Advance income tax in Bangladesh sounds simple until you try to match the phrase to the actual law. The system expects part of your tax to be paid during the financial year, not only when the return is filed. The confusion gets worse because many people also use AIT for import-stage tax collected at customs, which is related but not the same question.

If you run an SME, manage finance, or review tax papers, that distinction matters because quarterly advance tax and import-stage credits do not behave the same way. This guide breaks down who usually pays, the four due dates, how the amount is estimated, and what late payment can cost.

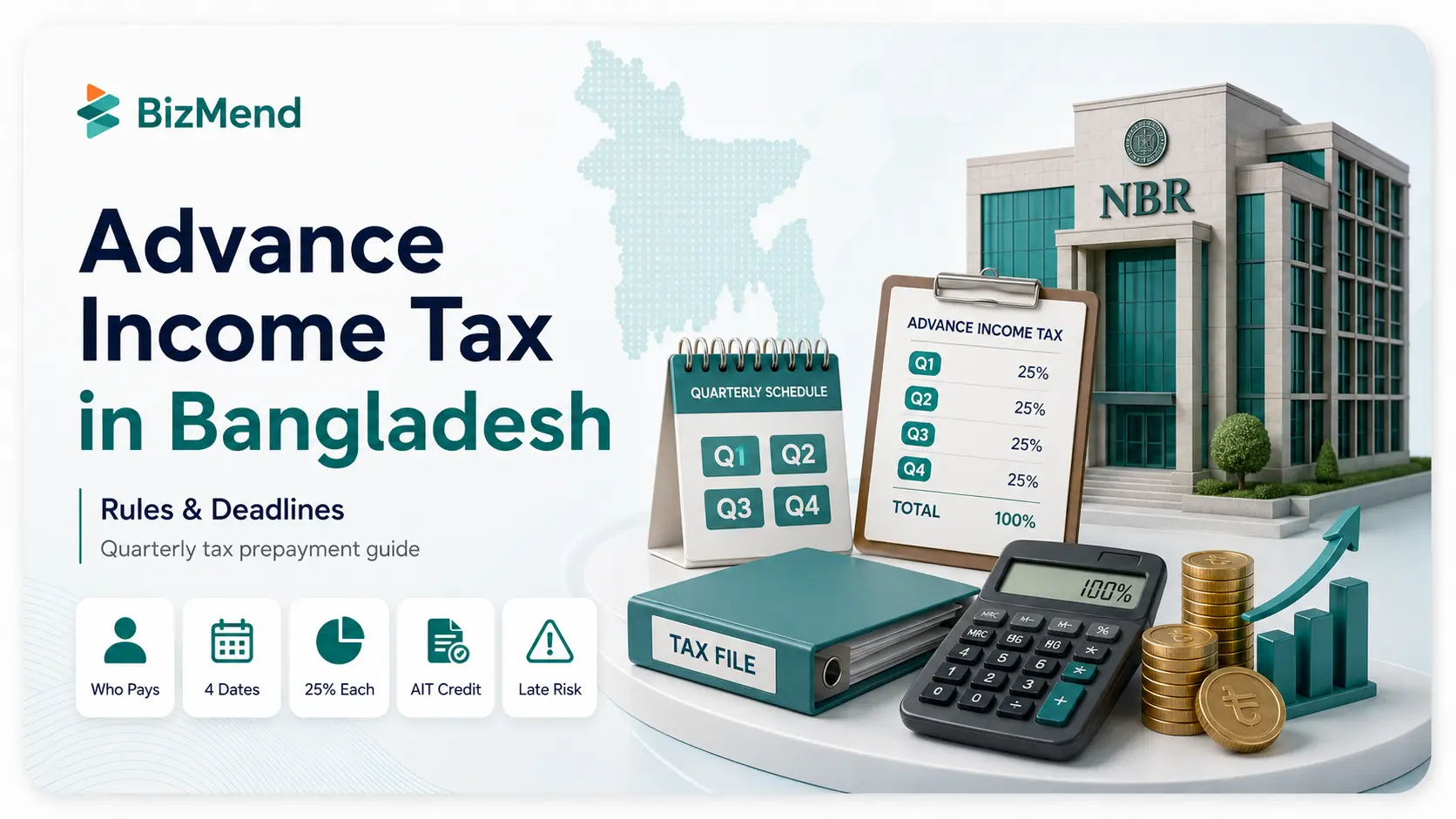

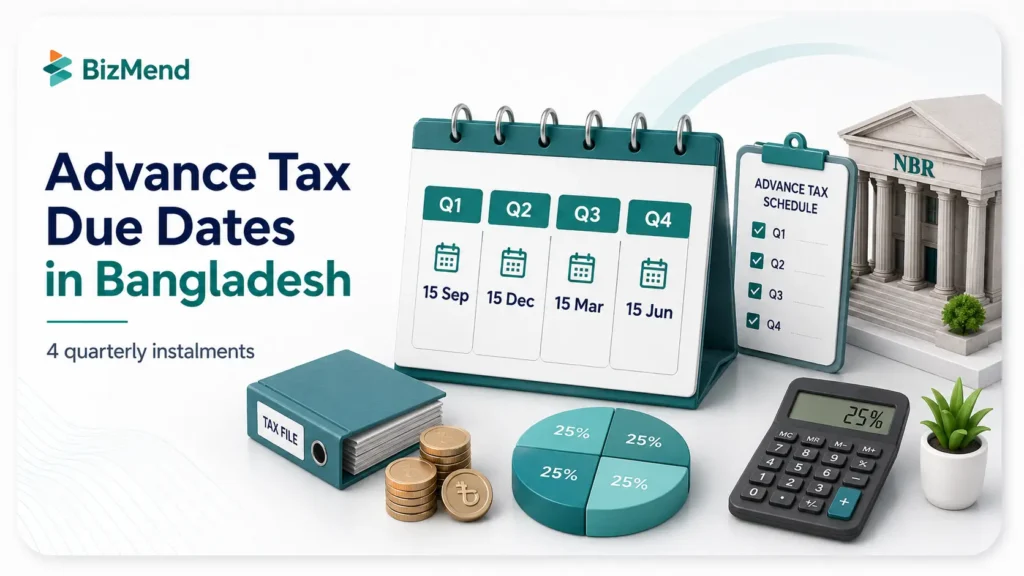

Quick answer: In Bangladesh, advance income tax usually means paying income tax in four 25% instalments on 15 September, 15 December, 15 March, and 15 June under the Income Tax Act, 2023. Importers may separately see AIT as a credit in the NBR return.

Key Takeaways

- Advance income tax is normally a prepayment of your yearly income tax, not a separate extra tax.

- The core trigger in the Income Tax Act, 2023, is whether your latest income year exceeded BDT 600,000.

- The standard payment rhythm is four equal installments due on 15 September, 15 December, 15 March, and 15 June.

- If your income changes during the year, the law lets you revise the estimate instead of blindly following last year’s number.

- A missed installment does not vanish; it rolls into the next one and can expose you to default consequences and interest.

- If advance tax plus tax deducted or collected at source stays below 75% of assessed tax, interest can apply at assessment stage.

- Importers often use the term “AIT” for customs-stage income tax credit, which is why many finance teams mix up two different rules.

- Good recordkeeping matters because advance tax payments and import-stage AIT credits both need clean reconciliation in the return.

What Advance Income Tax in Bangladesh Means

At the legal level, advance income tax is the part of your income tax that Bangladesh expects you to pay during the financial year instead of waiting for the final return. Section 154 of the Income Tax Act, 2023, ties that rule to taxpayers whose latest income year exceeded BDT 600,000. Think of it like rent paid monthly instead of a giant bill at the end of the lease.

That sounds simple until everyday business language gets in the way. In many offices, people say “AIT” when they mean the income tax collected at the import stage. NBR itself highlighted that import-side issue again on 18 January 2026 when it launched automatic crediting of import-stage income tax into e-returns. So yes, the same three letters often point to two related but different workflows.

| Term people use | What it usually means | Why it matters |

|---|---|---|

| Quarterly advance tax | Prepaying yearly income tax in four installments under sections 154 to 157. | It affects cash planning, due dates, and interest exposure. |

| Import-stage AIT | Income tax collected during import and later shown as a tax credit in the return. | It affects customs costs, credit matching, and return reconciliation. |

| Advance tax under VAT | A separate import-side concept in the VAT system, often discussed alongside AIT. | It adds another layer of naming confusion for finance teams. |

Who Usually Has to Pay

For an existing taxpayer, the first screening question is blunt: Did your latest income year exceed BDT 600,000? If yes, section 154 says tax is payable during the financial year as advance tax, unless a specific exclusion applies. That is why many businesses get pulled into quarterly payments even before they have sat down to prepare the next return.

- A previously assessed taxpayer generally looks at the latest income year and the tax already deducted or collected at source.

- A first-time taxpayer who is likely to cross BDT 600,000 must estimate income before 15 June and pay remaining installments that have not yet expired under section 156.

- A person earning only cultivation income up to BDT 800,000 is carved out by section 154.

- Capital gains and one-time income are specifically excluded from the advance-tax base under section 154(2), which matters for taxpayers with unusual gains in a single year.

In practice, that means many SMEs, company directors, traders, professionals, and import-heavy businesses should not assume this is a rule for giant corporations only. If your tax profile already exists, the system expects you to stay ahead of the bill. Waiting for year-end is where the trouble usually starts.

How the Amount is Worked Out

Section 155 says the minimum advance tax for the current financial year starts with the tax payable on your last income year, computed at the rate applicable in the current financial year. Then you subtract tax already deducted or collected at source, plus any advance tax paid under Part 7. So the law is not asking you to pay the same tax twice. It is asking you to prepay the balance that still looks likely.

Advance tax is not a bonus bill. It is your annual tax bill, arriving early in four envelopes.

The good news is that the law also recognizes that business forecasts move around. Section 155(5) lets you revise the estimate if the original figure is likely to be off. That matters for businesses with uneven revenue, project-based billing, import spikes, or a rough first half followed by a strong finish.

- Suppose your last income year produced BDT 1,200,000 in tax when recalculated at the current year’s rate.

- Suppose BDT 300,000 is already expected to be covered by tax deducted or collected at source.

- Your minimum advance tax base would then be BDT 900,000.

- Split equally, each installment would start at BDT 225,000 unless a revised estimate changes the later quarters.

That is why your working paper matters so much. If the source-tax numbers are wrong, or import-stage credits do not reconcile properly, the quarterly math goes crooked very fast. A clean schedule at the start of the year saves a lot of apologetic phone calls later.

When to Pay and How the Timeline Works

Bangladesh keeps the schedule straightforward: four equal installments, one every quarter. Section 155 fixes the dates, and it also says that if one lands on a public holiday, the next working day becomes the due date. If you miss one, the unpaid part compounds with the next installment instead of politely disappearing.

| Due date | Normal share of annual advance tax | Practical note |

|---|---|---|

| 15 September | 25% | Often the first real pressure point after early-year forecasting. |

| 15 December | 25% | A missed September amount can spill forward here. |

| 15 March | 25% | This quarter often catches businesses with weak cash forecasting. |

| 15 June | 25% | The final quarterly cleanup before the next cycle turns over. |

How Businesses Usually Pay in Practice

On paper, this is just a tax rule. In practice, it is an operations habit. Since 2023, NBR has pushed tax payments through electronic rails, and businesses commonly handle advance payments through the NBR e-tax setup, authorized banking channels, and the e-return ecosystem. That means the payment itself is only half the job. The other half is making sure the ledger, challan, and return all agree with each other.

Importers need to be even more careful here because import-stage AIT can sit in the same mental bucket as quarterly advance tax. NBR’s January 2026 automation helped by making import-stage income tax credits appear in the e-return. Still, auto-credit is not a magic eraser. If the customs data, taxpayer identity, or supporting records are off, someone still has to trace the mismatch.

- Keep every challan and bank confirmation in a one-year-wise folder.

- Reconcile source tax, quarterly advance tax, and import-stage AIT before return drafting starts.

- Review whether a revised estimate is needed after large revenue swings, one-off contracts, or import shocks.

- Match the taxpayer identification details across customs, banking, and tax records so credits do not drift.

What Happens If You Pay Late or Pay Too Little

This is the part people tend to notice only after it hurts. Section 157 treats the unpaid installment as a default. Section 162 then adds another risk at assessment stage: if your advance tax plus tax deducted or collected at source is less than 75% of the assessed tax, simple interest applies at 10% a year on the shortfall. If the return misses Tax Day, that interest rate rises by 50%.

A missed quarter does not disappear. It rolls forward, and the interest clock keeps its own notes.

- Cash flow pain arrives twice: once when the missed installment catches up and again when interest is computed.

- A weak estimate is better than no estimate, but a stale estimate left untouched for months can become expensive.

- Late payment risk is not only about money. It also creates messy reconciliation work when the return is prepared.

There is one small balancing point in the law. Section 161 says the government pays 10% yearly interest on excess advance tax. So if you overpay, the amount is still credited and the law does not pretend your extra cash had no time value. That said, most businesses would still rather keep their forecasting tight than lend money to the system by accident.

Checklist for SMEs and Finance Leads

- Check whether the latest income year crossed BDT 600,000 and whether any Section 154 exclusion applies.

- Prepare a simple tax forecast at the start of the financial year using last year’s tax and expected source-tax credits.

- Mark 15 September, 15 December, 15 March, and 15 June in the finance calendar with an internal reminder a week earlier.

- Review the estimate after big events such as a major contract, large import cycle, or sudden drop in revenue.

- Store payment evidence immediately and reconcile it against the e-return ledger instead of waiting until filing season.

- If your business imports goods, separate quarterly advance tax from import-stage AIT in your working papers so one does not get mistaken for the other.

None of this is glamorous. It is bookkeeping with legal consequences. But once the process is built, advance tax stops feeling like a surprise attack and starts behaving like a calendar task.

Final Thoughts

Advance income tax in Bangladesh is easier to handle once you separate the language from the law. Know whether you are dealing with quarterly prepayments, import-stage credits, or both. Then the job is simple: estimate honestly, pay on time, reconcile carefully, and revise when the year changes shape.

Frequently Asked Questions

Is advance income tax the same as regular income tax in Bangladesh?

No. It is usually a prepayment of regular income tax during the financial year. The final tax position still gets settled through the return and assessment process, where advance payments and source-tax credits are adjusted against the actual liability.

Who needs to pay advance income tax in Bangladesh?

A taxpayer whose latest income year exceeded BDT 600,000 generally falls into the rule under Section 154 of the Income Tax Act, 2023, unless a listed exclusion applies. A new taxpayer likely to cross that level may also need to estimate and pay under section 156.

What are the advance income tax due dates in Bangladesh?

The standard dates are 15 September, 15 December, 15 March, and 15 June, with 25% of the annual advance tax amount due each time. If a date falls on a public holiday, the next working day applies under section 155.

Can I change the amount later if my business income changes?

Yes. Section 155(5) allows a revised estimate when the original number no longer reflects the likely tax for the year. That is especially useful for businesses with uneven sales, project income, or import-heavy cycles.

What happens if I pay less than required?

You may be treated as in default for the missed installment, and interest can apply if advance tax plus tax deducted or collected at source ends up below 75% of assessed tax. The law currently states 10% yearly simple interest, with a 50% increase if the return misses Tax Day.