion by the mid-2030s. These figures assume significant reforms to the CETP, LWG certification, and value addition toward finished goods.

Key markets include Germany, the USA, Italy, Japan, France, Spain, the Netherlands, China, South Korea, and Canada. Exports to the US grew 74.1% to $209.61 million in the first seven months of 2025, making it one of the fastest-growing destinations for Bangladeshi leather footwear.

Bangladesh’s leather industry is one of those sectors where the gap between potential and performance is genuinely frustrating to study. The raw hides, low-cost workforce, established buyer relationships, and policy support are all there. The CETP and LWG certification failure is the single biggest reason this sector isn’t already a $3 to $5 billion story.

If you’re evaluating this as an investment, the China+1 shift and current tax incentives make the timing worth a serious look. Go in with clear eyes though: the compliance environment is improving slowly, LDC graduation is approaching fast, and the best positions will go to investors who account for those risks before committing.

An accurate overview of the ICT sector in Bangladesh: FY26 export data, top IT companies, freelancing figures, government policy, and…

Updated 2026 guide to agriculture in Bangladesh: GDP data, 2024 flood losses, fisheries rankings, agro-processing incentives, climate risks, and investment

A data-backed guide to the top industries in Bangladesh. Covers RMG, pharma, IT, agriculture, leather, shipbuilding, and the economic risks…