Grameen Bank Bangladesh: The Microfinance Model That Changed Banking

Learn how Grameen Bank began its journey in Bangladesh. How its revolutionary microfinance model works and why it still matters.

Learn how microfinance in Bangladesh began, which MFIs shape the sector, and how loans, regulation, and the Grameen model work in practice.

Bangladesh changed global finance with very small loans. That sounds dramatic. It’s also why microfinance in Bangladesh still draws students, policymakers, and skeptics alike.

What began in Jobra in 1976 grew into a national system of village lending, savings collection, and women-centered outreach that now reaches tens of millions. If you want to understand Bangladesh, its development sector, or the Grameen model itself, microfinance is a topic you cannot skip. This guide follows the history, institutions, rules, and lending mechanics people often hear about but rarely see explained clearly.

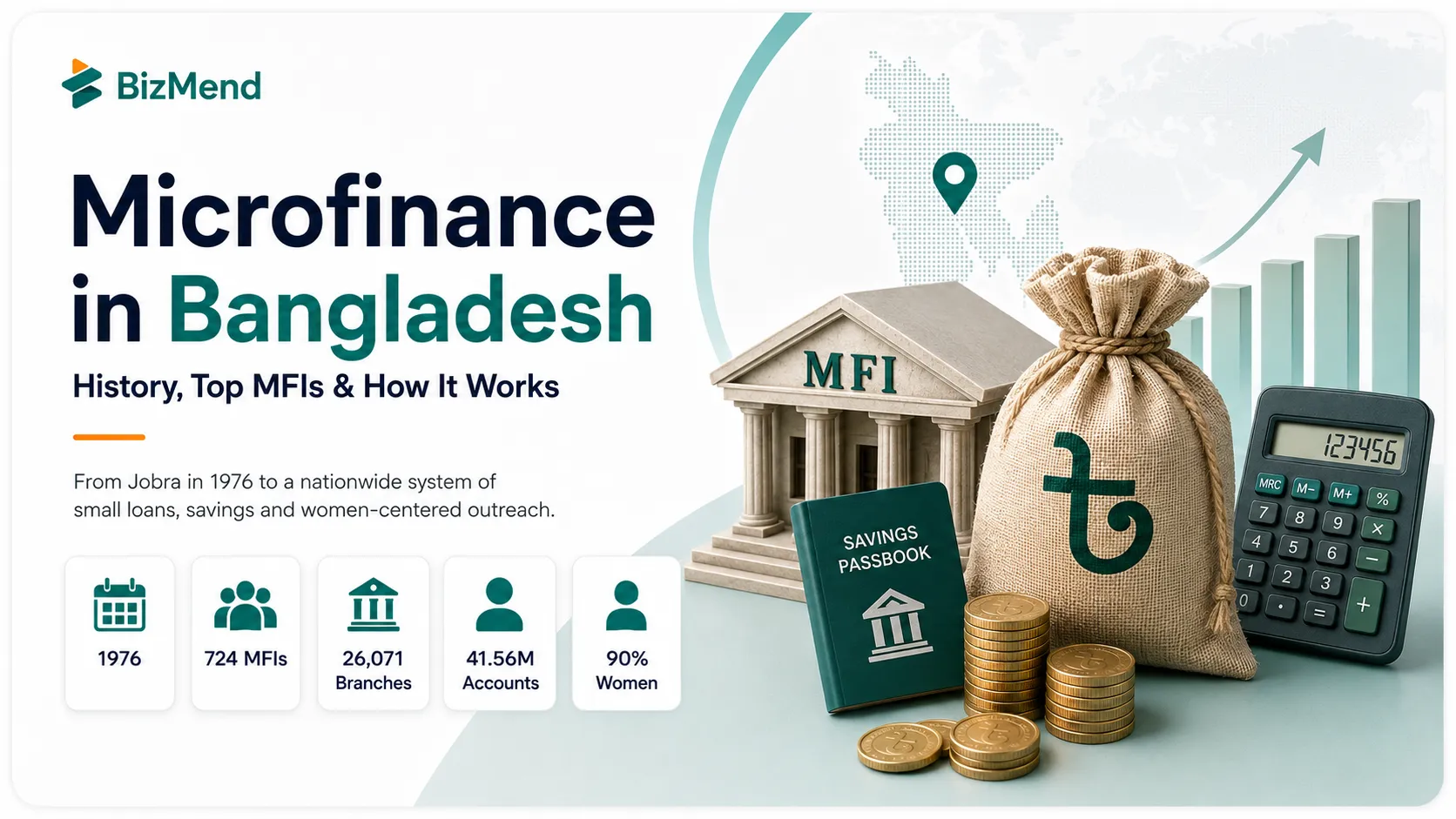

Quick answer: Microfinance in Bangladesh is a nationwide system of small loans, savings, and related services delivered mainly by licensed NGO MFIs and Grameen Bank. The sector grew from Muhammad Yunus’s 1976 experiment and, by December 2024, 724 licensed MFIs were operating through 26,071 branches under MRA oversight.

At its simplest, microfinance means giving small-scale financial services to people who are usually ignored by formal banking. In Bangladesh, that often means rural women, informal workers, tiny traders, farmers, or first-time entrepreneurs who cannot offer land deeds, salary slips, or the kind of collateral a bank branch would ask for.

The word matters because it is wider than microcredit. Credit is the loan. Microfinance includes the whole toolkit around that loan: savings, insurance, repayment discipline, financial records, and sometimes business support. Bangladesh Bank’s 2024 Financial Stability Report said licensed MFIs had more than 41.56 million account holders and 32.18 million borrowers, which tells you the sector is not a side story anymore.

Most institutions still work through community-level relationships rather than polished branch lounges. Field staff meet members close to where they live or trade. That lowers travel cost for clients, but it also shapes the whole culture of the sector: frequent contact, small ticket sizes, repeat borrowing, and strong pressure to keep repayment regular.

The usual starting point is Jobra village near Chattogram, where Muhammad Yunus began lending tiny sums to poor borrowers in 1976. The idea was plain: if a working woman needed only a small amount to buy bamboo, clay, or raw material, the lack of credit was not a side problem. It was the trap itself.

The experiment widened through a Bangladesh Bank supported project in 1979, then became a formal bank when the Grameen Bank Ordinance created Grameen Bank in 1983. Bangladesh did not stop at one institution, though. BRAC had launched its own large scale microfinance work in 1973, ASA pivoted toward its now famous low cost model in 1991, and PKSF was set up in 1990 as an apex funding body for partner organizations.

| Year | What happened |

|---|---|

| 1976 | Muhammad Yunus starts the Jobra village lending experiment. |

| 1979 | The model expands through a Bangladesh Bank backed project. |

| 1983 | Grameen Bank is formally established by ordinance. |

| 1990 | PKSF is created to finance and support partner organizations. |

| 2006 | The MRA Act creates the regulator for NGO MFIs. |

| 2006 | Muhammad Yunus and Grameen Bank win the Nobel Peace Prize. |

| 2024 | Bangladesh Bank reports 724 licensed MFIs and 26,071 branches. |

Regulation came later than the early growth wave. The Microcredit Regulatory Authority Act was passed in 2006, creating the MRA as the sector’s formal watchdog for NGO MFIs. That same year, the Nobel Peace Prize went jointly to Muhammad Yunus and Grameen Bank. One year gave the story both prestige and pressure: global admiration on one side and much closer scrutiny on the other.

Bangladesh did not just popularize microfinance. It gave the modern model its public identity.

There is no single perfect league table because institutions differ by legal form, client count, savings base, branch footprint, and product mix. Still, a handful of names show up again and again when you study Bangladesh’s sector because of their scale, history, or influence.

| Institution | Why it matters | Current indicator |

|---|---|---|

| Grameen Bank | Foundational institution linked to the original global model. | Official site says it works through 2,568 branches in 81,678 villages and serves 9.83 million members, 96.43 percent of them women. |

| BRAC Microfinance | One of the world’s biggest and most diversified microfinance programs. | BRAC says 11.4 million people accessed microfinance services through it in 2025, with 8 million using USD 6.6 billion in microloans. |

| ASA Bangladesh | Known for a stripped-down, low-cost operating model that many others studied. | ASA says it currently serves 7.2 million clients in Bangladesh and remains one of the country’s largest MFIs. |

| BURO Bangladesh | Large nationwide network with a strong financial services focus. | BURO says it serves 2.6 million active customers, 1.9 million active borrowers, and operates 1,410 branches. |

| TMSS | A major women focused NGO with an integrated health, education, and microfinance approach. | TMSS says its HEM model runs through 1,022 branches and reaches nearly 1,814,278 members. |

If you’re trying to picture the model on the ground, think less about a glossy bank counter and more about a repeated local cycle. A borrower joins, saves a little, takes a modest loan, repays in small installments, and becomes eligible for future products if repayment stays steady. The engine is repetition, not one dramatic disbursement.

The classic Grameen approach used five member groups and center meetings, but modern practice in Bangladesh is broader. Many MFIs now mix group based methods with individual loans, microenterprise finance, mobile collections, and products built around crop seasons or irregular cash flow.

The real engine is repetition: borrow, repay, save, borrow again.

Microfinance grew in Bangladesh because the formal banking map left huge blank spaces. Many low-income households had income, skills, and business ideas, but no practical way to turn those into usable finance. A local MFI worker with a passbook and a repayment schedule could reach villages, chars, peri-urban settlements, and women borrowers that commercial banks often never served well.

That reach mattered beyond money. Regular savings gave households a way to smooth shocks. Small enterprise loans helped tiny shops buy stock. Agricultural and seasonal products helped clients match repayment to harvest cycles. The sector also helped normalize the idea that poor women are bankable economic actors, not passive aid recipients. Bangladesh Bank’s 2024 sector snapshot, with roughly 90 percent women account holders, shows how central that gender shift still is.

A regular bank loan and a Bangladeshi microfinance loan can both fund a business, but the experience is usually very different. A bank may ask for collateral, formal statements, trade licenses, guarantors, and a longer approval trail. A microfinance institution is more likely to start with local knowledge, field visits, repayment history, and a smaller first loan that fits the borrower’s real cash rhythm.

That difference is exactly why the sector got so large. For many clients, the question was never whether a bank product looked cheaper on paper. The real question was whether the household could access that product at all. Microfinance won its place by being reachable, understandable, and repeatable, even when the ticket size was small and the repayment discipline felt strict.

Let’s not romanticize it. A system this large creates real pressure points. Critics worry about multiple borrowing, aggressive collection behavior, shallow enterprise returns, and clients taking a new loan partly to calm the old one. Those worries are not fringe anymore. TMSS itself highlighted the debt spiral question in a 2026 seminar, and the sector’s new Microfinance Credit Information Bureau reflects the same concern from a regulatory angle.

The other big shift is digital. MRA and IFC announced a modernization push in 2024, and several large institutions now talk openly about app-based service, identity verification, and tighter data systems. That could help with borrower protection and efficiency if it is done well. If done badly, it could just make a high-pressure system faster. So the next chapter is not about whether Bangladesh invented a powerful model. It is about whether the country can update that model without losing sight of the people it was built for.

Microfinance in Bangladesh is neither a miracle story nor a failed idea. It’s a living financial system with deep roots, global influence, huge reach, and very real tensions. If you want to understand why it still matters, start with that balance: bold innovation, hard discipline, mass inclusion, and an unfinished debate about what fair finance should look like.

Because the modern model took shape there. Muhammad Yunus began the Jobra experiment in 1976, Grameen Bank was formalized in 1983, and Bangladesh later became the best known global reference point for village based small loan programs.

No. Grameen Bank is a distinct institution created by ordinance, while many other providers are NGO MFIs regulated by the MRA. They share some lending logic, but their legal form, product design, and operating methods can differ a lot.

For NGO MFIs, the core regulator is the Microcredit Regulatory Authority, created under the 2006 law. Bangladesh Bank also matters indirectly because of broader financial stability work and technical support such as the Microfinance Credit Information Bureau.

Not anymore. Women remain central, but many institutions now offer microenterprise, agriculture, migration, sanitation, housing, savings, and digital services. Some still rely heavily on group structures, while others use more individual and product specific lending formats.

Borrower protection is probably the sharpest issue. Researchers and practitioners keep returning to multiple borrowing, debt stress, repayment pressure, and whether digital systems and credit data can improve the quality of lending instead of only expanding its speed.

Learn how Grameen Bank began its journey in Bangladesh. How its revolutionary microfinance model works and why it still matters.

Learn how BRAC microfinance works in Bangladesh, including loan products, borrower fit, documents, and what to check before applying.

Microcredit in Bangladesh is small money with big consequences. It can stock a tea stall, buy a sewing machine, or…