Most international trade money in Bangladesh doesn’t move by wire transfer or cash. It moves through a Letter of Credit. Whether you’re importing machinery from China, exporting garments to Germany, or sourcing fabric for your factory, you’ll almost certainly deal with an LC. Yet most new traders only have a foggy idea of what it actually is or how the money flows. This guide breaks down letter of credit in Bangladesh from the ground up: what it is, how it works step by step, which types matter most, the documents involved, and the 2025 regulatory changes that affect every importer and exporter.

Quick answer: A letter of credit (LC) in Bangladesh is a bank’s written guarantee that an importer’s payment will reach the exporter once compliant shipping documents are presented. Governed by UCP 600 (ICC) and regulated by Bangladesh Bank, LCs are the standard payment method for most commercial imports in Bangladesh. Key types include sight LC, usance LC, and back-to-back LC, which is critical for the garment industry.

What is a letter of credit in Bangladesh?

An LC, also called a documentary credit, is a commitment from a bank. Specifically, the importer’s bank promises to pay the exporter a fixed amount once the exporter presents the correct shipping documents.

Think of it as a trust bridge. The exporter doesn’t trust the buyer to pay once the goods ship. The buyer doesn’t trust the seller to ship quality goods on time. The LC puts a bank in the middle. The exporter gets paid when documents match. The buyer only releases money when documents are verified.

Bangladesh Bank requires most commercial imports to be settled through irrevocable LCs, meaning neither party can cancel or amend the LC without everyone’s agreement. All LCs in Bangladesh operate under UCP 600, the Uniform Customs and Practices for Documentary Credits issued by the International Chamber of Commerce (ICC), which came into force on July 1, 2007.

The Import and Export (Control) Act, 1950 provides the broader legal framework governing trade, while Bangladesh Bank’s Foreign Exchange Policy Department (FEPD) regulates how Authorized Dealer (AD) banks handle LC transactions.

How an LC works in Bangladesh, step by step

The four main parties in every LC

Before walking through the steps, you need to know the players:

- Applicant: The importer (buyer) in Bangladesh who requests the LC from their bank

- Issuing bank: The importer’s Authorized Dealer bank that creates and issues the LC

- Beneficiary: The exporter (seller) overseas who receives payment under the LC

- Advising bank: The exporter’s bank in their country that receives the LC from the issuing bank and informs the exporter

A confirming bank is sometimes added. This is a second bank (usually in the exporter’s country) that adds its own payment guarantee on top of the issuing bank’s. Exporters dealing with less familiar Bangladeshi banks sometimes require this.

The step-by-step flow from contract to payment

- Buyer and seller agree on terms. The exporter sends a Proforma Invoice (PI) or Indent to the importer stating the product, quantity, price, and payment terms.

- Importer applies to their bank. The importer goes to their Authorized Dealer bank with the PI, their Import Registration Certificate (IRC), trade license, TIN, and other required documents, and completes the LC application.

- Bank assesses and issues the LC. The bank checks the importer’s credit history, collects a margin deposit, and issues the LC. The bank then transmits the LC to the exporter’s advising bank, typically via SWIFT.

- Advising bank informs the exporter. The exporter’s bank notifies the exporter that the LC has been opened and is available.

- Exporter ships the goods. Once satisfied with the LC terms, the exporter ships the goods and collects all required shipping documents.

- Exporter presents documents to their bank. The advising bank checks the documents and forwards them to the issuing bank in Bangladesh.

- Issuing bank examines documents. The bank compares each document against the LC terms. Under UCP 600, banks have 5 banking days to examine documents.

- Payment is released. If documents comply with LC terms, the issuing bank pays the exporter’s bank. The importer then collects the documents to take delivery of the goods at Chattogram Port or wherever the shipment arrives.

If you’re new to starting an import business in Bangladesh, understanding this flow is the single most important piece of financial knowledge you need before your first shipment.

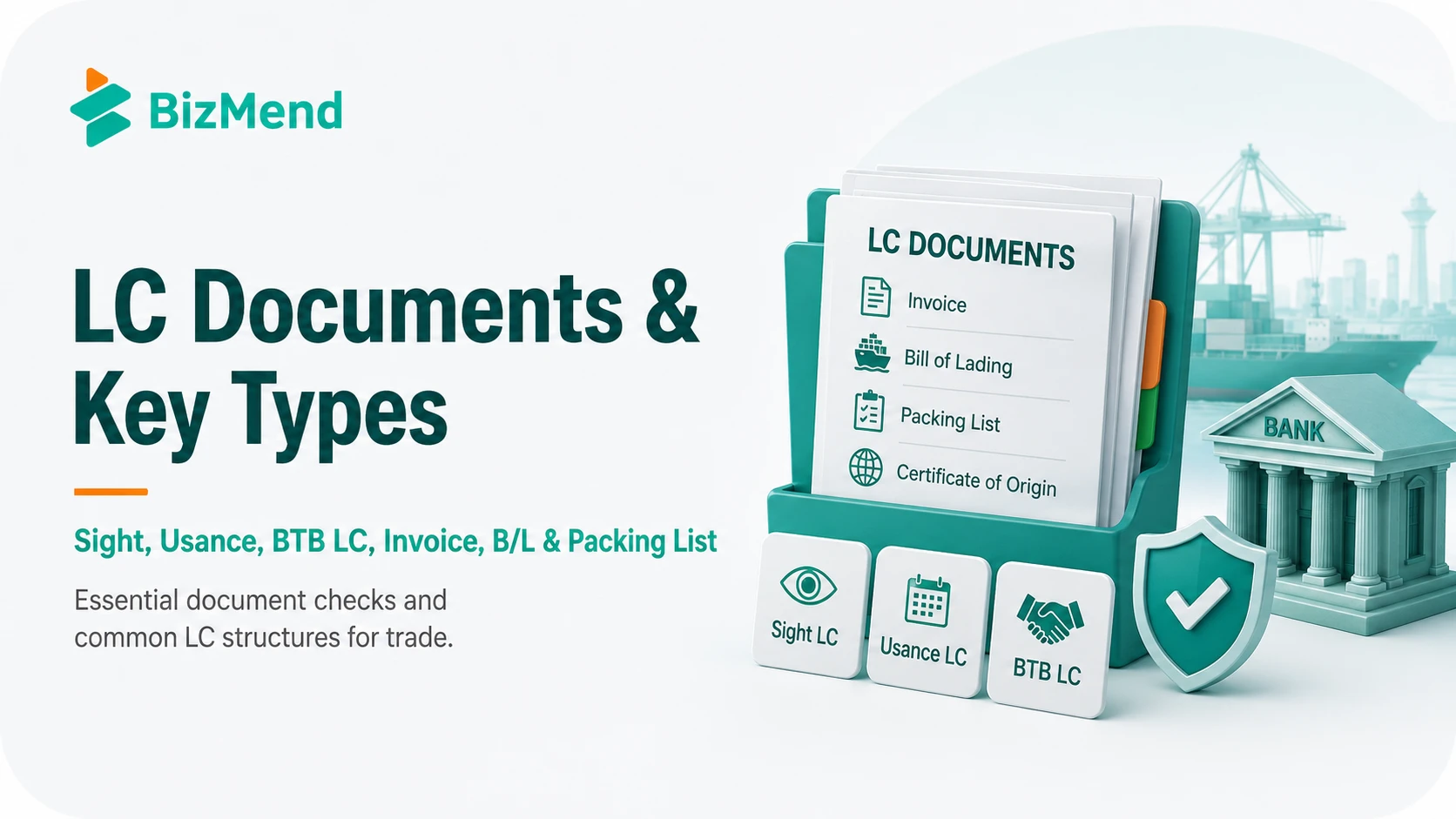

Types of LC used in Bangladesh

Not all LCs work the same way. The type you use depends on what you’re importing, whether you’re a manufacturer or trader, and what payment terms you’ve agreed with your supplier.

- Sight LC: Payment is made immediately once the issuing bank verifies the documents. The exporter gets paid fast. This is the most secure for exporters but can tie up the importer’s cash.

- Usance (Deferred) LC: Payment is made at a future date, typically 30, 60, 90, 120, or 180 days after the sight or shipment date. The importer gets time to sell goods before paying. Also called a time LC or deferred payment LC.

- Back-to-Back LC (BTB LC): A second LC opened by an exporter against an incoming master export LC, used to import raw materials needed for production. Critical in Bangladesh’s garment industry. Covered separately below.

- Transferable LC: The first beneficiary (usually a middleman) can transfer the LC to a second beneficiary (the actual manufacturer). Useful in triangle trade.

- Standby LC: Functions like a performance guarantee. It’s drawn only if the applicant fails to meet their obligation. Less common in everyday trade but used in project and service contracts.

Documents needed to open an LC in Bangladesh

Before your bank can open an LC, you’ll need to submit a specific set of documents. Incomplete or expired documents are the most common reason LC applications get delayed.

Core documents required by Authorized Dealer banks:

- Valid Import Registration Certificate (IRC)

- Valid Trade License

- TIN Certificate and VAT Registration (BIN)

- Completed LC Application Form

- IMP Form (Import Merchandised Permit Form)

- Proforma Invoice, Indent, or Purchase Contract from the supplier

- Insurance Cover Note

- Charge documents: Demand Promissory Note, Letter of Guarantee, and other bank-specific forms

- CIB report (your bank pulls this from Bangladesh Bank’s Credit Information Bureau to verify your creditworthiness)

- Membership Certificate from a Chamber of Commerce or relevant trade association (for commercial imports)

For an Import Registration Certificate in Bangladesh, the application goes through CCI&E’s Online Licensing Module at olm.ccie.gov.bd.

Documents required for payment under an LC

Once the goods ship, the exporter must present specific documents to their bank. If these don’t match the LC terms exactly, the bank can refuse payment. This is called a discrepancy.

Standard shipping documents under a typical LC include:

- Commercial Invoice: Must match the LC in terms of amount, currency, description, and buyer/seller details

- Bill of Lading (sea freight) or Airway Bill (air freight): Proof of shipment

- Packing List: Detailed breakdown of the shipment contents

- Certificate of Origin: Shows where the goods were made, often required by customs

- Insurance Certificate or Policy: Confirming the goods are insured

- Inspection Certificate: Required by some LCs to verify quality before shipment

The LC itself specifies exactly which documents are required and in what format. The exporter must present everything within the validity period of the LC and usually within a set number of days after shipment (21 days is the default under UCP 600 if the LC is silent on the matter).

Choosing the right Authorized Dealer banks in Bangladesh matters here. Banks with strong international trade finance desks process documents faster and spot discrepancies early, before they become payment delays.

Back-to-Back LC: the engine of Bangladesh’s garment trade

Honestly, no article about LC in Bangladesh is complete without a proper explanation of the Back-to-Back LC. This is how the garment industry runs.

Here’s the situation: a Bangladeshi garment factory receives an export LC from a foreign buyer (say, H&M or Walmart). They need to import fabric, accessories, and raw materials to fulfill that order. But they may not have cash to pay their fabric supplier upfront.

So the factory opens a second LC, backed by the incoming export LC. This is the Back-to-Back LC. The export LC from the buyer acts as collateral. The factory uses it to import what they need.

Key rules for BTB LC in Bangladesh per Bangladesh Bank guidelines:

- Back-to-back LCs must be opened on a usance basis for a period not exceeding 180 days

- They cannot be opened against LCs received under Barter/STA arrangements without prior Bangladesh Bank approval

- All amendments to the master export LC must be tracked carefully to avoid excess obligations under the BTB LC

This mechanism is what keeps Bangladesh’s RMG (Ready-Made Garment) sector, the country’s largest export earner, running at scale.

LC costs, margin, and bank charges

Opening an LC isn’t free. Your bank will charge commission, and they’ll likely ask for a margin deposit, which is a security deposit held against the LC value. The margin percentage varies by bank, your credit history, and the type of goods.

Commission is typically charged as a percentage of the LC value per quarter. Sight LCs, usance LCs, and back-to-back LCs each carry different commission structures. There are also courier and SWIFT transmission charges, LC amendment fees, and advising charges.

Because rates vary by bank and are periodically revised per Bangladesh Bank instructions, you should confirm current charges directly with your chosen bank before finalizing terms with your supplier.

For new importers, getting a loan from a Bangladeshi bank to cover the margin requirement is possible if your documents are in order. Top foreign banks in Bangladesh often have faster trade finance processing and stronger international correspondent banking networks, which matters when your exporter is in Europe or North America.

Common mistakes that cause LC discrepancies

A discrepancy means the documents don’t match the LC terms. The bank can refuse to pay until the discrepancy is resolved, and resolution can take days or weeks. Here’s what causes most of them:

- Invoice amount mismatch: The commercial invoice total doesn’t exactly match the LC amount

- Wrong description of goods: The invoice says “cotton shirts” but the LC says “cotton woven shirts, 100% cotton”

- Late presentation: Exporter presents documents after the LC’s expiry date or after the allowed days post-shipment

- Bill of Lading issues: Wrong consignee name, missing endorsement, or shipment date after the LC’s latest shipment date

- Partial shipment when prohibited: The LC says “no partial shipment allowed” but the exporter ships in two batches

- Wrong port of loading or destination: Any deviation from what’s written in the LC

To be real with you, even a missing comma in the invoice description has caused payment refusals. Read the LC line by line before you ship. And if you’re the importer, draft the LC terms carefully when applying. What you write goes into the LC exactly.

Building a DUNS number from Dun & Bradstreet for supplier credibility early also helps when working with overseas suppliers, since a verified business profile reduces friction in agreeing on LC terms.

2025 regulatory updates: what changed for Bangladesh traders

Two notable developments from 2025 affect how LC works in Bangladesh.

First, Bangladesh Bank issued a circular in 2025 easing import rules for industrial establishments in Export Processing Zones (EPZs) and Economic Zones (EZs). These companies can now import under a Letter of Agreement instead of a traditional LC. This gives export-oriented factories in special zones more flexibility in managing import financing.

Second, per a Bangladesh Bank directive highlighted in KPMG Bangladesh’s Q4 2025 regulatory update, all Authorized Dealers were reminded to follow URC (Uniform Rules for Collections) for non-LC trade transactions, including documentary collections, cash in advance, and open account trades. Previously, some ADs were applying UCP 600 rules to non-LC transactions. Now, UCP 600 applies only to LCs. URC applies to everything else.

For businesses considering top industries for foreign investment in Bangladesh where trade finance is critical, staying current on Bangladesh Bank FEPD circulars is non-negotiable. If you need a trade finance bank account to start LC operations, our guide on opening a business bank account in Bangladesh covers what Authorized Dealer banks need to onboard new trade clients.

Key Insights

- An LC is a bank’s payment guarantee, not a wire transfer. The importer’s bank pays the exporter only after verifying that all shipping documents match the LC terms exactly. Any discrepancy can delay payment.

- UCP 600 governs all LCs in Bangladesh, while from 2025, non-LC trade transactions (documentary collections, open account) must follow URC rules per Bangladesh Bank’s directive to Authorized Dealers.

- Back-to-Back LCs are how most of Bangladesh’s RMG factories import raw materials. They must be opened on a usance basis not exceeding 180 days and are backed by an incoming master export LC.

- Five types of LC are commonly used in Bangladesh: sight, usance, back-to-back, transferable, and standby. The right type depends on your cash flow, supplier trust, and trade structure.

- Discrepancies cost time and money. Under UCP 600, banks have 5 banking days to examine documents. A discrepancy means no payment until resolved. Most discrepancies are preventable with careful document preparation.

- Bangladesh Bank eased LC requirements in 2025 for industrial imports into EPZs and EZs, allowing Letter of Agreement in place of traditional LCs for eligible establishments.

- Your choice of Authorized Dealer bank matters. Banks with strong international trade desks process documents faster, catch discrepancies before submission, and have better correspondent bank networks for payment settlement.

Frequently Asked Questions

What is a letter of credit (LC) in Bangladesh?

A letter of credit (LC) in Bangladesh is a bank’s written commitment to pay an exporter once specific shipping documents are presented and verified. The importer’s Authorized Dealer bank issues the LC on behalf of the buyer. It protects both parties: the exporter knows payment will come if documents comply, and the importer knows payment goes out only after shipment documentation is verified.

Is LC mandatory for all imports in Bangladesh?

Most commercial imports into Bangladesh must be settled through irrevocable LCs under Bangladesh Bank regulations. However, there are exceptions. In 2025, Bangladesh Bank issued a circular allowing industrial establishments in Export Processing Zones (EPZs) and Economic Zones (EZs) to import under a Letter of Agreement instead of a traditional LC. Some specific approved import categories may also use alternative payment methods.

What is the difference between a sight LC and a usance LC?

A sight LC pays the exporter immediately once compliant documents are presented and verified. A usance LC (also called a deferred or time LC) pays at a future date, typically 30, 60, 90, 120, or 180 days after the sight date or shipment date. Usance LCs give the importer time to sell goods before the payment falls due, making them more cash-flow friendly for importers.

What is a Back-to-Back LC and who uses it?

A Back-to-Back LC is a second LC opened by an exporter against an incoming master export LC. It allows a factory to import raw materials needed to fulfill an export order without upfront cash. In Bangladesh, BTB LCs are heavily used by garment (RMG) factories. Per Bangladesh Bank guidelines, BTB LCs must be opened on a usance basis for a period not exceeding 180 days.

What documents does an importer need to open an LC in Bangladesh?

To open an LC, you typically need: a valid Import Registration Certificate (IRC), Trade License, TIN and VAT registration (BIN), completed LC Application Form, IMP Form, Proforma Invoice or Purchase Contract from your supplier, Insurance Cover Note, charge documents required by your bank, and a CIB report. Your bank may also require a Chamber of Commerce membership certificate for commercial imports.

What documents does an exporter need to get paid under an LC?

The exporter must present documents that match the LC terms exactly. Standard documents include: Commercial Invoice, Bill of Lading (sea) or Airway Bill (air), Packing List, Certificate of Origin, Insurance Certificate or Policy, and any other documents specified in the LC such as an Inspection Certificate. Under UCP 600, the bank has 5 banking days to examine the documents and decide whether to pay or refuse.

What happens if there is a discrepancy in LC documents?

If presented documents do not match the LC terms, the issuing bank issues a notice of refusal detailing the discrepancies. The exporter can then correct the documents if time allows before the LC expiry, request the importer to authorize acceptance of the documents despite discrepancies, or present them as a documentary collection item. Discrepancies cause delays and additional fees. Prevention through careful document preparation is always better.

What is the difference between an advising bank and a confirming bank?

The advising bank is the exporter’s bank that receives the LC from the issuing bank and notifies the exporter it has been opened. It doesn’t guarantee payment itself. A confirming bank adds its own independent payment guarantee to the LC. This means even if the issuing bank fails to pay, the confirming bank must pay. Exporters dealing with unfamiliar or smaller issuing banks often request confirmation for extra security.

Which banks in Bangladesh handle LC transactions?

All Authorized Dealer (AD) banks in Bangladesh are licensed to handle foreign exchange and LC transactions. This includes all major commercial banks, foreign banks operating in Bangladesh, and most state-owned commercial banks. Banks with strong international correspondent banking relationships process LC payments faster and handle document examination more efficiently. Checking a bank’s trade finance capability before opening an account is worthwhile.

What changed for LC regulation in Bangladesh in 2025?

Two key changes: First, Bangladesh Bank issued a circular in 2025 allowing industrial establishments in EPZs and EZs to import under a Letter of Agreement instead of a traditional LC. Second, per a Bangladesh Bank directive clarified in KPMG Bangladesh’s Q4 2025 regulatory update, Authorized Dealers must apply URC to non-LC trade transactions such as documentary collections and open account trades. UCP 600 now applies only to LC transactions specifically.

The Bottom Line

The LC isn’t just paperwork. It’s the mechanism that makes cross-border trade actually work when a buyer in Dhaka and a seller in Shanghai have never met and don’t fully trust each other. Once you understand the flow, the document logic makes complete sense: the exporter ships, provides proof, and gets paid. The importer releases funds only when the bank confirms everything is in order.

If you’re starting your first import or export transaction, open an account with an Authorized Dealer bank that has a serious trade finance desk before you commit to any supplier deal. The bank you choose shapes how smoothly every LC you open will run.