How to Become a Daraz Seller in Bangladesh: Registration, Fees & Growth

Learn how to become a Daraz seller in Bangladesh, register an account, list products, understand fees, manage orders, and grow…

International payments are now normal for Bangladeshi freelancers, remote workers, agencies, creators, students, and online business owners, especially as freelancing in Bangladesh becomes more formal. The hard part is choosing...

International payments are now normal for Bangladeshi freelancers, remote workers, agencies, creators, students, and online business owners, especially as freelancing in Bangladesh becomes more formal. The hard part is choosing the right payment method, sharing the correct details, understanding fees and exchange rates, and keeping clean records for your bank and tax file.

This guide explains how to receive international payments in Bangladesh through Payoneer, Wise transfers to Bangladesh, and direct bank wires and how they differ from a payment gateway in Bangladesh for website-based collections.

Quick Answer: An FDR (Fixed Deposit Receipt) in Bangladesh is a savings instrument where you deposit a lump sum with a bank for a fixed period at a fixed interest rate. In 2026, FDR rates remain elevated, but the exact rate varies by bank, tenure, deposit amount, and product type. Bangladesh Bank kept the policy/repo rate at 10% for January-June FY26. Tax is deducted at source from FDR interest under applicable NBR rules. For individual depositors, the rate is commonly treated as 10%, while different depositor types may face different rates; confirm the latest rate with the bank or NBR before opening.

There is no single best freelancer payment method BD workers should use for every project. The right option depends on the client, country, amount, speed, supported route, and the documentation you need later.

| Method | Best for | Main benefit | Watch out for |

| Payoneer Bangladesh | Freelancers, marketplaces, agencies, remote contractors | Flexible receiving and withdrawal options where eligible | Fees and features vary by account, route, currency, and payer method |

| Wise to Bangladesh | Individuals sending BDT to your Bangladesh bank, bKash, or Nagad account through a supported Wise route | Sender sees fee and delivery estimate before paying | Wise says business transfers to BDT are not currently supported, and Bangladesh addresses cannot get USD account details |

| Bank wire Bangladesh | Larger agency, B2B, consulting, or service-export payments | Strong bank documentation and formal inward remittance record | Can be slower and may involve bank or intermediary charges |

For beginners, Payoneer is often easiest because many freelance platforms and global clients already know it. Wise can work well for direct transfers into Bangladesh when the sender’s route is supported. Bank wire is still important for larger clients, retainers, and business payments.

Bangladeshi freelancers usually receive money through marketplace payouts, direct client payments, agency contracts, or business invoices. A beginner may get paid from a freelance platform. A remote worker may receive monthly contractor payments. An agency owner may invoice a foreign company and receive money through Payoneer or bank wire.

The safest rule is simple: use formal payment channels, receive money in your own name or business name, keep invoices, and save statements. Bangladesh’s official Freelancer ID platform recognizes freelancer income documents such as bank statements, MFS statements, remittance advice, and bank certificates for freelance or IT-enabled service income.

Payoneer is one of the most common international payment options for freelancers, agencies, affiliate marketers, creators, e-commerce sellers, and remote contractors. Eligible users can receive money from clients, marketplaces, and platform partners, then withdraw funds to a local bank account where supported.

Payoneer may also provide receiving account details in supported currencies. These can help some users receive payments from clients in a local-account style. However, Payoneer states that such receiving accounts are not actual bank accounts and cannot be charged like normal bank accounts, so only use them for supported incoming payments.

Do not assume one fixed Payoneer fee for Bangladesh. Official Payoneer pricing shows that fees depend on the payment type, payer method, currency, corridor, and account location. Receiving from another Payoneer balance can be free; marketplace payouts vary by marketplace; local-currency receiving accounts may be free; non-local currency receiving accounts may carry a fee; card-funded payments can cost more; and bank withdrawals vary by destination, currency, and route. Payoneer also says exact fees are shown before confirmation, and that final pricing can vary by account type, territory, onboarding channel, payment method, currency, and corridor.

For practical planning, look at three things: receiving fee, exchange-rate impact, and withdrawal or bank-side fees. The final BDT amount depends on all three. For most freelancers, the cleanest workflow is to receive money in Payoneer, review the rate and fee, then withdraw to your own Bangladeshi bank account.

Avoid informal dollar exchange groups, account buying or selling, and third-party cash-out shortcuts. They may look fast, but they create fraud risk, account limitation risk, and weak documentation.

Wise is useful for Bangladesh, but it is often misunderstood. There is a difference between receiving a Wise transfer into Bangladesh and having full Wise account features as a Bangladesh resident.

Wise supports BDT transfers into Bangladesh. Its BDT guide says a sender can send money to bank accounts, bKash accounts, and Nagad accounts in Bangladesh. For bank transfers, the sender normally needs the recipient’s full name, bank and branch details, and account number. Wise also says BDT cannot currently be sent from BDT, and its guide notes restrictions for business transfers to BDT.

For Bangladeshi freelancers, Wise is useful when a sender can use Wise to send BDT directly to your Bangladesh bank, bKash, or Nagad account. However, freelancers should confirm the sender type first because Wise says business transfers to BDT are not currently supported.

Do not tell a client to send USD to your Wise account unless your Wise dashboard clearly shows eligible USD account details, because Wise says users with a Bangladesh address cannot get USD account details. Wise’s help center says USD account details are not available if your address is in Bangladesh. Wise’s holding-money availability page also does not list Bangladesh among the countries and territories where customers can hold money in a Wise account. Features can change, and older accounts may differ, so always verify inside Wise before giving payment instructions.

If your client is a company paying an invoice, confirm whether Wise supports that exact transfer type to Bangladesh. For larger company payments, Payoneer or bank wire may be more reliable.

Bank wire is the traditional way to receive foreign payments directly into a Bangladeshi bank account. It is useful for larger freelance invoices, agency retainers, software services, consulting, and formal business payments. The client sends money from their bank to your bank using international transfer instructions, often through SWIFT.

Bank wire can be slower than platform payouts, but it gives strong documentation. Your bank statement shows inward remittance, and you can request payment advice or a bank certificate when needed.

Always collect wire details from your bank’s official website, branch, app, or customer support. Do not copy old screenshots or random SWIFT codes from social media. One wrong detail can delay the transfer.

Yes, foreign income can enter Bangladesh through formal banking and approved payment channels, but many freelancers receive the final amount in BDT. Whether you can retain foreign currency in an ERQ account depends on your bank, service-export status, documentation, and applicable Bangladesh Bank rules. Many freelancers simply receive converted BDT in a local bank account.

Some eligible service exporters and freelancers may ask authorized dealer banks about Exporters’ Retention Quota, or ERQ, accounts. Bangladesh Bank has advised authorized dealers to provide ERQ account services to ICT companies, freelancers, and other cross-border service providers so they can carry out remittance transactions from those accounts. If you regularly pay for foreign tools, software, ads, hosting, or subscriptions, ask your bank whether ERQ or an international card facility is suitable for your work.

| Situation | Recommended option | Why |

| Freelance platform payouts | Payoneer | Many platforms support Payoneer payouts and statements. |

| A foreign individual client wants a simple transfer | Wise, Bangladesh, or Payoneer | Depends on sender availability, route support, and fees. |

| A foreign company is paying a larger invoice | Bank wire or Payoneer | Better for formal records and business payments. |

| You need strong bank documentation | Bank wire | Direct inward remittance appears in your bank account. |

| You want to hold funds before withdrawal | Payoneer, if eligible | Wise balance-holding features are limited for Bangladesh residents. |

A practical setup is to keep two formal routes ready: Payoneer for platform and recurring online payments, and bank wire for larger direct clients. Use Wise when the client prefers it and the Bangladesh transfer route is supported.

International payment costs usually come from four places: the sender’s bank or platform, the receiving platform, the exchange-rate spread, and intermediary or local bank charges. That is why ‘no fee’ does not always mean ‘no cost.’ A payment may show no visible receiving fee but use a weaker exchange rate.

Before choosing a route, compare the total fee, exchange rate, delivery time, and documentation quality. A small $50 project may not justify a bank wire. A $5,000 agency invoice may deserve a formal bank wire or business-friendly Payoneer route.

The safest payment method is not always the fastest one. Formal payment history is valuable because it helps prove income later.

Many payment problems start because the invoice is unclear. A good invoice helps your client, your bank, and your tax records.

Short purpose note, such as digital marketing service or software development service

| Sample line: Please include Invoice #BD-2026-014 in the payment reference. Payment is for digital marketing services provided remotely from Bangladesh. |

For recurring clients, set clear payment terms such as 50% upfront, weekly milestones, or a Once income becomes consistent, upgrade your setup with business registration, a separate business account, bookkeeping, a tax adviser, and a clear payment policy. monthly retainer due within seven days. Avoid vague terms like ‘pay later.’

This is general guidance, not tax advice. Bangladesh tax rules can change, and your obligation depends on your income, status, business structure, and current law. If your foreign income is growing, speak with a qualified tax professional.

In practice, freelancers should keep organized income records, get an e-TIN when required, and file tax returns when required. NBR provides income tax FAQs and the e-Return platform for online return-related services. Keep invoices, platform statements, Payoneer statements, Wise receipts if available, bank statements, remittance advice, contracts, and client emails in one folder.

Start simple. Open one local bank account in your own name. Create a Payoneer account if your platform or client route supports it. Ask your bank for correct wire instructions and save them. Use Wise only when your client can send directly to Bangladesh through a supported route. Create one invoice template and use it every time.

Once income becomes consistent, upgrade your setup with a separate business account, bookkeeping, a tax adviser, a clear payment policy, and US company formation if you plan to work with international clients through a formal business structure. Agencies should receive payments under the business name instead of mixing all client income into a personal account.

For most freelancers, Payoneer is practical for platform and recurring client payments. Wise is useful when a client sends money directly to Bangladesh through a supported route. Bank wire is better for larger and more formal business payments.

Freelancers can receive foreign income through formal channels, but funds may be converted into BDT depending on the route. Eligible service exporters can ask authorized dealer banks about ERQ accounts under applicable rules.

Payoneer is commonly used by Bangladeshi freelancers and online workers. Specific features, receiving accounts, cards, withdrawal routes, and fees depend on current Payoneer policy and account eligibility.

Wise can be useful when a client sends money to your Bangladesh bank, bKash, or Nagad account through a supported Wise route. Bangladesh residents should not assume they can get Wise USD account details or hold balances like users in some other countries.

Yes. Bank wire is a formal way to receive larger international payments. Provide accurate SWIFT and account details, use a clear invoice, and keep source-of-funds documents ready.

Freelancers should keep records and follow Bangladesh tax rules. Whether tax is payable depends on income level, status, exemptions, business structure, and current law. Use NBR resources and consult a qualified tax professional.

No. For freelance and business income, use formal, document-friendly routes. Unofficial exchangers and risky shortcuts can create fraud, compliance, and account problems.

Receiving international payments in Bangladesh is manageable when you use formal routes and keep records. Payoneer is strong for freelancers and online platforms, Wise works when a client can send directly into Bangladesh, and bank wire is best for larger formal invoices.

Use your own verified accounts, check fees and exchange rates before each transfer, withdraw through clean channels, and save every invoice and payment record. That habit protects your income today and builds a stronger financial history for tomorrow.

Learn how to become a Daraz seller in Bangladesh, register an account, list products, understand fees, manage orders, and grow…

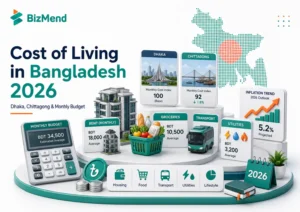

Compare the cost of living in Bangladesh in 2026, including Dhaka and Chittagong rent, food, transport, utilities, inflation, and monthly…

Learn MoA and AoA requirements in Bangladesh, key clauses, drafting basics, RJSC filing steps, amendments, and common company-registration mistakes. Suggested…