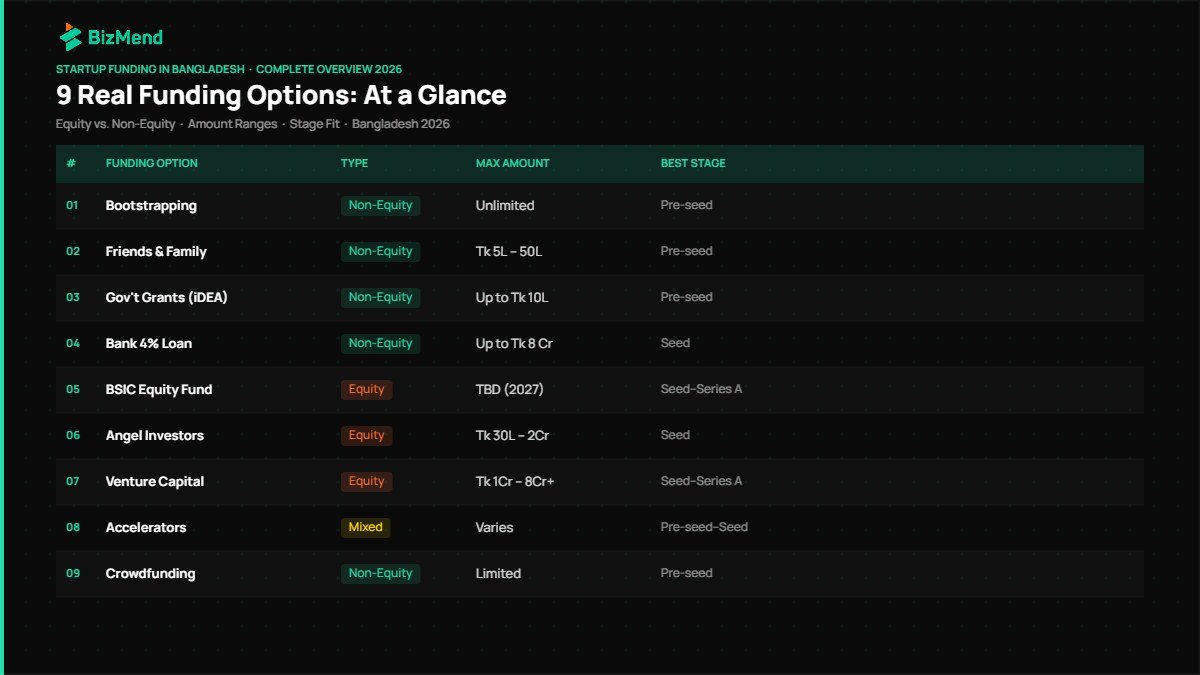

| Quick answer: Startup funding in Bangladesh in 2026 comes from nine main sources: bootstrapping, friends and family, angel networks like BAN, government grants from iDEA, Bangladesh Bank’s 4% startup loan (up to Tk 8 crore), the new Bangladesh Startup Investment Company, local VCs like SBK Tech and Anchorless, accelerators, and crowdfunding. Most B2B SaaS founders combine two or three by Series A. |

Raising money in Dhaka isn’t what it was in 2021. That year, Bangladeshi startups pulled in $434 million across 94 deals. By 2024, that number collapsed to $42 million. In 2025, only 12 rounds closed, and most of that came from a single ShopUp-Sary merger.

So why am I still bullish on startup funding in Bangladesh? Because the rules just changed. The central bank rewrote the startup loan framework. A brand-new Tk 425 crore equity fund went live. And most founders haven’t heard about either one yet.

This guide covers all nine real options — what they are, who they’re for, and exactly how to access them.

The Bangladesh startup ecosystem just lived through a brutal reset.

According to Tracxn data updated in April 2026, Bangladesh has 12,865 startups, 421 funded companies, and just 2 unicorns. Total venture and PE capital raised since the country started counting: $2.9 billion. To put that in perspective, Bengaluru does that in about a month. So yes, the pool is small.

But here’s what’s actually happening on the ground. Bangladesh Bank issued SMESPD Master Circular No. 02 on July 9, 2025, and it changed the math for every founder reading this. Loan ceilings jumped from Tk 1 crore to Tk 8 crore. Interest rates dropped to 4%. The upper age limit (45) got scrapped entirely. Banks can now make equity investments, not just loans.

Then in May 2026, the Bangladesh Startup Investment Company (BSIC) opened for business, backed by 39 banks contributing 1% of their 2020-2024 profits. Initial capital: Tk 425 crore. That’s roughly $35 million of fresh, bank-backed risk capital pointed at local startups, with BRAC Bank holding the largest share at 7.71%.

The point: capital is more available, but the bar is higher. Investors learned hard lessons in 2024. They want metrics, not vibes.

When Should You Actually Raise (and How Much)?

Most SaaS founders raise too early. I’ve seen this kill more cap tables than market timing.

Here’s a rough map:

- Idea stage (no MVP): Bootstrap. Maybe friends and family. Aim for $0 to $25,000.

- Pre-seed (MVP + first 5–10 paying customers): iDEA grant, angels, founder savings. Tk 30 lakh to Tk 1 crore.

- Seed (clear product-market fit, $5K–$25K MRR): BAN, SBK Tech Ventures, Anchorless, Startup Bangladesh Limited. Tk 1 to 8 crore.

- Series A ($50K+ MRR, repeatable sales motion): Cross-border VCs, regional funds, late-stage local players. $1M to $5M+.

If you’ve heard “raise as much as you can, as early as you can,” ignore that advice. It was bad in 2021. It’s worse now. Raise enough to hit the next milestone with 18 months of runway. That’s it.

9 Real Funding Options for Startups in Bangladesh

Here are the funding options for startups in Bangladesh that actually work in 2026, ranked roughly by stage.

1. Bootstrapping (Self-Funding)

The most underrated option. Period.

Bootstrapping means using your own savings, side income, or early customer revenue to fund the business. No equity given up. No board seats. No quarterly grilling.

The smartest pre-seed SaaS founders I’ve worked with in Bangladesh ran a small consulting or service business on the side. Building an HR SaaS? Run a payroll outsourcing service for 3 months while you build. The cash flow keeps the lights on. The work tells you what to build. Burning through personal savings while you “go all in” feels romantic. It also kills decision quality.

For SaaS founders, the goal isn’t to bootstrap forever. It’s to bootstrap to your first 10 paying customers, then raise on real traction instead of a promise.

2. Friends, Family, and Founder Loans

This is how most Bangladeshi founders actually start. You won’t see it in deck templates, but it’s the truth.

A few notes from working with local founders. Always paper it. Even with your uncle. A simple convertible note or SAFE template (Y Combinator publishes free ones) prevents heartbreak later. Document the amount, the conversion terms, and what happens if the company dies. Yes, it feels awkward. Do it anyway.

Pro tip: route F&F money through a properly registered entity. That means finishing your company registration with RJSC first. Otherwise you’re creating tax problems for everyone.

3. Government Grants (iDEA + Startup Bangladesh Limited)

Government startup funding in Bangladesh has quietly become a real category.

iDEA Project (ICT Division) offers pre-seed grants up to BDT 10 lakh for early-stage tech and innovation startups. Truck Lagbe and Skoot both used iDEA grants to bridge to commercial validation. Application is online, and the program also includes free co-working space and mentoring.

Startup Bangladesh Limited, the government VC sponsored by the ICT Division, has Tk 500 crore allocated. It invests at pre-seed, seed, and growth stages through equity, convertible debt, and grants. Past investments include Bimafy, Shuttle, and Pickaboo.

Reality check: government grants are slow. Plan 3 to 6 months from application to cash in your account. But they’re non-dilutive. That matters.

4. Bangladesh Bank’s 4% Startup Loan

This is the big news of 2025-2026 and most founders still don’t know about it.

Under the July 2025 Master Circular, eligible startups can borrow up to Tk 8 crore at 4% annual interest, with up to 8 years repayment including grace period. To qualify, you must be a Bangladeshi citizen aged 21 or older (no upper limit), with no loan default record, and your startup must be registered for less than 12 years and offer a tech-driven product or service with scalability.

A 500-crore refinancing facility from Bangladesh Bank backstops this, and banks can access central bank funds at just 0.5% interest, then lend to you at 4%. The spread is small enough that banks are actually motivated.

Mercantile Bank, NCC Bank, UCB, and Sonali Bank all have dedicated startup loan products under this scheme. If you have receivables, recurring revenue, or hard assets, this is some of the cheapest capital you’ll ever see. For B2B SaaS with predictable MRR, it’s almost free money compared to the dilution cost of equity. Just make sure your business bank account setup is rock solid before applying.

5. Bangladesh Startup Investment Company (BSIC)

Brand new. Worth knowing.

Launched May 12, 2026, BSIC is a Tk 425 crore equity-only investment company supported by 39 banks. It’s chaired by Mashrur Arefin (also City Bank MD) and will invest in 8 to 12 startups between 2027 and 2028.

Initial focus sectors: health, agriculture, education, transport, retail, and logistics. SaaS founders building for those verticals should be on their radar now, even though deals don’t close until 2027. Getting on their radar now, before deals open, will pay off.

The catch: BSIC takes equity. No interest. No loan repayments. They want ownership in exchange for capital.

6. Angel Investors and Networks

The angel investor market in Bangladesh has matured fast since 2019.

Bangladesh Angels Network (BAN) is the country’s first and largest angel platform. Since launch, BAN has facilitated $12M across 51 portfolio companies, including Pathao, Chaldal, Shajgoj, and PulseTech. The network has 500+ angels globally.

Bangladesh Women Investors Network (BWIN) is BAN’s sister chapter, focused on pre-seed and seed-stage startups led by women or solving women-centered problems.

How to get in front of angels: warm intros beat cold pitches by a mile. Attend BAN’s quarterly virtual showcases. Apply to be pitched. Build relationships months before you actually need money. The angels who invested in Pathao met its founders 18 months before the round.

What earns an angel check in 2026:

- Tk 5 to 10 lakh MRR (or USD-billed equivalent)

- 80%+ logo retention over 6 months

- A founder who knows their numbers cold

- Proof of at least one expansion within an existing customer

Hit those four and BAN angels engage. Miss them and don’t waste the round.

7. Local and Regional Venture Capital

Venture capital in Bangladesh is split between government-backed, local private, and cross-border funds. Here’s a working list of who’s active in 2026:

| Fund | Focus | Stage |

|---|---|---|

| Startup Bangladesh Limited | Tech, SDG-aligned | Pre-seed to growth |

| SBK Tech Ventures | Fintech, healthtech, edtech | Early stage |

| Anchorless Bangladesh | Scalable tech, exit-ready | Seed to Series A |

| BD Venture | Fintech, e-commerce, agritech | Early to growth |

| IDLC Venture Capital | Tech and tech-enabled | Early to growth |

| Pegasus Tech Ventures | Cross-border tech | Seed to Series B |

| Razor Capital | Consumer, agritech, gig | Early to growth |

| DIVC (Dekko ISHO) | Deep tech, AI, agritech | Seed |

| Flagship Ventures | Local-to-global SaaS | Seed to Series A |

| Maslin Capital | Late-stage venture | Series B+ |

For SaaS specifically, Anchorless, SBK Tech, and Flagship Ventures are the most active in 2026. Anchorless wrote checks into Pathao and Agroshift. SBK has the Silicon Valley network most local funds lack.

If your sector touches fintech or capital markets, an investment bank in Bangladesh like IDLC Investments or LankaBangla can help structure later rounds and eventual exits.

Cross-border VCs that take Bangladesh meetings. Local capital realistically tops out around $2 to $3 million. Past that, founders look outward. The funds actively writing Bangladesh checks in 2026 include Surge by Peak XV (formerly Sequoia India), which backed 10 Minute School at pre-seed and Shikho at seed; Lightspeed India, with an emerging-market B2B SaaS bias; Antler, whose global pre-seed program has active Bangladesh founders; Insignia Ventures for SEA-flavored deals; and Endiya Partners for cross-border SaaS. Warm intros required. Cold pitching cross-border rarely works. The path goes from portfolio founder intro to associate to partner.

When local capital runs out: the Delaware flip. If your customers are mostly global (US, EU, or SEA), most international VCs will require you to incorporate a Delaware C-Corp parent company and make the Bangladesh entity a subsidiary. This costs $10,000 to $15,000 in legal fees and takes 4 to 8 weeks. Do it 9 to 12 months before you start the Series A process. Mid-pitch flips read as red flags to investors.

8. Accelerators and Incubators

Less capital, more curriculum. Best for first-time founders.

Active programs in Bangladesh: Tiger Cage (the Shark Tank-style show by Startup Dhaka, up to 2 crore taka), iDEA Accelerator, Banglalink IT Incubator, GP Accelerator (Grameenphone), r-ventures (Robi Axiata), and Toru (BRAC’s social impact incubator that backed Sheba.xyz, iFarmer, ShopUp, and 10 Minute School in early days).

If you’re building a B2B SaaS for the local market and need product-market fit guidance, an accelerator is worth more than the check. If you already have $10K MRR and a clear thesis, skip them. Go straight to angels.

9. Crowdfunding and Alternative Financing

Crowdfunding in Bangladesh is the weakest of the nine options. Honest take.

Bangladesh has no JOBS Act equivalent. Equity crowdfunding is essentially unregulated. Reward-based platforms like GoRiseMe and Oporajoy exist, but they skew toward charitable causes, not B2B SaaS rounds. BSEC has discussed small-cap stock exchange rules to give startups exit pathways, but it’s still early.

Alternative financing that works better for SaaS:

- Convertible notes / SAFE agreements: standard global instruments, accepted by Bangladesh Angels and most local VCs. Quick rule: if you’re 6 months from a likely larger round, take a SAFE with a cap. If you’re 18+ months out, take priced equity with a clean term sheet. Avoid uncapped notes. They almost always burn the founder later.

- Revenue-based financing: rare locally, but cross-border platforms like Pipe and Capchase will work with Bangladeshi SaaS that bills in USD.

- Venture debt: offered through selectcommercial banks in Bangladesh for post-revenue companies.

If you’re billing global customers in dollars, revenue-based financing is genuinely worth looking at. No dilution. Repays from MRR.

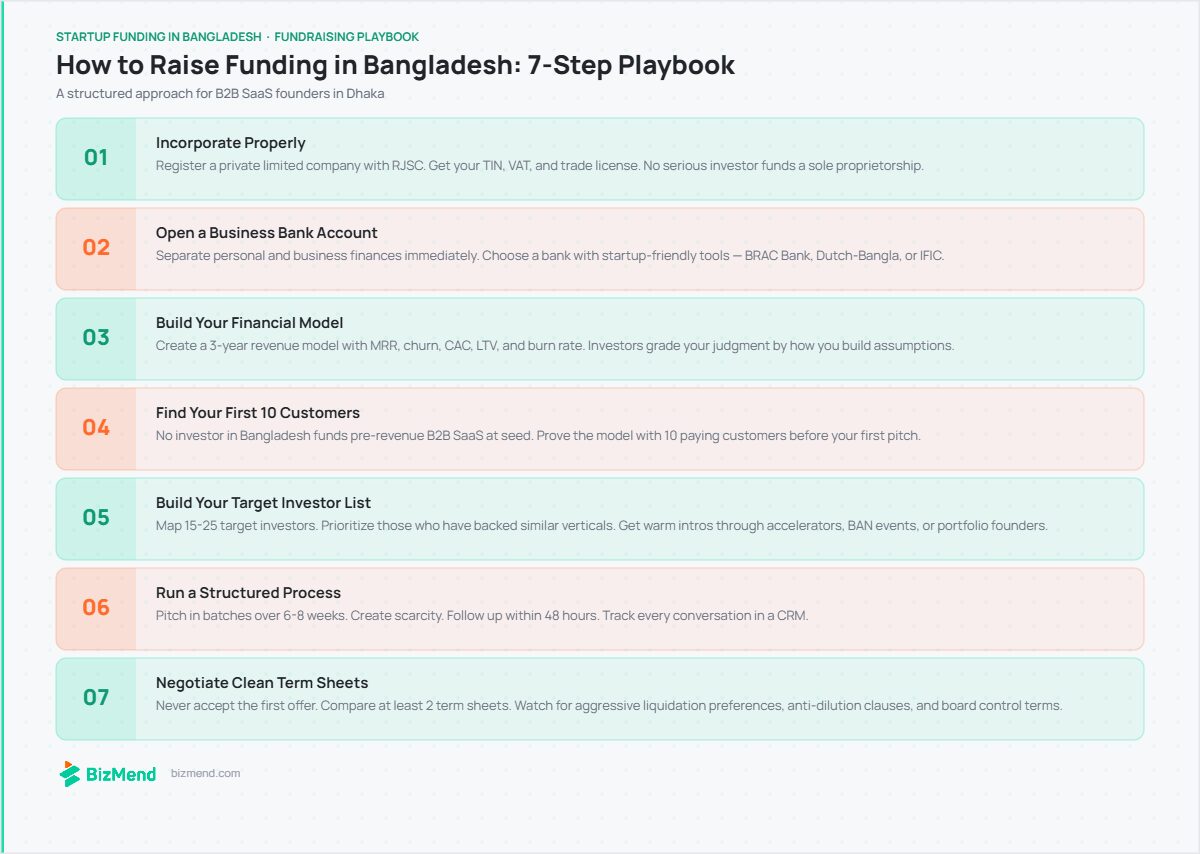

How to Raise Funding in Bangladesh: A 7-Step Playbook

This is the playbook I’d give a B2B SaaS founder in Dhaka starting from zero today.

1. Incorporate properly first. Register a private limited company with RJSC. No serious investor will fund a sole proprietorship. Get your TIN, VAT registration, and trade license sorted. This takes 2 to 4 weeks.

2. Open a separate business bank account. Mix personal and business funds and you’ll lose the round at due diligence. Pick a bank that understands tech (BRAC, City, Eastern, Dutch-Bangla).

3. Prove a real metric. For SaaS, that’s MRR + 6-month retention. Not “users.” Not “downloads.” Paid retention. Investors in 2026 are skeptical, and the only thing that cuts through skepticism is data.

4. Build a real pitch deck. 10 to 12 slides max. Problem, solution, market size, traction (numbers), business model, GTM, team, ask, use of funds, milestones. No one reads slide 15.

5. Match your stage to the right investor. Sending an iDEA grant request to Anchorless wastes everyone’s time. So does pitching SBK Tech a $2M pre-seed round. Match the round size and stage to the source.

6. Run a proper process. Pick 15 to 25 target investors. Get warm intros (LinkedIn, accelerator network, BAN events). Pitch in batches. Create scarcity. A two-month window beats a one-year drift.

7. Negotiate cleanly. Don’t accept the first term sheet. Compare 2 to 3 if you can. Watch for liquidation preferences, anti-dilution clauses, and board composition. A lawyer who has done startup deals before is non-negotiable here, not optional.

5 Metrics Bangladeshi Investors Actually Care About in 2026

Skip vanity stats. Investors in Dhaka are looking at:

1. Net Revenue Retention (NRR). 100% or higher means happy customers. Below 90% kills the round.

2. CAC Payback Period. Under 12 months is great. Under 18 is okay. Over 24 is dead.

3. Burn Multiple. Net burn divided by net new ARR. Below 2x is healthy. Above 4x and you’ll get hard questions.

4. Founder Salary vs. Runway. Investors check this. Paying yourself $4K a month while burning $30K monthly looks irresponsible.

5. Real Sales Pipeline Coverage. 3x pipeline coverage of next quarter’s target. Less than that and your forecast reads like fiction.

I watched two founders lose rounds in 2025 specifically because their burn multiple was 7x. The product was fine. The capital efficiency story was broken.

5 Mistakes That Kill SaaS Funding Rounds in Bangladesh

1. Pitching too early with no traction. Investors in 2026 want at least $5K MRR and 80%+ logo retention before serious seed conversations.

2. Optimizing for valuation over investor quality. A $3M valuation from a smart angel beats a $5M valuation from someone who’ll ghost you in month four.

3. Ignoring local compliance. Founders skip RJSC filings, miss VAT deadlines, then scramble during due diligence. Investors notice. Some pull out.

4. Confusing grants with equity. Government grants like iDEA aren’t a substitute for raising. They’re a runway extender. Plan for the next round before the grant lands.

5. Underestimating cross-border complexity. Many Bangladeshi SaaS companies serve global customers but bill in BDT through local accounts. That hurts valuations. Consider a Delaware C-Corp parent if you’re targeting international VCs.

Key Takeaways

- Funding is back, but the bar is higher. Bangladesh raised $124M in 2025 across just 12 deals, with most coming from a single ShopUp-Sary deal. Investors want real metrics, not pitch deck dreams.

- The Bangladesh Bank 4% loan is the biggest unlock. Up to Tk 8 crore at 4% interest with no upper age limit is some of the cheapest capital available anywhere. Many SaaS founders qualify and don’t know it.

- BSIC changes the math for late seed and Series A. A Tk 425 crore equity-only fund backed by 39 banks reshapes what’s possible for local startups in health, agriculture, education, transport, retail, and logistics from 2027 onward.

- Angels are still active when VCs aren’t. Bangladesh Angels Network has facilitated $12M across 51 companies and runs quarterly showcases. For pre-seed and seed-stage SaaS, BAN often beats cold-emailing VCs.

- B2B SaaS founders should stack non-dilutive capital first. iDEA grants, the 4% loan, and revenue-based financing extend the runway without giving up equity. Save dilution for when growth capital actually needs to be deployed fast.

- Compliance kills more rounds than market timing. Skipping RJSC filings, mixing personal and business banking, or ignoring VAT registration creates due diligence problems that investors won’t fix for you.

Frequently Asked Questions

How much funding can a startup get in Bangladesh in 2026?

Funding amounts vary by stage and source. Government grants like iDEA offer up to BDT 10 lakh, the Bangladesh Bank 4% loan goes up to Tk 8 crore, angel rounds typically range from Tk 30 lakh to Tk 2 crore, and seed VC rounds from local funds usually fall between Tk 1 crore and Tk 8 crore. Series A from regional or cross-border VCs can hit $1M to $5M for proven SaaS companies.

What is the easiest way to get startup funding in Bangladesh?

The lowest-friction path for most early-stage founders is the iDEA grant (non-dilutive, online application) combined with the Bangladesh Bank 4% startup loan. Neither requires giving up equity. Both are available to registered businesses with no loan default history. The catch is time: government processes run 3 to 12 weeks depending on documentation readiness.

What legal structure do I need before raising investment?

Register a private limited company with RJSC, get a TIN, complete VAT registration, and obtain a trade license before pitching. Sole proprietorships and partnerships create tax and liability problems that investors avoid.

Can foreign investors fund startups in Bangladesh?

Yes, foreign investors can fund Bangladeshi startups, and most local VCs operate cross-border. Capital must flow through proper banking channels, and any equity investment requires BIDA notification for repatriation rights later. Many SaaS founders set up a Delaware or Singapore parent company to make foreign VC investment easier.

What is the Bangladesh Bank Startup Loan and who qualifies?

The Bangladesh Bank Startup Loan offers up to Tk 8 crore at 4% annual interest with up to 8 years repayment under SMESPD Master Circular No. 02 dated July 9, 2025. To qualify, you must be a Bangladeshi citizen aged 21 or older, free of any loan default records, and your startup must be registered for under 12 years and offer a technology-based scalable product or service.

What is crowdfunding like in Bangladesh?

Crowdfunding in Bangladesh is limited. There’s no equity crowdfunding regulation equivalent to the US JOBS Act. A few platforms like GoRiseMe and Oporajoy support reward-based and donation campaigns, but they skew toward social causes. Most founders use crowdfunding only for product launches or specific campaigns, not as a primary funding source.

What are the top venture capital firms in Bangladesh?

The most active venture capital firms in Bangladesh in 2026 include Startup Bangladesh Limited, SBK Tech Ventures, Anchorless Bangladesh, BD Venture, IDLC Venture Capital, Pegasus Tech Ventures, DIVC, Razor Capital, Flagship Ventures, and Maslin Capital. For B2B SaaS specifically, Anchorless, SBK Tech, and Flagship Ventures are the most relevant early-stage backers.

How long does it take to raise a seed round in Bangladesh?

A seed round in Bangladesh typically takes 4 to 8 months from first conversations to wire transfer. Government grants take 3 to 6 months. The 4% Bangladesh Bank loan takes 6 to 12 weeks once your documentation is complete. Plan for the slower end of these ranges and start fundraising before you actually need the cash.

Can a B2B SaaS startup in Bangladesh raise money from international investors?

Yes, but most international VCs prefer to invest via a Delaware C-Corp or Singapore parent company. A Bangladesh-only corporate structure makes repatriation complicated and limits exit options. If your MRR is mostly in USD and you’re targeting $1M+ rounds, plan the Delaware flip early — not mid-raise.

The Bangladesh startup market is still small by global standards. A good year here wouldn’t move the needle on a single Indian unicorn round. But that’s also why right now is interesting. The cheap capital is here. The 4% loan is real. BSIC is live. And competition for the few hundred SaaS founders building seriously in Bangladesh is far lower than competition for the millions building in Bangalore.

If I were starting a B2B SaaS in Dhaka tomorrow, I’d stack the iDEA grant, apply for the 4% loan against my MRR, raise a small angel round through BAN to bridge to seed, and only then talk to VCs. Slow, deliberate, dilution-aware. The founders who play it that way will be the ones standing in 2030.

What’s the one funding source you’ll explore this week?